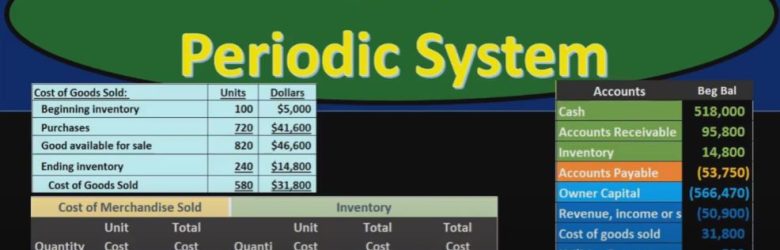

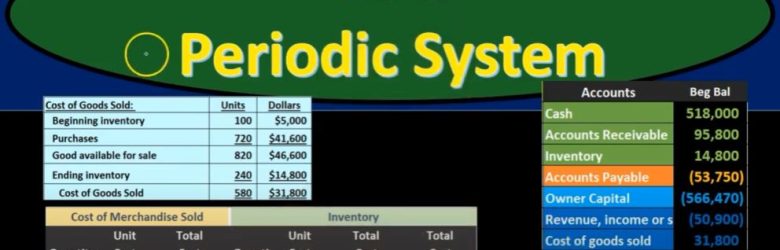

In this presentation, we will delve into the intricacies of the Last-In, First-Out (LIFO) inventory system, focusing on the periodic inventory method rather than the perpetual one. Throughout our discussion, we will draw comparisons between LIFO and other systems, such as First-In, First-Out (FIFO) and the average cost method. Additionally, we will explore the differences between the periodic and perpetual inventory systems. To illustrate these concepts, we will use a comprehensive worksheet, which will prove invaluable for addressing various inventory flow assumption problems.

Posts in the Bob Steele CPA category:

600 CPA Exam Part 1 – Inventory Methods FIFO, LIFO, Average – CPA exam & other accounting test prep

In this blog post, we will delve into the world of accounting, specifically inventory accounting. We will work through several practice problems to understand how to calculate the per unit value of ending inventory, using both the weighted average perpetual inventory system and the FIFO (First-In-First-Out) perpetual inventory method. We’ll also explore how to adjust inventory figures when errors occur. So, let’s dive right in!

Typing Mathematical Equations in Microsoft Excel 1410 Statistics & Excel

Welcome to the world of statistics and Excel! In this blog post, we’ll guide you through typing mathematical equations in Microsoft Excel, a handy tool for performing statistical calculations and data analysis. If you’re new to Excel, don’t worry—we’ll start from scratch and build our way up.

First In First Out (FIFO) Periodic System 42

In this presentation, we will delve into the concept of First In, First Out (FIFO) inventory valuation, comparing it within the context of both periodic and perpetual inventory systems. FIFO is one of the most widely used methods for valuing inventory, and understanding how it operates under different systems can be crucial for effective inventory management.

Weighted Average Periodic System 46

In this presentation, we will delve into the weighted average inventory method using a periodic system. We’ll also explore the weighted average method in contrast to the first-in, first-out (FIFO) or last-in, first-out (LIFO) methods, as well as the differences between periodic and perpetual inventory systems. To better grasp these concepts, we’ll work through an illustrative worksheet.

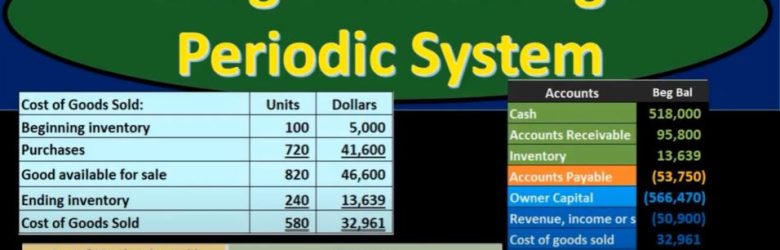

Last In First Out LIFO Inventory Method Explained 60 600

Hello, and welcome to this lecture on the Last In First Out (LIFO) inventory method. In this discussion, we’ll explore how LIFO impacts inventory accounting, using the example of selling coffee mugs. Instead of individually tracking each coffee mug, we’ll employ the cost flow method, specifically LIFO, to manage our inventory. To facilitate this process, we recommend setting up a worksheet with three essential components: purchases, merchandise cost, and ending inventory. This approach allows us to calculate units sold, unit costs, and total costs, addressing various questions that may arise.

Mean and Outliers 1416 Statistics & Excel

In this blog post, we’re diving into statistics and Excel, focusing on mean and outliers. Before we begin, take a deep breath, hold it for 10 seconds, and let’s get ready to explore the world of statistics in a smooth and soothing manner.

Combining Two Histograms on One Chart Part 3 1353 Statistics & Excel

Welcome back to part three of our series on combining histograms in Excel. In the previous two parts, we walked through creating histograms and bar charts for two different data sets related to heights. Now, in this part, we’ll learn how to combine these histograms onto a single chart and explore some formatting options to make them visually appealing.

600 Inventory Methods Explained and compared FIFO LIFO Ave

In the world of accounting and inventory management, determining the cost of goods sold and valuing inventory is crucial for accurate financial reporting. There are various methods available to estimate inventory costs, including First In First Out (FIFO), Last In First Out (LIFO), and the Average Cost method. In this blog post, we will delve into these methods and explore how they impact financial statements, particularly in the context of rising prices.

Specific Identification vs. Estimating Methods

Before we dive into the specifics of FIFO, LIFO, and Average Cost methods, it’s essential to understand why we might use estimating methods instead of specific identification. Specific identification is ideal when dealing with distinct, high-value items, like forklifts, where each item has a unique identifier. However, for more homogeneous items with lower values, such as coffee mugs, it becomes impractical to track each item’s cost individually. This is where estimating methods come into play.

FIFO: First In, First Out

First In, First Out, or FIFO, is a widely used method and often the most intuitive. It assumes that the first items purchased are the first ones sold. This method aligns with the common practice of trying to sell older inventory before newer stock, even for non-perishable items like coffee mugs.

Let’s illustrate this with an example:

In January, you buy 8 coffee mugs at $1 each. In April, you buy 5 more coffee mugs at $1.20 each. In July, you purchase additional coffee mugs at $1.50 each.

Now, a customer wants to buy a coffee mug, and you sell it for $5. The FIFO method assumes that the cost of this coffee mug is $1, which is the cost of the oldest inventory in this scenario. Consequently, your cost of goods sold is $1, and your inventory decreases by $1.

After this sale, your ending inventory would be $22.

LIFO: Last In, First Out

While FIFO is the most intuitive, Last In, First Out, or LIFO, assumes that the last items purchased are the first ones sold. This method might seem counterintuitive, as one would typically want to sell older items first, but it can have tax advantages by lowering net income during times of rising prices.

In the same example, if we use LIFO for the sale of the coffee mug, the cost of goods sold is now $1.50, which is the cost of the most recent purchase. This higher cost results in lower net income.

After the sale, your ending inventory would be $21.50.

Average Cost

The Average Cost method takes a middle-ground approach, assuming that the cost of goods sold is the average cost of all inventory items. To calculate the average cost, you divide the total cost of your inventory by the total number of units.

In our example, with an average cost of $1.21, the cost of goods sold for the coffee mug would be $1.21, and your ending inventory would be $21.79.

Comparing the Impact

Now, let’s compare the impact of these methods on your financial statements:

- Net Income: In a period of rising prices, like in our example, FIFO will typically result in the highest net income, while LIFO will yield the lowest. Average cost falls in between.

- Ending Inventory: FIFO will show the highest ending inventory value, LIFO the lowest, and Average Cost again falls in the middle.

In summary, the choice of inventory costing method can significantly impact financial statements and net income, particularly when prices are rising. FIFO tends to make a company look more profitable, while LIFO can provide tax advantages. The Average Cost method offers a compromise between the two. It’s crucial for businesses to understand these methods and choose the one that best aligns with their financial goals and reporting requirements.

In future posts, we’ll explore these inventory methods in more detail and discuss their implications in various business scenarios. Stay tuned for a deeper dive into the world of inventory management!

Statistical Inference – Questions of How Close & How Confident 1306 Statistics & Excel

Statistical inference is a powerful process that helps us draw meaningful conclusions about a population using data from a sample. In essence, it allows us to bridge the gap between the information we have and the broader population we want to understand. To grasp the concept of statistical inference, it’s essential to differentiate between two major categories of statistics.