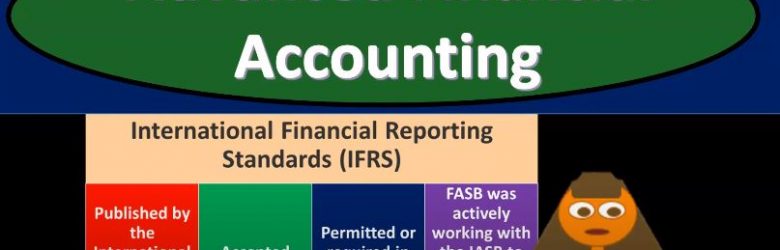

Advanced financial accounting PowerPoint presentation. In this presentation, we will take a look at attempts to converge to one set of global accounting standards get ready to account with advanced financial accounting attempts to converge to one set of global accounting standards. When preparing financial statements of global companies, accounting firms must think about differences and accounting principles across national boundaries. So obviously, if we’re a large company, and we have places of business across national boundaries, then we got to think about well, what are the accounting principles and standards in those different locations? And what are the requirements for us to prepare financial statements if doing business in you know, different countries across boundaries that have different accounting standards, differences in currencies that are used to measure the operations of companies in different countries. So again, this is something of course we have to think about it for a large company. We have places of business in our company that are across different different areas. Different countries that have different currencies, that it’s possible that we could be measuring parts of the books and whatnot in different currencies. We need to know what the standards are in different places so that we can meet those standards if we’re a large company. International Financial Reporting Standards IFRS published by the International Accounting Standards Board is ay ay ay ay SB, as the name indicates International Financial Reporting Standards. The goal here or one of the goals is have one set of standards that will go across different areas, different countries, different nations, which could make it easier to do business in different companies or across borders. So it is accepted widely the set of standards and permitted or required in over 100 countries.