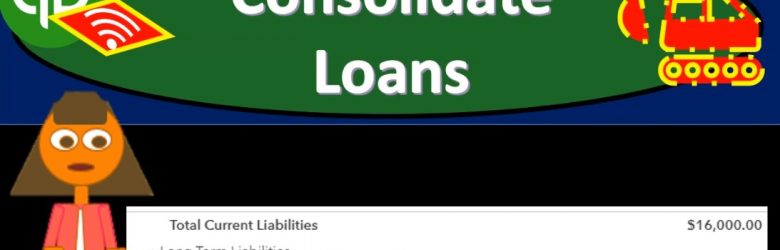

This presentation and we’re going to consolidate two loans and reflect that in our bookkeeping. Let’s get into it with Intuit QuickBooks Online. Here we are in our get great guitars file, we’re going to start off by going to our reports down below and taking a look at the balance sheet, we’re going to be opening up our balance sheet report to consider the loans that we currently have on the book. I’m going to scroll back up top, we’re going to change the dates up top from a one a 120 to 1231 to zero, and then we will run that report. I’m going to then duplicate the tab up top.

Generate Report Export to Excel 7.80

This presentation and we will generate, analyze, print and export to Excel our month in financial statement reports that’s going to include the profit and loss report or income statement report, the balance sheet report, and then we’ll take a look at that transaction detailed report that’s going to give us a lot of information to see what we have done over the month. It’s really good information that some people use for billion for the month.

Job or Sub Customer Sales Receipt 7.75

This presentation, we’re going to create a sales receipt and we’re going to apply that to a sub customer or a job. Let’s get into it within two, it’s QuickBooks Online. Here we are in our get great guitars file, you’re recalling a prior presentation, we set up sub customers or jobs, which we then created these project file with. So if we go into the project tab down below, we’ve got our sub customers for Jones guitars and Sam the Guitar Man at 305 and 402. What we’re going to do now is create a sales receipt and apply it to those sub customers.

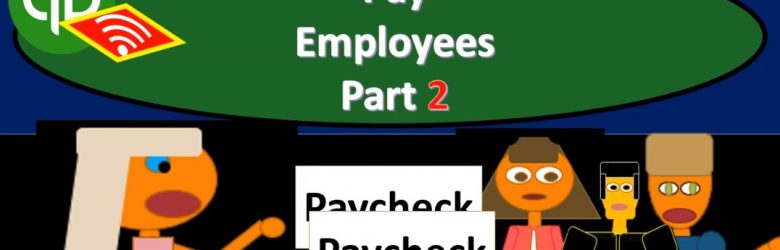

Pay Employees Part 2 7.71

This presentation and we’re going to continue on with part two of entering the payroll information into our system within QuickBooks Online. Here we are in our get great guitar system. Last time we entered our information, we’re imagining we have payroll or paychecks, basically giving us this register information. And that register information we’re going to enter into the system.

Pay Employees Part 1 7.70

Presentation and we’re going to enter payroll into our practice problem. Note that we’re not going to be processing payroll through the quickbooks online system, because that’s going to be an add on feature. We will talk more about payroll after the the practice problem has ended and its own section so you can get some more information there.

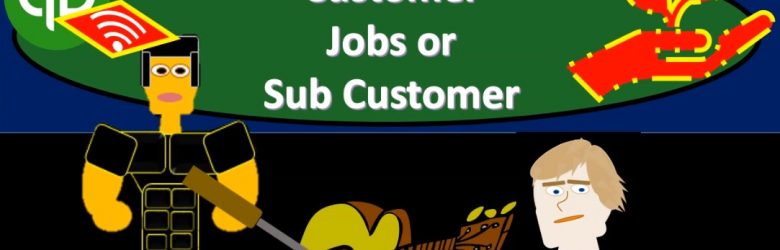

Customer Jobs or Sub Customer 7.65

This presentation and we will set up customer jobs or sub customers. In other words, if you’re working with QuickBooks desktop, people will typically call them jobs. If you’re working with QuickBooks Online, they’re using the terminology of sub customers. Let’s get into it with Intuit QuickBooks Online. Here we are in our get great guitars file. Before we go any forward, let’s take a look at our flowchart within QuickBooks desktop.

Pay Bills 7.60

This presentation and we’re going to take a look at the pay bills form. In other words, we’ve entered bills in the past, and now we’re going to be paying them using the paid bills feature. Let’s get into it with Intuit QuickBooks Online. Here we are in our get great guitars file. Before we go any further, let’s first take a look at our flow chart that’s going to be in the desktop version. So we’re going into desktop version just to take a look at the flow chart.

Enter Check & Expense Forms 7.55

This presentation and we will enter check and expense forms, we’re basically going to go through the month in kind of information or checks or expenses, we would have typical expenses such as the utility bill, the phone bill, and so on and so forth. Think about how we can enter that into the system, either as checks or Expense Type forms. If we were to actually write the check, or possibly if we had some kind of electronic transfer that would happen out of our bank account, then how would we be recording that information into QuickBooks Online? Let’s get into it with Intuit.

Receive Payment & Make Deposit 7.50

This presentation and we’re going to record the receive payment and make deposit forms. In other words in prior presentations, we recorded the invoice billing the client. Now we’re going to receive the payment for it, take those payments to the bank and record the related deposit. Let’s get into it with Intuit QuickBooks Online. Here we are in our get great guitars file. Before we move forward, let’s take a look at our flowchart. This is in the QuickBooks desktop version. And we just want to see this scenario the story that we had, as we go through it starts off with someone came into the store, they’re looking for a guitar, if they didn’t have we didn’t have the one they want and the right color.

Company Preferences Checking 6.006

This presentation, we will continue on looking at the company preferences, this time focusing in on the checking preferences, although we will also take a quick look at the bills and the calendar preferences within QuickBooks Pro QuickBooks desktop 2020. Here we are in our get great guitars file, we’re going to go back into the preferences by going to the Edit drop down up top, and we’re going to go back down to our preferences, edit and event preferences, we did the accounting last time, we’re going to be moving down from accounting will be stopping at the checking item here.