It’s not good for your back.

If somebody up there really needs something they can come down so you can give laterally rather then up. . .

especially if you are giving something heavy.

I Don’t Think Anybody Should Ever Give Up

It’s not good for your back.

If somebody up there really needs something they can come down so you can give laterally rather then up. . .

especially if you are giving something heavy.

I Don’t Think Anybody Should Ever Give Up

This presentation, we will continue on looking at the company preferences, this time focusing in on the checking preferences, although we will also take a quick look at the bills and the calendar preferences within QuickBooks Pro QuickBooks desktop 2020. Here we are in our get great guitars file, we’re going to go back into the preferences by going to the Edit drop down up top, and we’re going to go back down to our preferences, edit and event preferences, we did the accounting last time, we’re going to be moving down from accounting will be stopping at the checking item here.

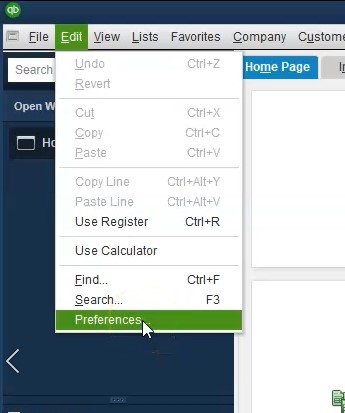

This presentation, we will take a look at company preferences focusing in on the accounting preferences within QuickBooks Pro QuickBooks desktop 2020. Here we are in the QuickBooks system, we’re at our homepage. Typically, when I’m in the homepage, I usually like to have the open windows open. So usually every time I go in here, we go to the View tab, and we go to the open windows list. And that’s what I would prefer doesn’t really matter here with what we’re doing.

0:26

But that’s typically the system I will have every time, we’re then going to go to the preferences to do so we will go to the Edit screen up top will scroll down to the company preferences, and we want the company preferences. Now there’s a lot of preferences and they could be confusing, you’ve got the preferences on the left, that will be by category, you also typically will have tabs up top depending on what preference you are in for my preferences in the company preferences. So we’re going to go through a lot of these mini the default settings are pretty good. So don’t be too overwhelmed because the default settings are generally good.

0:59

And they’ll okay to move forward. With a practice problem like this. In particular, we want to go into the company settings so that we can get rid of some annoyances such as time, our time constraints, that will give you a warning type of thing when we’re working in the past or the future.

1:15

They’re not as effective. We also just want to discuss the company preferences, because different people have different preferences. And if you set up on or you sit on someone else’s computer or someone else’s QuickBooks files with different preferences, and you can start to annoying and have annoying little things happen. And you say, Well, why is that different, it’s just the way the preferences are set up. And you can see where those are at and understand what’s going on.

1:36

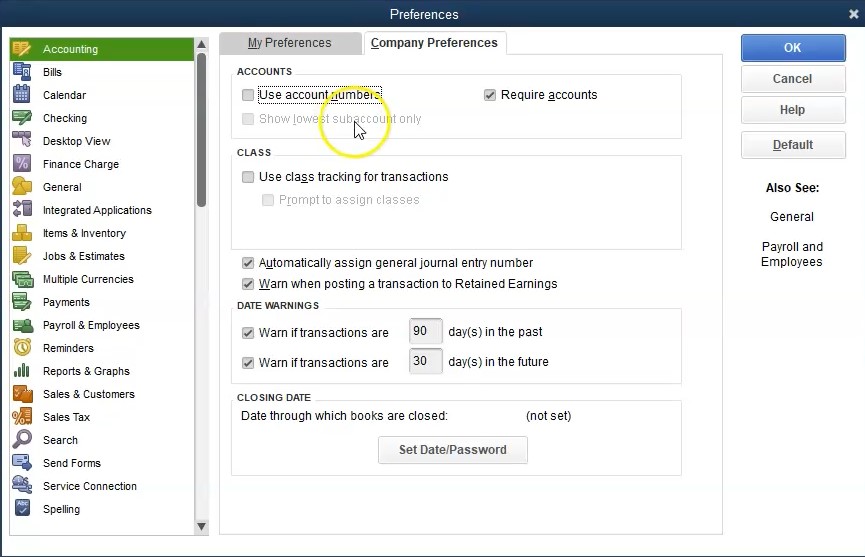

Therefore, we will start at the top with the accounting preferences, you’ll see there’s two tabs up top we have the my preferences and we have the company preferences, we then have nothing in the my preferences, which is nice and makes it easy, we’re going to go into the company Preferences Tab, then we have the user account numbers and require accounts. Now, if you select the use account numbers, notice it’s not the default over here is the default. And other words, not having account numbers is basically the default.

2:03

If you’re if you use account numbers, they can be very useful because they give you a lot more control in the ordering of the accounts that you have. However, if you do not have experience with account numbers, and you put account numbers and you don’t understand the ordering system, you can really kind of muddy the waters and make things not not good. And therefore, if you know about account numbers, you can put them in if you’re not, you can put the default and it will order the trial balance the way we have seen it previously, that being by basically account type assets, liabilities, equity, income and expense and the subcategories of those including cash, accounts receivable, types of assets, and then the other current assets and so on.

2:43

And then within those categories, those types, it’ll order by alphabetical order. So that’s where the control could happen. If you don’t want it order by alphabetical order. Within the account types, you can use the account numbers. So we’ll discuss that a bit more detail later, we might do a presentation simply on accountant numbers show the control that they can add. But for now, we’re not going to include them.

3:04

And then we have classes use class tracking for transactions. This could be a great tool for some types of things. If you want to if you want to group things separately for class tracking, it could be very useful for things like job tracking, if you’re going to class different jobs, or different segments or different regions. There’s various uses for class tracking, we may put some presentations later on when you would use class tracking. But by default, typically, most companies don’t need the added feature.

3:32

That’s why By default, the class tracking is not included, we’re going to keep that they’re automatically assign at general journal entry numbers. So when you make a general journal entry, like the debits and credits, it’ll automatically basically assign a number to it. That’s basically a useful practice to have, therefore, we will keep the account setting they’re worn when posting a transactions to retained earnings.

3:57

Why would it do that retained earnings is an equity account. So the equity account is an account that usually is only used when something is closed out to it, such as basically the you know, when you close out the income statement to it, net income is going to close out to the equity assets, liabilities, equity.

4:13

So it’s unusual, therefore, to post things to the retained earnings. So it’s saying, Hey, we’re going to tell you that you’re doing something a little bit unusual, we will from time to time post something to a retained earnings type account, and we’ll see this warning pop up, I’m going to keep it there, however, so that we can, you know, see that it will pop up and say, hey, that’s okay. When is it? Okay? When is it not?

4:34

Okay, so it’ll it’ll give us that warning, then we have the date warnings. So Warren, if transactions are 90 days in the past, Warren of transactions are 30 days in the future. Now, this is a great tool, if you’re working in real time, if I’m putting my transactions in daily, or you know, within the same month, then of course, it’s very possible that you someone can miss key, put the wrong date the wrong year, and now you got something posted totally in the wrong period. And that’s not good, right.

5:03

So it’s really nice to have these saying, hey, you posted something way out of the range. And so you want to change that. Now you could increase the range if you’re if you’re lagging in your posting. And therefore, and you know, you don’t want to have a big mistake, like post the wrong year. So you might up these ranges, to make them larger. If you’re so forth. For example, if you’re doing bookkeeping and someone gave you something, and you want to enter all your data for the whole year, or if you’re a business owner, I know no one, this wouldn’t happen anybody here, right.

5:32

But if you if you had no bookkeeping for the entire year, and you wanted to put together the whole bookkeeping for the whole year, because you need to do your taxes at the end of the year will then the 3090 range isn’t going to be helpful, because you’re going to be going back to dates way past that. And it’s going to give you a pop up every time you do that.

5:50

However, if you wanted to say, hey, I want to be within a year’s range, you could just increase these ranges. And that might help you from at least putting in a day a year that’s completely wrong. In this practice problem. Because we have to work in the past or the future, that we’re going to remove the date ranges because if you’re working the problem, I don’t want you to get have this pop up screen happening all the time. So again, very good in practice, not good. If you’re working far in the past, you could change the ranges.

6:22

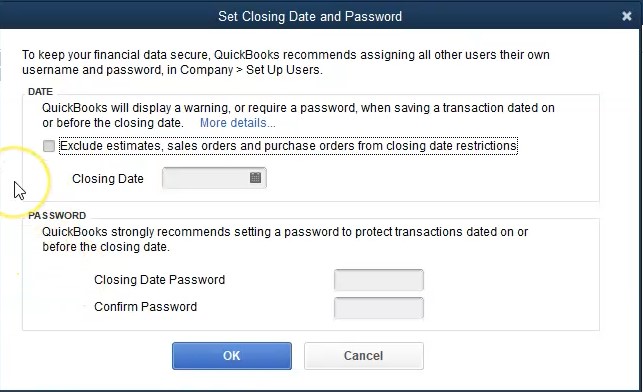

However, if you’re working at a future or past date, for some reason, these will be very annoying as they pop up all the time. And then lastly, we have the closing date, date through which books are closed that we have the set up process here says to keep your financial data secure, QuickBooks recommends assigning all other users their own username and password and company set up users.

6:45

So then we have the date, QuickBooks will display a warning or require password when saving a transaction dated on a before the closing date. And then we can include the date here and this can help us there’s a lot of the problems with bookkeeping is to say, hey, the books are closed for this period, as of now and so we don’t want any transactions to be posted to the prior period. So you could basically say, Hey, you know, close that date, give a warning. If that if that time period is closed, if you don’t, you know, things can get messed up in terms of rolling over the books.

7:14

So we’re not going to deal with that now. And we’ll we’ll mention that as we start to go through the process. And then the password. QuickBooks strongly recommends setting a password to protect transactions dated on or before the closing date. So it’s going to say hey, don’t what you’re basically saying here is that, hey, this, this period is closed, do not mess with this period or any date prior to this period.

7:35

We’re basically done with that period. And you can only do so if you have a password that can really help people from you know, going back and adjusting things or making an adjustment to a prior period which can cause problems. So we’re going to go ahead and keep that as is and then we’re going to go to I’m going to just basically say okay, and close this out and we’ll move on to the next preferences next time. If you make any changes when you say okay, it’s going to ask you to save those two inches as you do so.

In this presentation, we will set up a new company file from QuickBooks desktop, QuickBooks Pro 2020. These are going to be the icons we will be using in order to open the program, you’ll recall that we’re going to be using QuickBooks 2020. We no longer need this set up process, I’m going to remove that or QuickBooks Pro 2019. The process would be much similar for prior versions of QuickBooks as well.

0:24

Note that this is the program this is actually the program file. As we open up the desktop version, we will be creating company files in a similar fashion as you would think with Microsoft Word, or excel in that we have the program. Then we have the word documents, Excel worksheets, and we could then open up those Word documents and excel worksheets from the actual docs document or worksheet, or we can find them by first opening the program. QuickBooks is a little bit different because most people with QuickBooks will open up the program instead of going and searching out the file size.

1:00

And one reason for that is because most people only have one file unless you’re a bookkeeper do public accounting, you typically work with only one file. Therefore, if you open up QuickBooks, you expect it to go through the one QuickBooks file that you are using. However, you want to know where that file is located in case there’s a problem. And if you are a bookkeeper, you want to be very organized with where you put the QuickBooks company files because it can get confusing just like any kind of file system.

1:26

Therefore, the first thing we’re going to do is set up a file that we’re going to be putting the folder into. So we’re going to create a new company file that company will be called get great guitars. So we’re going to create a new file, and then put get great guitars here once it is created. So I’m going to make a new folders, put it right on the desktop, we’re going to call it I’m going to call it get great guitars. And that’s where we’re going to end up as having our company file once we set it up within QuickBooks, so we’re going to start the new company from scratch, we’re going to open up QuickBooks by simply double clicking the icon.

2:00

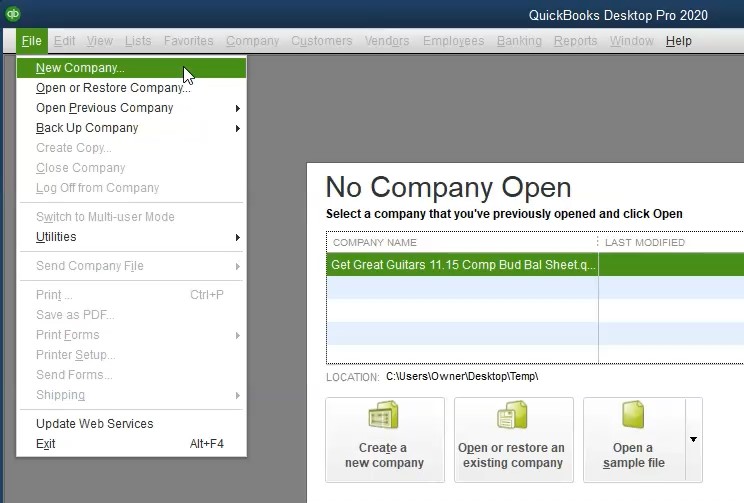

When we open up QuickBooks, it’ll typically open up to this screen, older versions will typically often go right into the company file that you had previously opened. If that is the case, you can go to the File tab and you can close this the company file that you are in, or we can actually just go to new company file without even closing the company file we’re in. Recall that this file here is only showing the recent items that we have been in. So once again, if we only work with one company file, it’ll typically be listed here.

2:29

And we can use this quick search field to go into it very quickly. However, if we have multiple company files, then this field may not show all of them because we haven’t been in there recently. So you want to know exactly where they are. Even if you only use the one file, you really want to know where it is located on your desktop on your computer. Because if there’s a problem with the system, and then you don’t know what, then you have to go and actually search for the file, I could actually be a little bit confusing.

2:56

So you want to know where the QuickBooks file is. And this field doesn’t really show you exactly where it is. And so you don’t really want to depend on that. So just be aware of it. This is not the file that we will be using, we’re going to create a new company file from scratch. Now if you look at the screen down below, you could use this icon which says Create new company file. The other icon open or restore. If you had to wanted to restore a company file or open an existing file, or open a sample file which are useful to us within QuickBooks as well, we do have the feature now find a company file, which makes it a little bit easier now to find those company files within the system.

3:36

You know, QuickBooks default settings to save the company files were a little bit strange before it would kind of put an under the C drive and under like five folders down under an Intuit type folder. So it’s nice to have this icon here, which will help you to locate QuickBooks files as well, we may review that icon later. Now I like to instead of using the Create a new company file here, go up to the File tab up top, which has the same option.

4:04

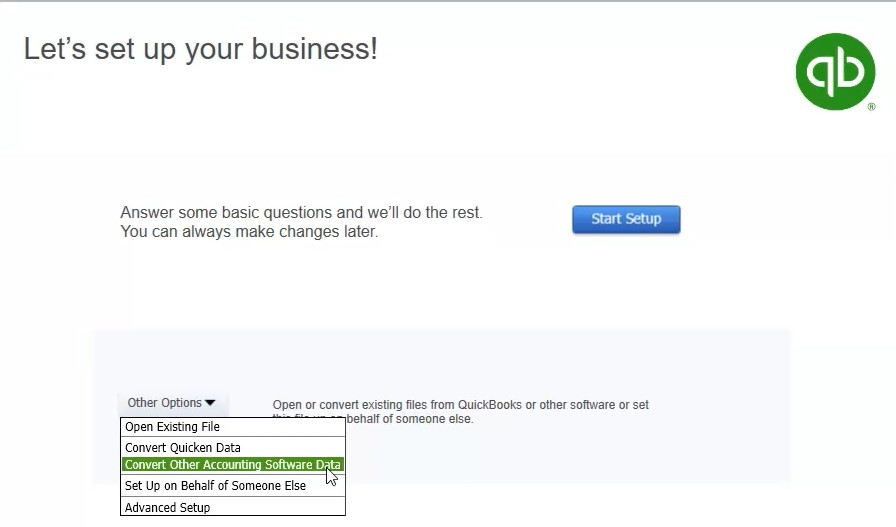

The reason I like it better is because if I have some other window open, and I don’t see this window, then I could still open it, you can open it from any window, I can go to the File tab, and we can go to new company. So that’s what we’ll do here file new company. Then QuickBooks says let’s set up your business. So we have the answer some basic questions, and we’ll do the rest. So you can always make changes later.

4:27

So we’re going to start here note, you have some other options. And if there these are some other options that are applying typically, if you already have some accounting in another system, there may be some options to import some of that data from a prior system. So open or convert existing files from QuickBooks or other software or set this file up on behalf of someone else. If that’s the case, then you can go into some of these open existing file.

4:54

Obviously, if we opened it and existing file, we would have done that from a previous setup just to open an existing quick QuickBooks file convert Quicken. So Quicken is another Intuit product very similar to QuickBooks designed more for individual and investment tracking. So you may be able to then convert the quick in data to QuickBooks data, and then be able to save some data input in that case, converged other accounting software.

5:20

So if you have some other type of accounting software that you want to import, instead of starting from scratch in QuickBooks, you probably want to consult with a CPA or a bookkeeper to think about whether or not you want to convert that or just start from where you are at at this point in time, set up on behalf of someone else and advanced setups. And so we’re going to go through here and start this simple setup, the basic setup the advised set up and then we’ll go back into the file. And we’ll make some more adjustments in terms of the chart of accounts, adding new accounts in adjusting the preferences.

5:56

QuickBooks, then once I sign in, you’ll enter your email address will use this email address to see if you have an into an account. But it’s kind of their checking feature. Next, we’re going to enter the company data. So the company data, everything that has the Asterix here, the red mark, those are things that are going to be a required field.

6:16

Now note that not all the fields are required, if you’re going to be using this bookkeeping system, and you’re going to be using it in order to give invoices to customers and whatnot, then you’re going to be wanting to include things of course, like the business field and the EIN number and all of that kind of data.

6:32

If you’re just simply using it for bookkeeping system to track your bookkeeping and you’re not providing that type of information to third parties. And or and or if you just want to test the system and work through the system, then of course, all you need is really the name, the industry and the business type, you need the name because that’s going to help QuickBooks to say what company file it is, it’s going to save the company file under the name, it wants the industry because that in the business type, because these things are going to help QuickBooks to customize the set up for you, it’ll try to customize the chart of accounts for you so that you can set them up.

7:09

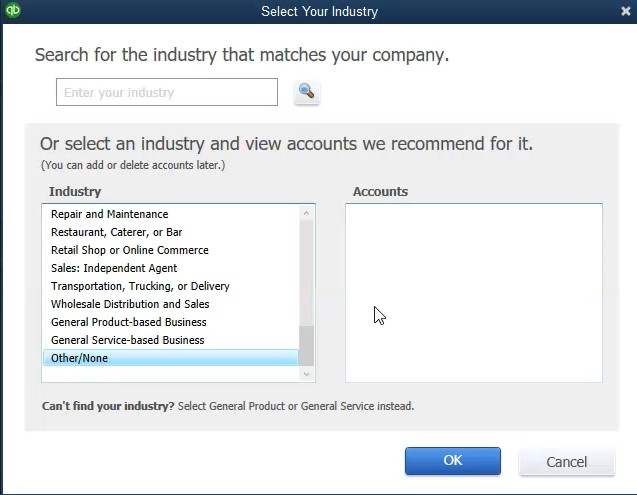

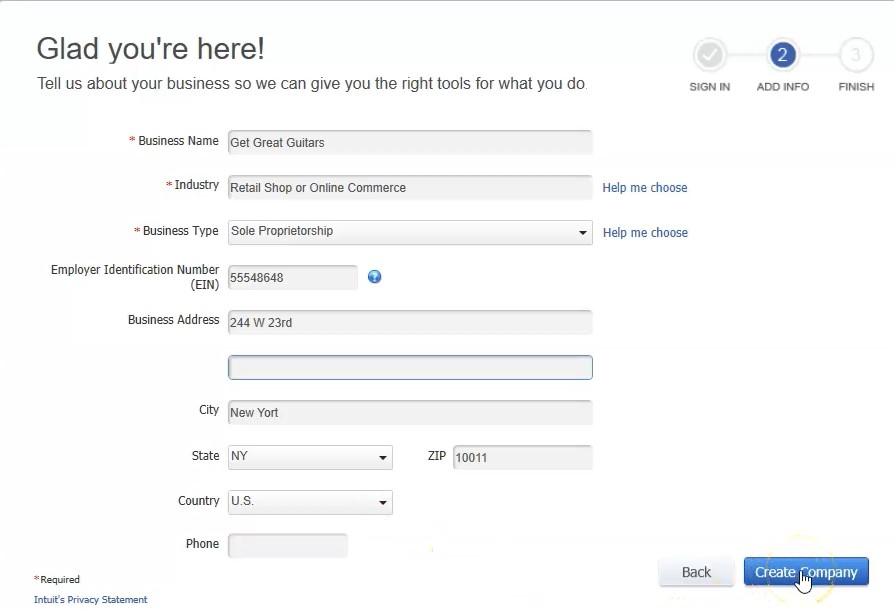

So these three are the ones that you’re going to have to have in order for QuickBooks to do anything to set up a company file. In other words, if you don’t have an EIN number, or you don’t want to put an EIN number for whatever reason in the system, you could still set up the file, but you would want the EIN number, if you were to issue something like 1099, same with the address, and so on and so forth. So let’s go ahead and put put in this information, our business name is going to be get great guitars there Here is the get great guitars, then we’re going to go to the industry, we could use the help me choose item for the industry.

7:45

Now note that these items are the things that are going to help QuickBooks to set up things like the chart of accounts that I’ll give you kind of a default chart of accounts to work with, which for most people is useful. However, for some people, you might want to customize your own Chart of Accounts. So therefore just keep that in mind. So if I go into the Help me choose, we have the industry selections we can have these are going to be the basic type of industries.

8:07

Again, if you don’t want any Chart of Accounts over here, at like, you’ll notice that if you select any industry, it gives you basically the accounts it says, hey, these are the chart of accounts that’s kind of common to this industry. These are the chart of accounts that we’re going to set up for you, they will automatically be there from QuickBooks by setting it up, if you say hey, I don’t want a chart of accounts, I want to do my own accounts, I want to set up my own stuff to customize it for myself, then you can go down to the other tab down here, no Chart of Accounts. And you could just basically started from scratch, it’ll just give you a couple basic accounts that are pretty much mandatory for any kind of industry.

8:42

Most people will want to basically choose an industry here and most of these industries will be something that fit most people, you want to have that chart of accounts that’s going to be set up for you. Because then if you’re not really familiar with accounting, you can kind

8:58

of use the chart of accounts as a deep in other words, you can think about when we record transactions, is it on the chart of accounts, is there something on the chart of accounts, if it is basically use that as the default, because QuickBooks is saying, hey, that’s the industry standard. And if it’s not on the chart of accounts, then you can basically add new accounts as you go. So you can always add new accounts.

9:20

But if you have some concern about what’s industry standard, what’s the norm, then then, of course, you want to choose the chart of accounts here. And that’ll really help to guide most people, we are going to be choosing a retail shop or online commerce. And as we do this, then it’ll see the chart of accounts on the side over here and we can kind of review through them. The main thing we want is, is that if we’re a service company, we’re not going to have things related to basically the cost of goods sold basically inventory type of items.

9:48

If we have inventory items, which we want to look at with our example problem, because they can make things a bit more complex. And then we are going to need things like cost of goods sold and the tracking of the inventory. So we want to pick something that will have that we’re going to have the retail shop and the online commerce, we will be considering items of inventory as well as service transactions when creating our bookkeeping system.

10:13

So we’re going to say, Okay, next we have the business type, what’s the business type that we have set up once again, we have the drop down, or we could go to the help me choose center, if we go to the help me choose, we have the business setups. Now these are basically the business type entities that we have.

10:30

Most people when they set up a very small business, they’re going to be a sole proprietor. In other words you haven’t Incorporated, you haven’t set up anything that makes the entity basically a separate entity from yourself or a pass through type of entity. That’s what we’re going to choose here.

10:44

Now you could be a partnership or LLC. So that would basically a partnership would mean that you have two people that would be involved as the owners, an LLC is a kind of limited liability type of partnership. If you have questions on which of these to set up as an terms of your legal entity, you want to consult an accountant or a lawyer on that. And then we have the LLC could be a single member or multiple, we have the corporation. Most small to mid sized companies are not c corporations, they may be typically S corporations more likely a pass through type of entity, not for profit organization or other.

11:22

Once again, we’re going to choose the sole proprietorship here, most of the accounting kind of basics and fundamentals within QuickBooks will be much the same with these different types of entities. The major difference being with the equity section, you know, when we have the partnership, we have to think about two partners and breaking out the equity. So we’ll discuss that a bit as we go.

11:42

So we’re going to say okay, and then we are going to put an EIN number and address because we do want to look at the documentation for recording transactions that we would give to somebody else such as invoices and other types of transactions. The EIN number is an employer identification number, this is a number from the IRS. Now you would think you would only need it if you had employees. But that’s not necessarily the case.

12:08

Because anytime you have a business transaction where somebody wants to identify you with something other than just the business name, they typically need a number, obviously, the IRS thinks of you as a number, but other people think of you as a number two when they have to deal with the IRS. So if you had to give a 1099 or something like that, or someone needed to give you a 1099, then you have to give them some type of number, if you don’t have an EIN number, you got to give them your social security number, which you know, that’s not the best thing to be given out most of time, right?

12:36

So you want it so an EIN number might be something that would be useful for pretty much any any business, you can go to the irs.com, website irs.gov, IRS not not IRS. com, irs. gov. GOV and look at the process for the EIN number. And then we have the business address, this is the address I’m just going to use for the example problem.

12:58

So here’s the address that we’re going to use zip code. And the country this kind of stuff, of course, will be showing up on things like invoices that we will be sending out to the clients to the customers. So then we’re going to create the company file, we could actually select the blue item creating the company file now. And my my EIN number is not formatted correctly. So let’s I think I’m missing an eight, I’m missing a digit, which for me, I’m going to add an eight. So I’m going to say all right, there’s the added eight. And then I’m going to say create.

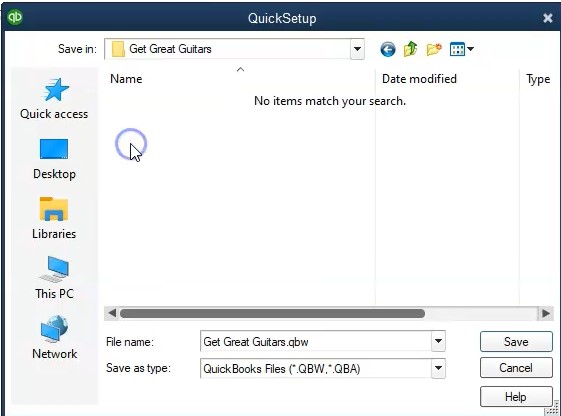

13:29

Now QuickBooks is going to say Where do you want to put it. So we have to create the company file. So this is where we’re telling QuickBooks Hey, this is where we want to create the new company file. So whenever we go into it, we’re actually opening up a company file here. So we want to go to the folder that we just set up, which is going to be the get great guitars. And that’ll be here. So get great guitars, hearts a little bit messy on the desktop here. And then I’m just gonna keep notice that name, get great guitars, you’ll notice it’s a QBW file

13:56

as a quote, as opposed to a QBB type five, which will be about backup type file. And so here’s the QuickBooks file, type the QBW. So I’m going to go ahead and say save, it may take a little bit of time to set up the company file. So be patient be calm, it’s setting up the company file that’s been updated. Now we get this little pop up screen, which says QuickBooks desktop usage and analytics studied into it, we work continuously to improve our software and provide you with the best possible product service and experience.

14:28

One way we do this is by tracking QuickBooks desktop usage, QuickBooks is a web enabled product. When you’re connected to the internet from within QuickBooks, in addition to delivering product updates, messages, service information, and help content, we also collect data about you and your use of our software. This helps us see where our software is effective. And what Intuit services help you manage your business most effectively learn more about the data we collect.

15:01

So they’re basically saying, Hey, we’re tracking the usage of QuickBooks to some degree, it should just be for business, you know, analytics use, hopefully to help the software to improve. So I’m going to say all right, continue. That before we get into the software, QuickBooks, once again gives us another kind of upsell in type screens and other types of things we may want to purchase related to QuickBooks again.

15:22

So keep everything in one place with QuickBooks desktop. So you got to get paid faster type of center for for a payment setup, we have once again the payroll that they’re saying, hey, do you want payroll information, once again, that would be an added cost to learn more about that. And then we have the checks and supplies Do you want to have checks and supplies that would be pre printed that typically types of things that would go along with the QuickBooks systems such as checks that which you can print out through QuickBooks, we’re going to say no here, and I’m just going to close it up here.

15:51

Or you could say start working down below, I just kind of x these things out, typically, as long as they get out there. Now again, before we’re actually in the software system, QuickBooks has a other basically pop up that it’s happening before we’re in the system. And this includes things like the new feature tour will discuss a bit about the new features, you know, this is going to be the new features since basically last year that we had, and we’ve got the invoicing, we’ve got the reports, we’ve got the help support and file management, we’re not going to go through all these. Now just note that you could take a look at those if you don’t want to and you want to get straight into the work, then once again, you’re going to close this screen out.

16:29

And then QuickBooks desktop will typically default to our good old home screen here on the left, you see the home screen on the left. Now typically, I like to see on the left the open windows. So what I do whenever I start a new company file, or whenever I open it, I then go to the View tab up top, and I go to the open windows list. So then I could see the open windows, which in this case is just the Home tab.

16:52

So of course the Home tab is going to give you that flowchart, you’ve got the vendors, you’ve got the customers, you’ve got the employees, that’s basically our default kind of setup, this will help us to basically enter data fairly easily. The other thing we want to take a look at that we selected as we set up the file is going to be the chart of accounts. So to get to the chart of accounts, I typically you could go to the chart of accounts here and the company data, I usually use the drop downs to get to the chart on account. It’s a format of lyst.

17:21

So I’m going to go to the lists up top and go to the chart of accounts, what are the accounts that we will be using, whenever we do some new thing that will be set up, we’re gonna have to let name and account in some way, typically, and these are going to be the chart of accounts that we will be using. So notice QuickBooks set these up for us, we didn’t have to do anything, they set up the chart of accounts how based on the industry that we put in. So based on the industry saying that we’re going to be basically selling kind of inventory, we have the chart of accounts. So we have and notice the order of the chart of accounts, it’s going to be in order by in essence type. So the type is going to basically be the accounting equation, right assets, liabilities, equity, and then broken out into more detail, the assets would be current assets, which we don’t have any yet, we’re gonna have to add some.

18:06

And then we have the property plants and equipment or fixed assets, then we have the other assets. And then we have liabilities, which is going to be the current liabilities, and then the equity section. So assets liabilities, equity, then income type accounts, revenue type of accounts, and then Expense Type of accounts that it’s going to be the order that the accounts will be set up in our default then will be typically, when we add new items, when we start to enter things into the system,

18:36

we’re going to say, Hey, is there an account already set up that would line up to the new thing that we are putting into the system, the new bill, the new check the new payment, if there is we’ll just simply use that account, because that’s typically going to be the default account for the industry that we are in.

18:52

If there is not, then we’ll consider adding a new account. So you want to be careful adding new accounts because they can get kind of long and messy. So you’re going to you what you want to basically that’s the system that I would basically put in your mind is it you know, put a new thing in there is there an account already selected that would go along with this one, if there is great if it seems like there’s you’d like a new account to track this out separately, then make a new account, just don’t do it, you know, be don’t do it every time make a new account for every transaction.

19:21

You’ll note, of course that we have the merchandise sales, because we said we’re going to be selling the inventory. So that’s going to be one of our key accounts, we’ve got the cost of goods sold, we’re selling inventory. If we did not sell inventory, if we said we were a service company, then we probably wouldn’t have those items. Down here in the income type section, it might name then the revenue or income type of accounts some other name. If we would like to change the name of these accounts, of course we can, we can call it revenue, we can call it some other sales item. If we if we choose to.

19:54

We’ll go through some of those options as we move forward and future presentations. Also note that if you click QuickBooks and you open it back up, it will typically require you to have a password. So if you want to put the password in proactively will do that. Now note that it will typically require you to have when you want to make sure that you know where the password is, it’s not as easy to recover the password here as it is with other types of things. So don’t just put in a password and say well, that’s okay, I could recover it later.

20:22

If I forget about it or something like that just to push forward, make sure you write it down it’s not as easy to recover the password. So the where you go for the passwords as you go up to the company drop down up top, you’re going to set up user preferences and passwords and you want to change your password because I’ve already set one up so it says change the password. And this would be the screen where you would enter the password. The recommendations that I believe these are the minimum requirements actually are to have seven characters including one number and one uppercase letter.

20:53

So make sure to put that in there our password for all the files that we will be working with in this practice problem will be GGG 1234 get great guitars GGG 1234 any file you open up here will typically need that password if you use one of the backup files related to this problem.

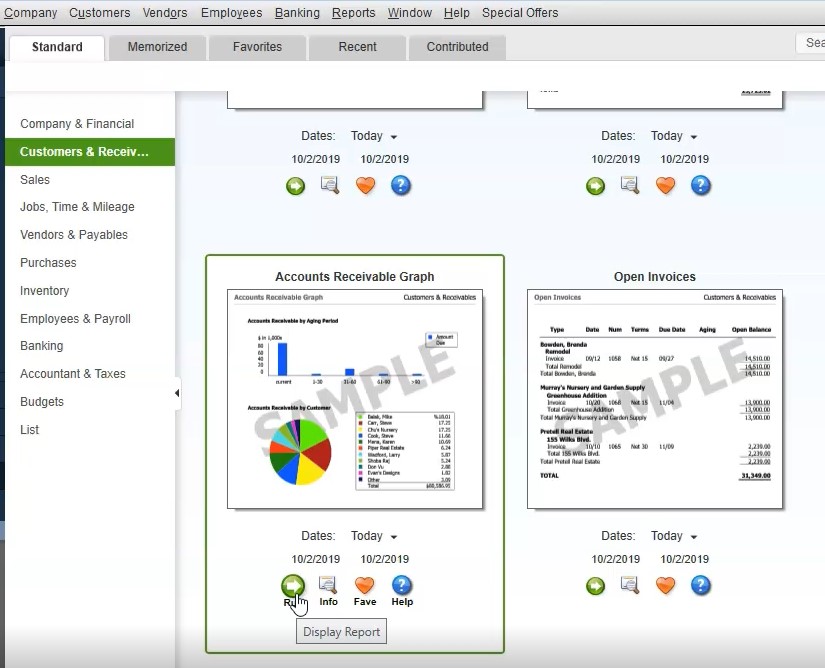

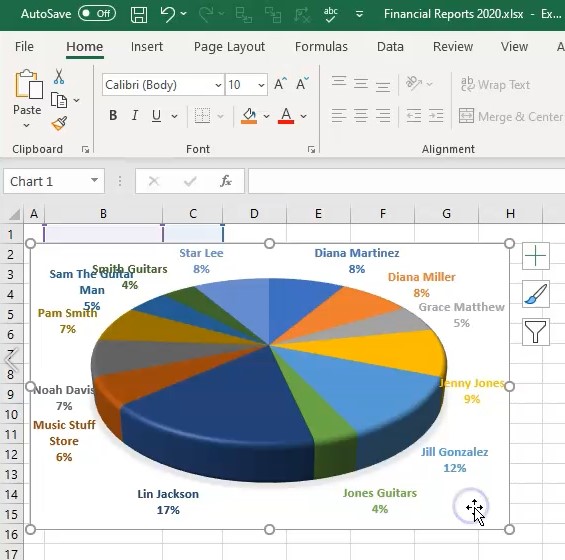

In this presentation, we will create an accounts receivable graph within QuickBooks Pro 2020 QuickBooks desktop 2020. Here we are in our get great guitars file we currently have the open windows open, we can open the open windows by selecting the view drop down and the open windows lyst.

0:18

We’re now going to be considering an accounts receivable graph whenever we think about any graph or report, other than the major financial statements balance sheet and income statement, we want to consider what account and which of those financial statement reports are going to be supported with the report or graph we are running. In this case, accounts receivable will be a balance sheet account.

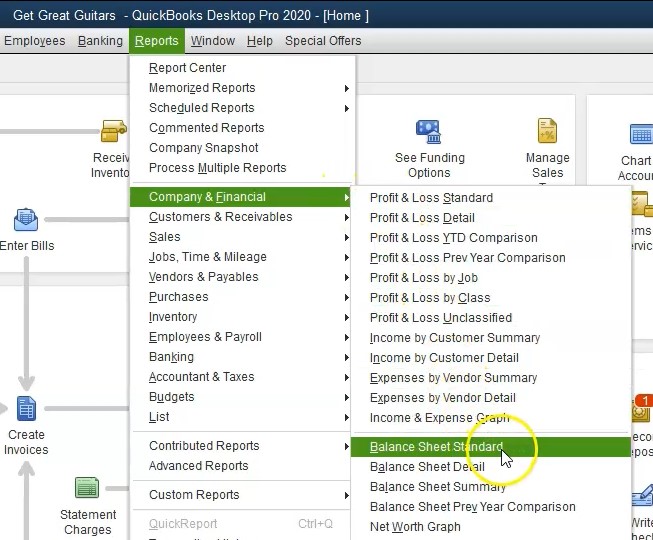

0:38

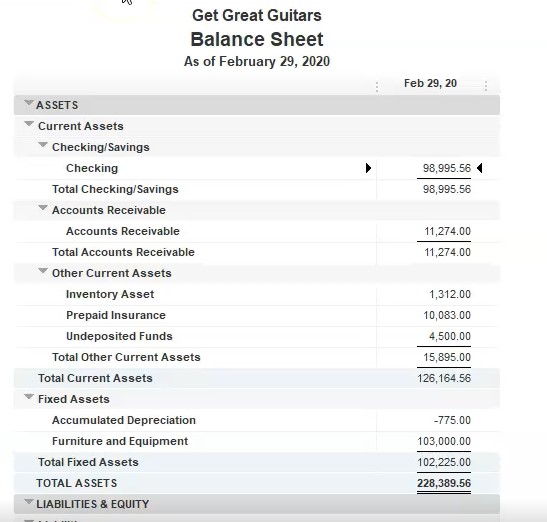

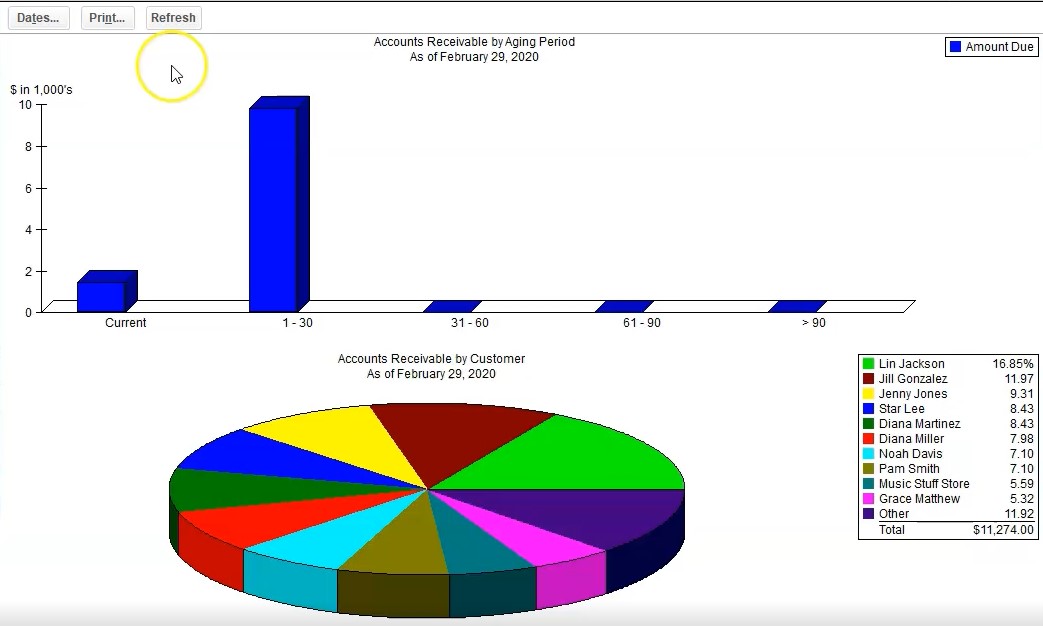

Therefore, let’s first open the balance sheet we’re going to go to the reports drop down up top, I’m going to go to the company and financial and scroll on down to that balance sheet standard report the balance sheet standard report we’re going to take the date as of Oh to 29 to zero in February. Remember the balance sheet is as of a point in time accounts receivable is of course, right here that represents money that is owed to us by customers. So now we want to think about the accounts receivable report, which will break out what is owed to us by customer.

1:08

Also note, we could run another report that would help to support this detailed that being Of course, of report we’ve seen in the past reports drop down. If we go to the customer and receivables we’re looking at the customer balance Summary Report. And that will give us our customer balance information. And in a summary format, we’re at 10,009 74. If I change the dates up top 202 29 2020 229 to zero, we’re at the 11 to 74. If we go back to the balance sheet, we’re at the 11 to 74.

1:44

Next, we’re going to run the graph, a couple ways we can get there, we can go to the reports drop down and we can go to the customers and receivables and find the graph here. Or we could use the report Center by going to the reports drop down and the report center. So let’s go into the report center. We’re in the standard tab, I’m going to maximize the sheet by selecting the maximize tab here. And then on the left hand side, we want the customers and receivables within the customers and receivables.

2:12

I’m going to scroll down till we get to our graphs. Here’s the accounts receivable graph, we can run the report, we can change the dates on the report I saw I choose I usually will simply run the report so I’m going to run it, then we’ll change the dates on it, nothing’s here. Is it a date problem? Yes, it is we’re going to go back up top and change the dates for it.

2:32

Change the date to go to 20 920 noting once again that it’s going to be at the end of February. And there’s only one date because it is as of a specific point in time, how much do people owe us who owes us as of this point in time, we have the key to the right, which is going to be listing the people that owe us which are going to be customers. And then of course, the graph in the middle of the pie chart for us the total been adding up to the 11 to 74 that then matching what’s up on the balance sheet back to the balance sheet, we see the 11 to 74. If we go back to our graph, then we can take this number note we can create this graph.

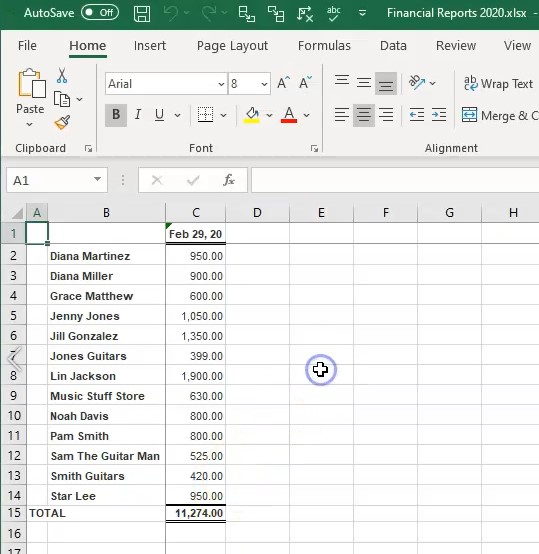

3:10

How is this graph created? Well, if we were to take the customer balance summary report back to the customer balance summary in the open windows, export this to excel, we can see how to basically create this graph in Excel if you want to use that and make your own graph and make it a little bit more flexible in that format. Let’s do that. And then we’ll copy and paste the graph from QuickBooks and see how we can use those items as well.

3:35

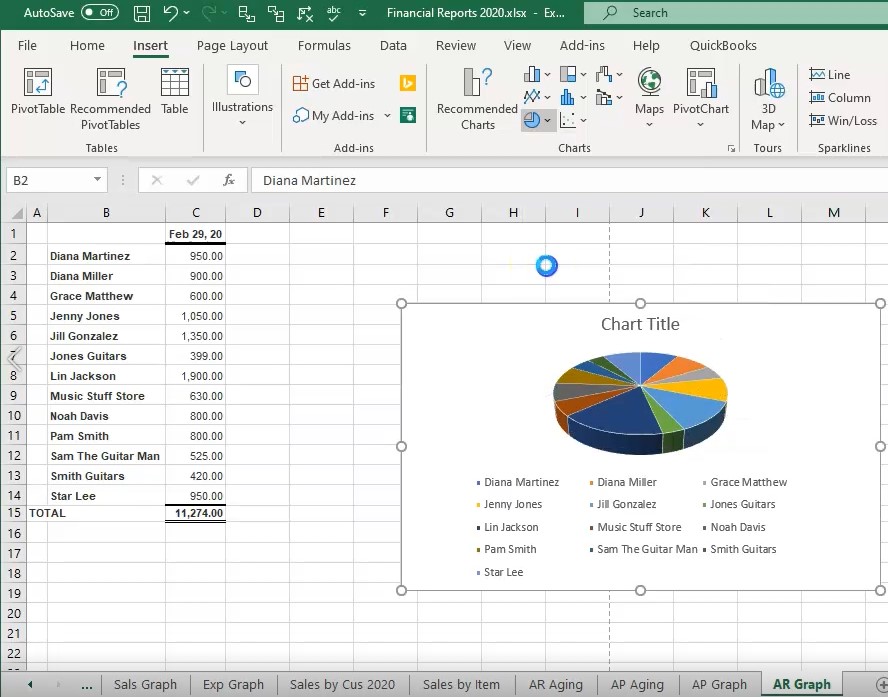

We’re going to go to the Excel laptop, we’re going to create a new worksheet, we’re going to put that new worksheet into an existing workbook when we have created in the past, and we’re going to select the browse, there’s the workbook we want going to double click on it, we will then export to in here is our Excel worksheet, we’re going to do our normal kind of formatting, I’m going to go all the way to the left, we’re going to click on this screen with the instructions, right click on it and delete it, then I’m going to say delete, I’m going to go all the way to the right, then I’m going to pick up this new sheet, I’m going to pull it all the way to the right, I’m just going to drag it left clicking on it to the right, then we’re going to do some formatting in the Page Layout tab, I’m going to go to the Page Layout View, I’m going to say okay, we’re going to go to the View up top so we can remove the splits there, I’m going to go to the View up top windows group and remove the splits, I’m going to double click then on the name, I’m going to call this and ARAGR graph, let’s just say accounts receivable graph, that’s what we’re going to be making from this. Now note, we might want to read rename the title up here, like I haven’t done in the prior ones, this is going to be a bar graph, you know, and that’ll be on the title.

4:46

And then I’ll go back over here and back not there, but back here. And then we need to basically make our graph. So all I have to do is highlight these numbers, then go to the Insert. And then we go to go, we want a pie chart, we’ve been making these 3d pie charts. So we’ll make that one. And there we have it. So that’s another format. Another way you can make the graph, you could rotate the graph, you can put a name up to up top, or you can delete it, you can then put the percentages into it if you if you so choose by formatting the graph.

5:17

So for example, if I chose a different format, it might it’ll look something like this, we could put the percentages in here again, you’d have to mess with it to get it, you know, to look as nice as you would like it. Let’s go back up top and go to the the first one here, I’m going to go back up top and select this one here. And then we can adjust these around and make this look as nice as much nicer. But there’s a lot of different formats, we won’t go into all the formatting in Excel here. But in any case, I’m going to put this down below. So we’ll put it below the data.

5:48

Now also know you might want to hide the data in some way, if you don’t want to print the data, like there’s a couple ways you could do, you could try to hide the data or you can even you can just hide the font, even if I was to select all of this information, and go to the Home tab, and then go to the color of the font and make it say white. And then I can I can remove basically, I don’t even need this top number, right click here and delete. And I don’t need the total. So I can get rid of that formatting, right click and delete.

6:19

And then you can basically put your graph right on top of the data. And then and then you can actually print this report without, you know showing the data but just showing the graph if you would choose if you so choose to. And then I’m going to put the graph from Excel right underneath it or the graph that we’re going to copy from QuickBooks, let’s go back to QuickBooks. Here’s our graph there, we’re going to go back to excel, just insert that by going to the Insert tab, we’re going to go to the illustration, we’re going to go to the screenshot, and then I’ll take a clipping of it.

6:49

I’ll take a clipping of this graph. So we’ll just pick up that graph. There it is, and then I’ll take a clipping of the key. So I’m going to go below it, I’m going to go to the illustration, going to go a screenshot, we’re going to take a clipping then of the key. So here’s the key will take that up, and that’ll be right below it. And so there is that. So that looks pretty good. Now we’ll print this entire thing to a PDF file will go to the File tab up top, we’re going to go to print, and then we’re going to print it to a PDF file, we’re going to save the existing the entire workbook, we want the entire workbook, which is going to be including 20 pages now, then I’m going to go to the printing up top.

7:30

And then it’s going to be printing those 20 pages, we’re going to see where it wants to go. And here is our dialogue box, we’re going to go into financial statements, I’m going to call this actually, we’re going to be putting this into here, I’m going to double click on the financials, and say save. Yes. So there we have that, then I’m going to go back to QuickBooks, and I’m going to print this one. So we’re going to go to the reports, I’m going to go to the printing up top, we’re going to go then print it to a cute PDF printer and print this item.

8:09

It’ll then get a give us the printing dialog box. We’re going to put this into the financials, and I’m going to pick I’m going to name it then the counts, let’s say accounts receivable graph. There we have it, and then we’ll save that there. And then let’s see what we have in our folder. If we go to section one through four, within I’m going to delete this bottom one, we don’t need that.

8:37

If we go into the financial reports, then we have all these financial reports that we could then put on an email, we could zip it, I could right click on this and zip the files so that we can then send just that zip file in an email or we can send the Excel worksheet, or we could send this PDF file which has everything included in one PDF file so far that we done which includes the balance sheet, the profit and loss, the comparative balance sheet, the summary balance sheet, the income statement, the comparative profit loss, vertical profit and health, vertical analysis, grasp of the expense and sales.

9:17

And then we have the sales by customer summary. We’ve got the sales by item, we’ve got the accounts receivable, we got the accounts payable, aging, then we have a graph, then we have the vendor balance. And then now we have the accounts receivable graph here. Again, we could probably format these graphs a little bit nicer. We certainly don’t want this on the other page here so we can get rid of that. But we won’t go into a lot of detail here. That’s just an example of how you can basically format these in different fashions.

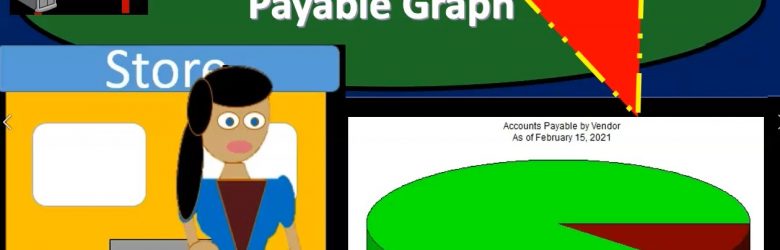

This presentation we will create an accounts payable graph within QuickBooks Pro 2020, QuickBooks desktop 2020. Here we are in our get great guitars file, we currently have the open windows open, you can open the open windows by selecting the view drop down and then the open windows lyst.

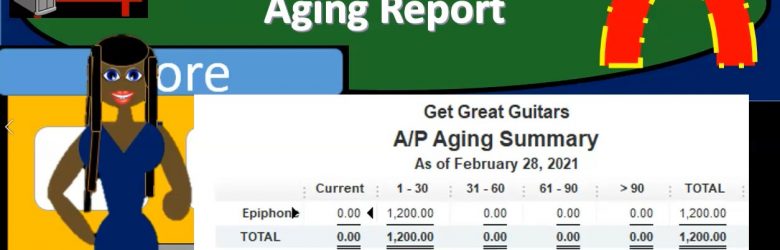

This presentation we will generate analyze a print and export to Excel and accounts payable aging report within QuickBooks Pro 2020, QuickBooks desktop 2020. We are in our get great guitars file we currently have the open windows open, you can open the open windows by selecting the view drop down up top and choosing the open windows a list. We’re now going to be considering an AP or accounts payable aging report.

This presentation, we will create a sales by item report within QuickBooks Pro 2020, QuickBooks desktop 2020. Here we are in our get great guitar file, we currently have the open windows open, you can open the open windows by selecting the view drop down and the open windows lyst. We’re now going to be creating a sales by item summary.

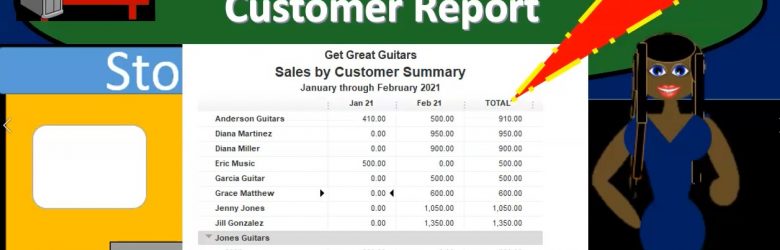

This presentation we will generate analyze Export to Excel and print a sales by customer report within QuickBooks Pro 2020, QuickBooks desktop 2020. Here we are in our get great guitars file, we currently have the open windows open, you can open the open windows by selecting the view drop down and the open windows lyst.