In this presentation, we will discuss measurement period and contingent considerations within an acquisition process, get ready to account with advanced financial accounting. At this point with the discussion of the acquisition process, you’re probably thinking, Okay, I kind of see how this fits together. I’ve see how this works. But logistically, it could still be a little bit tough. If you were to apply this in practice, you’re probably saying, Hey, there could be some problems. In practice. If we were to apply this out. For example, if we’re saying, okay, we’re going to revalue the assets and the liabilities. And we’re going to value the consideration we’re going to make a comparison of the value of the assets and liabilities to the consideration that’s being given for the company that in essence is being acquired in the acquisition process. Well, then what about that valuation process? That’s going to be difficult because how do we revalue the assets and liabilities because normally, when you value something, you value it from a market perspective, which means there’s actually a transaction a sale that’s taking place. So note obviously that valuation process is going to be somewhat of a tedious process for us to go through and revalue. And how long do we have for that to take? I mean, if this isn’t happening basically instantly with regards to this process, this is going to be taking some time.

Posts with the figure tag

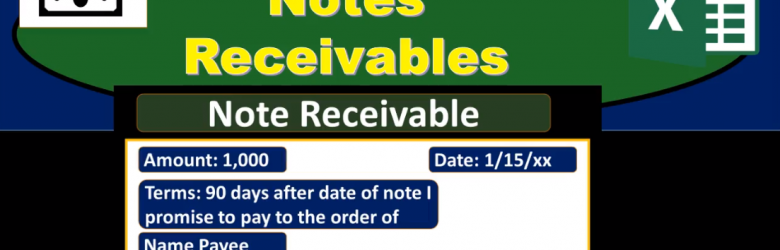

Notes Receivable

In this presentation, we will take a look at notes receivable. We’re first going to consider the components of the notes receivable. And then we’ll take a look at the calculation of maturity and some interest calculations. When we look at the notes receivable, it’s important to remember that there are two components two people, two parties, at least to the note, that seems obvious. And in practice, it’s pretty clear who the two people are and what the note is and what the two people involved in the note our doing. However, when we’re writing the notes, or just looking at the notes as a third party that’s considering the note that has been documented. Or if we’re taking a look at a book problem, it’s a little bit more confusing to know which of the two parties are we talking about who’s making the note who is going to be paid at the end of the note time period? We’re considering a note receivable here, meaning we’re considering ourselves to be the business who is going to be receiving money. into the time period, meaning the customer is making a promise, the customer is in essence, we’re thinking of making a note in order to generate that promise, that will then be a promise to pay us in the future.