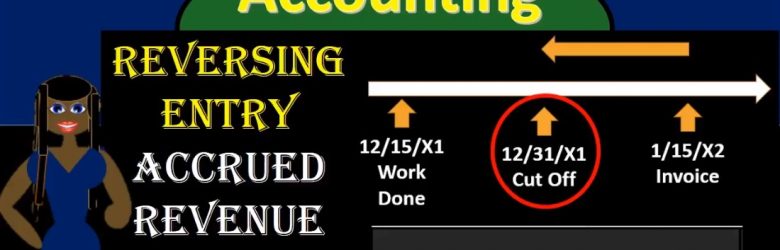

Hello. In this presentation we’re going to talk about reversing journal entries as they are related to accrued revenue. When considering reversing journal entries, we’re talking about those journal entries made after the financial statements have been generated after the adjusting process has been done. Remember that the adjusting process happens after all the normal transactions for the month have happened. Then at the end of the month, we have that adjusting process. All journal entries being made as of the same date as of the end of the month in order to make the financial statements correct so that the financial statements can be made. As of that point in time, in this case, the end of the year being 1231 that the cutoff date that the point in time that we make the financial statements, then we want to consider if we want to use reversing journal entries.

Posts with the revenue recognition tag

Cash Method vs Accrual Method 135

Whoa in this presentation we will be discussing a cash method versus an accrual method objectives. We will be able to at the end of this, define and explain a cash method, define and explain an accrual method and explain the difference between the cash and accrual methods. When considering the cash method and the accrual method, they’re not necessarily completely different or diametrically opposed. But when presented, they are often presented in this format partially because in order to explain one, it’s often useful to know the other it’s useful to be able to compare the differences between the two methods.