QuickBooks Online 2021 pay bills form. Let’s get into it with Intuit QuickBooks Online 2021. Here we are in our Google search page, we’re going to be searching for QuickBooks Online test drive. And then we’re going to be selecting QuickBooks Online test drive from Intuit. It’s then going to be verifying that we are not a robot, which I don’t think is very fair. It’s like they’re saying my good buddy see, threepio is not allowed in the QuickBooks establishment.

Posts with the payee tag

Check & Expense Forms 1.28

QuickBooks Online 2021. Check and expense forms. Let’s get into it with Intuit QuickBooks Online 2021. Here we are in our Google search page, we’re going to be searching for QuickBooks Online test drive, then we’re going to be selecting and QuickBooks Online test drive. And then QuickBooks is going to try to call us a robot. Again, we’re gonna say we’re not a robot, you’re the robot, you’re you’re the robot, QuickBooks. And then we’re gonna log in there, we’re still looking at our vendor section. So if we hit the drop down over here, we’ve got the new drop down, we’re in the vendor section, we talked about, basically the accrual process, which is the entering of the bill and then the pain of the bill.

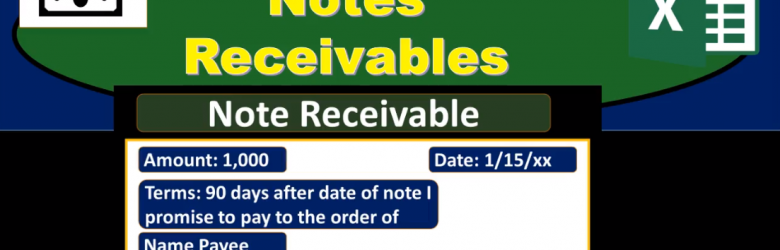

Notes Receivable

In this presentation, we will take a look at notes receivable. We’re first going to consider the components of the notes receivable. And then we’ll take a look at the calculation of maturity and some interest calculations. When we look at the notes receivable, it’s important to remember that there are two components two people, two parties, at least to the note, that seems obvious. And in practice, it’s pretty clear who the two people are and what the note is and what the two people involved in the note our doing. However, when we’re writing the notes, or just looking at the notes as a third party that’s considering the note that has been documented. Or if we’re taking a look at a book problem, it’s a little bit more confusing to know which of the two parties are we talking about who’s making the note who is going to be paid at the end of the note time period? We’re considering a note receivable here, meaning we’re considering ourselves to be the business who is going to be receiving money. into the time period, meaning the customer is making a promise, the customer is in essence, we’re thinking of making a note in order to generate that promise, that will then be a promise to pay us in the future.

Receivables Introduction

In this presentation we will take a look at receivables. The major two types of receivables and the ones we will be concentrating on here are accounts receivable and notes receivable. There are other types of receivables we may see on the financial statements or trial balance or Chart of Accounts, including receivables, such as rent receivable, and interest receivable. Anything that has a receivable, it basically means that someone owes us something in the future. We’re going to start off talking about accounts receivable that’s going to be the most common most familiar most used type of receivable and that means something someone, some person some company, some customer typically owes us money for a transaction happening in the past, typically some type of sales transaction. So if we record the sales transaction, that would typically be the way accounts receivable would start within the financial statements, meaning If we made a sale, we would credit the revenue account, we’ll call it sales. If we sell inventory, it would be called sales. If we sold something else, it might be called fees earned, or just revenue or just income, increasing income with a credit, and then the debit not going to cash. But going to accounts receivable.

Bank Reconciliation Second Month Part 2 9.15

In this presentation, we will continue on to part two of our bank reconciliation for the second month of operations, this time focusing on the decreases to the checks to the withdrawals from the bank account. Let’s get into it with Intuit QuickBooks Online. Here we are in our get great guitars file, we’re first going to be opening up some reports. So we’re going to go down to the reports on the bottom left, we’re going to be opening it up first, the balance sheet report, let’s open up the balance sheet report. And we’re going to be changing the dates up top. So I’m going to change the dates up top of the two months of operations that we’ve had thus far. That’s going to be a 1012020 229 to zero.