Retiree Health Costs Demand Financial Wellness

Retiree Health Costs Demand Financial Wellness https://t.co/MktrpcwO3U pic.twitter.com/7lOfxjMwQY

— CFO (@cfo) July 9, 2017

Confessions of a Millennial CPA: Your boss is asleep

Confessions of a Millennial CPA: April is firing season and your boss is asleep. What happens then? https://t.co/R16QZQIp9r

— Accounting Today (@AccountingToday) July 7, 2017

Accounts Receivable General Ledger 200

Download the Excel worksheet to get the most out of this problem or to add it to your curriculum.

Download is not required to watch the video and see how the problem is worked but working through problems in Excel is the best way to understand accounting. Worksheet includes example tab with answer, a tab to work the problem, and hyper links to instructional videos.

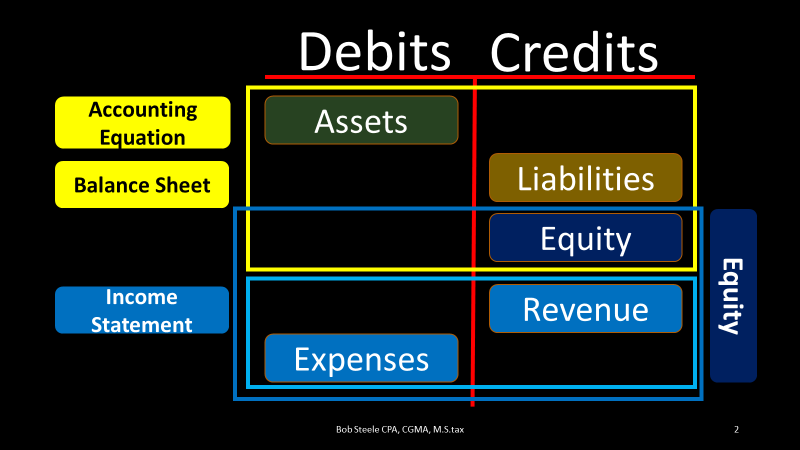

One Rule for Increasing and Decreasing an Account Balances

Once we understand the normal balance of an account, represented by the image below, there is only one rule we need to know to make an account go up or down.

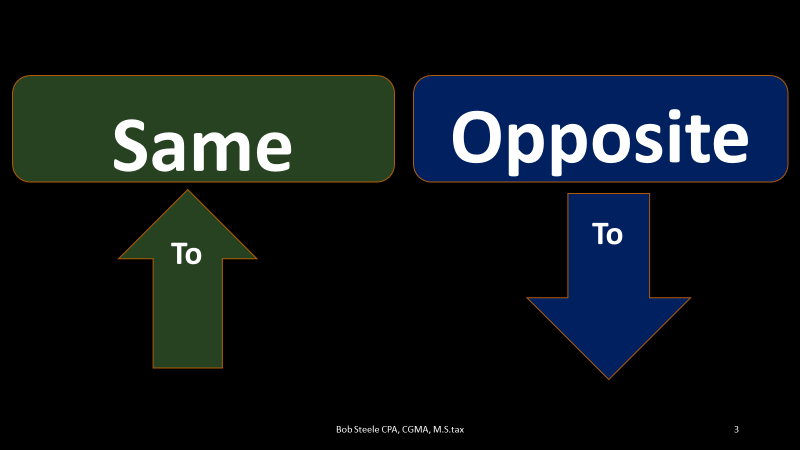

The rule to make an account balance go up or down is: do the same to go up and opposite to go down.

The rule of, do the same to go up and opposite to go down, may seem abstract at first but once we have the normal balance cheat sheet above it is easy to apply. The one rule means that an account with a normal debit balance will be increased by another debit because a debit is the same thing as the normal account balance and an account with a normal credit balance will be increased by a credit because a credit is the same thing as the normal account balance. Conversely, an account with a normal debit balance will be decreased by a credit because a credit is the opposite thing as the normal account balance and an account with a normal credit balance will be decreased by a debit because a debit is the opposite thing as the normal account balance.

Like most thing, the one rule is best learned through doing, by running through examples of transactions again and again.

Fortunately we have some examples of transactions here.

AICPA seeks input for new framework on valuation of financial instruments

The new guidance aims for clarity, consistency and transparency https://t.co/LxcrsEh7r6

— JournalofAccountancy (@AICPA_JofA) July 6, 2017

Companies grapple with leasing standard complications

Companies are starting to grapple with some of the unexpected complications of the new lease accounting standard. https://t.co/01Pd8OFucU

— Accounting Today (@AccountingToday) July 6, 2017