In this presentation, we will discuss measurement period and contingent considerations within an acquisition process, get ready to account with advanced financial accounting. At this point with the discussion of the acquisition process, you’re probably thinking, Okay, I kind of see how this fits together. I’ve see how this works. But logistically, it could still be a little bit tough. If you were to apply this in practice, you’re probably saying, Hey, there could be some problems. In practice. If we were to apply this out. For example, if we’re saying, okay, we’re going to revalue the assets and the liabilities. And we’re going to value the consideration we’re going to make a comparison of the value of the assets and liabilities to the consideration that’s being given for the company that in essence is being acquired in the acquisition process. Well, then what about that valuation process? That’s going to be difficult because how do we revalue the assets and liabilities because normally, when you value something, you value it from a market perspective, which means there’s actually a transaction a sale that’s taking place. So note obviously that valuation process is going to be somewhat of a tedious process for us to go through and revalue. And how long do we have for that to take? I mean, if this isn’t happening basically instantly with regards to this process, this is going to be taking some time.

01:12

So how much time? You know, is it going to take to revalue all that stuff? And then basically, what what do you do in terms of that that time period? How much time do you have in order to do that, we have the measurement period period of time to ascertain fair values can be found in ASC 805 is when the acquirer obtains the necessary information about the facts as of the acquisition date. So we have the date, we’re going to set the date date of the acquisition date, and then we’ve got the measurement period, which is going to be the period of time it takes for us to basically get the information we need and you can imagine with different types of assets, it would take different things to value them of course, cash is pretty easy cash is cash. However, you know, different types of property plants and equipment, buildings and whatnot. Those things are more difficult to evaluate made need appraisals and whatnot in buildings types of situations and then limit to not exceed one year, so not exceeding one year. Now the next kind of messy topic we have is the contingent consideration. So if you think about this process when company purchasing another if there if the purchase was straight for cash, like that’s the first way we want to think about it pretty straightforward. If there was stock exchanged in it and whatnot, still not too bad, we could still figure that out. And what if there’s other types of assets and liabilities that are involved? We can figure that out.

02:29

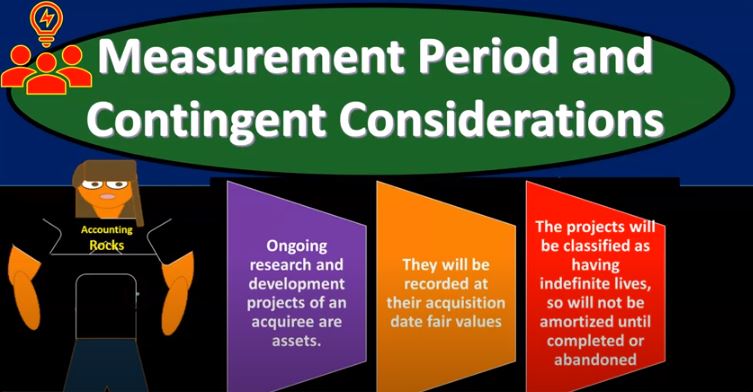

But then what if there’s a contingent consideration that’s been that’s given as part of the consideration in essence, in other words, as part of the purchase process and part of the acquisition process, well, that gets Messier as well, that makes it adds a bit of a mess to the process as well. So contingent consideration, consideration exchange and contingent on future events. So the consideration that’s being given then, is going to be contingent in some future event, which of course is an unknown. We don’t know you know, we don’t know the future of it. So continuous consideration to be valued at fair value as of the acquisition date and classified as a liability or equity. So we need to value it. So the contingent, so the contingent consideration to be valued at the fair value as of the acquisition date and classified as a liability or equity at that time. And you can see this in ASC 805. As you can see, this is somewhat consistent to contingencies dealing with contingencies in general. So we have to say, you know, normal kind of contingencies type of accounting. If there’s something like a lawsuit that’s going to happen, we got to say, we got to figure out well, is it very likely to happen, or somewhat likely to happen? Do we know what the value the valuation of this thing will be? If there’s a lawsuit in the future which is contingent on a future event whether or not we win or lose the lawsuit where you can you can, you know, kind of compare and contrast that if you have that type of accounting process in your mind. So acquirer needs to recognize every contingency they can Thumbs up from contractual rights or obligations and other contingencies. It is more likely than not that they meet the deaf the definition of an asset liability at the acquisition date for ASC 805. Now, another kind of messy component when you’re thinking about an acquisition is what about in process research and development?

04:21

So you’re acquiring a company, they have research and development that’s in process. You know, they haven’t quite, they haven’t possibly we don’t know exactly the application or what’s been made or whatnot, but it’s an in process research and development. What do we do with that ongoing research and development projects of inquiry are assets so we need to value those assets in some way. They will be recorded at their acquisition date, they will be recorded at their acquisition date fair values. So once again, we got to figure out what the fair value of that is not the easiest thing in the world, but we have to do our best to hit to value that those items as well. The projects will be classified. as having indefinite lives, so will not be amortize until completed or abandoned. So you might think, okay, if we have this research and development, we figure out, okay, it’s in process that we’re purchasing. That’s part of what we’re purchasing here. We need to value that in some way, because we’re paying for that that’s part of what we’re paying for. So we’re going to value it, we’re going to put it on the books, you would think as an asset, then it’s going to go on the books as an asset, is it going to be something that we’re going to depreciate or amortize in some way like you would for property, plant and equipment, for example, or some intangible type of assets? And they’re saying no, in this case, the projects will be classified as having indefinite lives. So we’re going to put it on the books, indefinite life, we’re not just going to apply the cost that we allocate to these items and just and just expense that in accordance with like a straight line depreciation. We’re going to say indefinite life, so will not be amortized until completed or abandoned. So either the project is completed, at which time we’ll know what the value You have something is that the research and development development that’s been, you know, completed or whatnot or abandoned at which time we say okay, it was a useless thing and at that point in time, then we’ll record that the fact that it has been been abandoned