And I’m going to say it’s going to be unrestricted. And then we don’t need anything here, the debit amount is going to be that 11 five, I believe is what we’re working with here. 11, five, yes, 11 500. We don’t need any any other categorization here. So we look good, the other side is going to be going out of that new account, we set up in the expenses, pp and e 8100. It’s also it’s going to be the fun should be unrestricted, I’m going to say unrestricted here, unrestricted. And then that’s going to be the credit of 11 500. Now, if you’re not good with with the debits and credits, obviously, if you went the wrong way, what would happen you’d see this account be doubled. And in that would be wrong way, right. And then you just switch the debits and credits, and you’d be back on so the total debits add up to the total credits, this is going to be our transaction.

Posts with the property tag

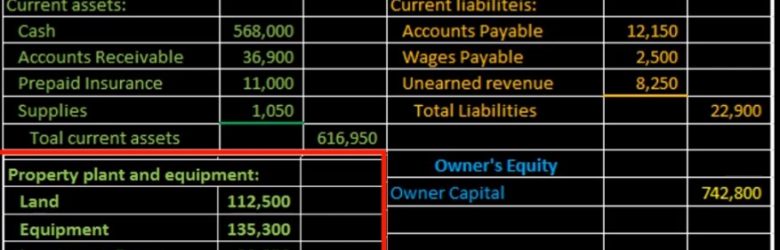

Balance Sheet Property Plant %26 Equipment From Trial Balance 13

Hello in this lecture we’re going to put together the section of the balance sheet of property plant and equipment from the trial balance property, plant and equipment will be part of the assets can be the subcategory of assets, we talked last time about the creation of the current assets. And now we’ll be moving on to property, plant and equipment, which will then sum up everything for total assets. We will be picking these numbers up from a trial balance. And once we have completed all the financial statements, what we’re basically doing is taking a debit and credit format from the trial balance, converting it to a plus and minus format in terms of the financial statements, assets, equal liabilities plus owner’s equity so that people can read it even if they don’t understand debits and credits. In this lecture, we’re focusing in on this section here, which will be a land equipment and each cumulated depreciation.