Topics, 100 Accounting Resources, 100 Reading List

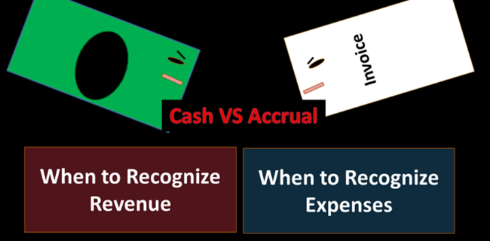

Generally Accepted Accounting Principle GAAP will be based on accrual concepts. The accrual basis can be compared and contrasted to a cash basis, the cash basis being a simplified method, one which does not provide information as useful, as relevant, or as accurate as an accrual method.

Cash basis – Records revenue when cash is received and expenses when cash is paid. A cash basis is not the basis required by GAAP, GAAP rules following an accrual basis, but understanding a cash basis helps in understanding both how an accrual basis works and the reasons for it. Cash and revenue are not the same things, as we will see when we record transactions, but a cash basis uses cash as an indicator of when revenue will be recorded. The concept of a cash basis is like a firefighter following the smoke to get to a fire, the smoke not pinpointing the exact location but being close enough. Cash collection does not always equal the exact location in time of revenue earnings but is often close enough.

In a similar way as revenue being recorded when cash is received under a cash basis, expenses are recorded when cash is paid under a cash basis. Cash and expenses are also not the same things, as we will see when we record transactions, but a cash basis uses cash as an indicator of when expenses will be recorded. The concept of a cash basis is like a firefighter following the smoke to get to a fire, the smoke not pinpointing the exact location but being close enough. Cash payment does not always equal the exact location in time expenses were incurred but is often close enough.

Very few businesses use a pure cash basis because there are times when the smoke is not close to the fire, times when revenue is not close to cash collection, and times when expense incursion is not close to cash payment. For example, almost any business would recognize a cash payment of $100,000 for a building as an asset of a building rather than an expense of building expense even though cash is paid. The reason a building is recorded as an asset is that the asset has not yet been consumed, has not yet been used to generate revenue.

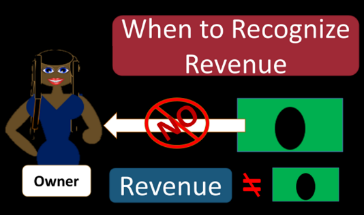

Revenue recognition is. . .

For more reading consider the e-book below