QuickBooks Online 2021. Make loan payments using an amortization table. Let’s get into it with Intuit QuickBooks Online 2021. Here we are in our great guitars a practice file, we’re now going to make loan payments with the help and use of our amortization table, which we set up in a prior presentation. To do so let’s open up some of our reports, we’re going to duplicate the tabs up top, right click on the tab up top, duplicate it, we’re going to right click on the tab up top again, duplicate again opening up then our balance sheet and P and L Profit and Loss report going on down then to the reports on the left hand side, opening up the balance sheet report.

Posts with the interest expense tag

Intercompany Transactions

Advanced financial accounting. In this presentation we’re going to discuss intercompany transactions. So typically we have a situation where where we have a parent subsidiary relationship or thinking about a consolidation type of process within it. And then we have those intercompany transactions between the companies that need to be consolidated between parent and subsidiary, get ready to account with advanced financial accounting intercompany transactions, the intercompany transactions we’ll be focusing in on here and working some practice problems in on will include the intercompany receivables and payables need to be eliminated for consolidated financial statements.

Premium Amortization & Interest

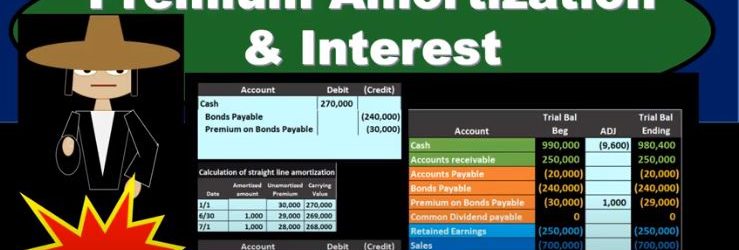

In this presentation, we will discuss the amortization of a bond premium and the recording of interest expense on bonds. This is going to be our starting point. This is the initial transaction in order to get the bonds on the books. Here’s our data down here we’ve got the number of years we’ve got the face amount of the bonds, we’ve got the issue price 270, we see that the interest on the market rate is different than the contract rate. The result then is that cash is going to be increased by the 217. The bonds payable went on the books for the face amount of the bond, the amount that’s on the bonds of the 240, which is a liability. And then we have the premium being the difference increasing the premium here by the 30. The 240 plus 230 is going to be equal to the 270,000 carrying amount book value of the bonds. Now we’re going to go through the process of recording the interest we can see that this is going to have 15 years bonds, we’re going to pay the bonds semi annually. So we’re going to have to record the interest on them. And we’re gonna have to reduce this premium in some way as well. Remember, at the end of the bonds, we’re not going to pay back the 270. We’re only going to pay back 240. So how are we going to get rid of that the premium on the bond and why are we going to do it in the way we will. We’ll start off by amortize in the premium using a straight line the method. Note that the effective method is the preferred method for amortize in a premium for generally accepted accounting principles, but the straight line method will be appropriate in some cases, if the difference is going to be a non material. And the straight line method is a simplified method and it’s easy for us to see what is going on. So we’ll start off with the straight line method.

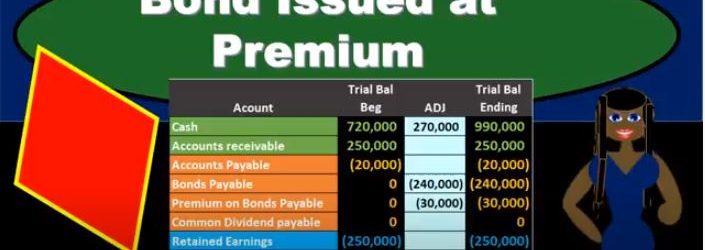

Bond Issued at Premium

In this presentation, we will take a look at the journal entries related to issuing a bond at a premium. When considering the journal entry for a bond, remember what can change and what is the same for a bond. When we think about a bond, it’s already been printed, we know the amount of the bond, the interest on the bond, the maturity date of the bond, these are already set. So if we’re making a negotiation with the bond after it had already been printed, then we can’t change the face amount. We can’t change the interest due dates. What can we change in order to negotiate and make a sales price on the bond, we can change the amount that we issue it for. So keep that in mind. Whenever you think about these bond problems. That’s the thing that’s going to differ from a bond to a note. The thing that changes when we want to loan is the interest rate. The thing that changes when we want to issue a bond that’s already been made is going to be the amount we receive For the bond being different than the face amount of the bond if there’s a difference in the market rate and the contract rate. So in this example, we’re saying that we issued a bond. Now note that when we think about the issuance of the bond, just like a note, we often have more information than we really need. And that can be a little bit confusing for us.

Make Loan Payments 8.05

In this presentation, we will make loan payments with the help and the use of an amortization schedule. Let’s get into it with Intuit QuickBooks Online. Here we are in our get great guitars file, we’re going to start off by opening up our reports down below, we’re going to be opening up three reports. This time, we’re going to be opening up the balance sheet report, our favorite report the balance sheet reports, we’re going to scroll back up top, change the dates from 1120 to 1231 to zero, then we’re going to go ahead and run that report. Then I’m going to go back up top and duplicate the tabs. I’m going to right click on the tab, I’m going to duplicate that tab. Going back to the left and we’re going to do this again. We’re going to go back down to the reports down below. We’re going to be opening up the profit and loss our second favorite report the profit and loss, the p&l the income statement, we’re going to be changing the dates up top again.