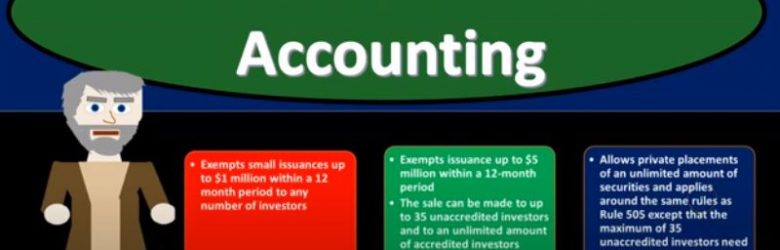

Advanced financial accounting PowerPoint presentation. In this presentation we will discuss the process of registering securities with the SEC, the Securities and Exchange Commission get ready to account with advanced financial accounting, issuing securities. If a company wants to sell debt or stock securities in interstate offerings to the general public, they are usually required by the Securities Act of 1933 to register those securities with the SEC. So one more time, we’re talking about the issuing of securities if a company wants to sell debt or stocks securities in interstate offerings to the general public, so now we got the interstate offerings going to the general public, in order to have that benefit. They are usually required by the Securities Act of 1933 to register those securities with the SEC. And you can see we saw a little bit of history in the prior presentation on how this could develop. Obviously, it’s going to be a benefit to the businesses in order to To generate capital typically to be able to offer the stock to the general public in interstate offerings. But in order to do so then you would think you’d want to have some transparency that will be involved in it so that both sides of the negotiation will be involved. That’s where the SEC came into play here. So we talked a bit about the SEC and its role in a prior presentation we’ll get more into the process of the registration here. General financial statement required for this process will typically include two years of balance sheets three years of statements of income, three years of statements of cash flows, three year of statement of stockholders equity, prior years statements are generally presented on a comparative basis with the current years it will typically have a comparative basis. For the for the comparative years prior and current year.

Posts with the form tag

Forms of Business Combinations

This presentation we’re going to talk about forms of business combinations, which is basically external expansion, two types of entities that are going to be related in some way, shape or form, get ready to act because it’s time to account with advanced financial accounting, forms of business combinations. Now remember, we’re talking about expansion. Here, we’re thinking about expansion. We’ve got the two categories, we’ve got the internal expansion and external expansion. We’re considering here, the external expansion, we have an organization that now wants to expand and they’re going to be consolidated in some way or have two separate entities that will be combining. So now we’re talking about two separate legal entities typically separate legal entities that are now going to be combined in some way shape or forms. The forms of business combinations can be the statutory merger, the statutory consolidation, and the stock acquisition. So if you think about, in other words to separate legal entities and say, Alright, well how can these two separate legal entities be combined in some type of way, you can imagine some different Kind of scenarios in which that could take place. So and when you’re imagining those different types of scenarios, you’re going to be thinking about, okay, well, what’s going to be the key factor here, it’s going to be the controlling interest. So what’s going to be a situation where you had two separate legal entities, and now they’re they’re going to be have some controlling relationship, which could be that they’re combined together under one entity at some point or they are having a parent subsidiary type of relationship, in which case the control would be over the 50%. So that control concept is what you want to keep in mind here.