QuickBooks Online 2021, accounts payable, beginning balances and new vendors. Let’s get into it with Intuit QuickBooks Online 2021. Here we are in our get great guitars practice file, we’re going to be continuing on entering our beginning balances as well as entering vendors so that we can use them for our data input into the future. So two things that we are looking into here, one, we want to enter our beginning balances, we’re imagining these beginning balances coming from our prior accounting system, we want to start at this point, so that we can then do the data input from that point into the future.

Posts with the period tag

Check Entry Correction 7.13

QuickBooks Online 2021 check entry correction. Now, let’s get into it with Intuit QuickBooks Online 2021. Here we are in our get great guitars practice problem, we’re going to start out by opening up a trial balance. To do that, we’re going to duplicate a tab up top right clicking the tab up top, and we’re going to go ahead and duplicate that tab, we’re then going down to the reports on the left hand side in the reports, and then we’re going to be typing in to locate the good old trial balance, which is going with a TB the trial balance this time.

Report Formatting Basics 2.15

QuickBooks Online 2021. Now, report formatting basics. Let’s get into it with Intuit QuickBooks Online 2021. Here we are in our free QuickBooks Online test drive file, which you can find by searching in your favorite browser. For QuickBooks Online test drive, we’re in Craig’s design and landscaping services practice file, we’re going to practice formatting of reports and customization of reports from the basic or standard reports, we will do so with the balance sheet report.

Comparative Profit & Loss, P&L, Income Statement 3.20

QuickBooks Online 2021 comparative profit and loss, p&l or income statement, let’s get into it with Intuit QuickBooks Online 2021. Here we are in our free QuickBooks Online test drive file, which you can find by searching in your favorite browser for QuickBooks Online test drive. When Craig’s design and landscaping services, we’re going to go down to the reports on the left hand side and take a look at a comparative profit and loss. We’re going to construct one from a standard Profit and Loss report.

Void Check Prior Period Adjustment 1.29

QuickBooks Online 2021 void check prior period adjustment. Let’s get into it with Intuit QuickBooks Online 2021. Get into it. Here we are in our Google search page, we’re searching for QuickBooks Online at test drive. And then we’re going to be selected QuickBooks Online test drive for Intuit, the owner of QuickBooks, we’re going to verify that we are not a robot, and then we’ll continue.

Report Formatting Basics 2.15

QuickBooks Online 2021. Now, report formatting basics. Let’s get into it with Intuit QuickBooks Online 2021. Here we are in our free QuickBooks Online test drive file, which you can find by searching in your favorite browser. For QuickBooks Online test drive, we’re in Craig’s design and landscaping services practice file, we’re going to practice formatting of reports and customization of reports from the basic or standard reports, we will do so with the balance sheet report. But many of these things can be done to many other types of reports as well.

Comparative Balance Sheet Creation 2.35

QuickBooks Online 2021 comparative balance sheet creation, let’s get into it with Intuit QuickBooks Online 2021. Here we are in our QuickBooks Online test drive practice file, which you can find by searching in your favorite browser for QuickBooks Online at test drive, we’re in Craig’s design and landscaping services practice file, we’re going to be constructing a comparative balance sheet. So we’re going to go down here to the reports. On the left hand side, we’re going to be creating the comparative balance sheet from a standard balance sheet.

Getting Software For Free .05

QuickBooks Online 2021 getting the software for free. Let’s get into it with Intuit QuickBooks Online 2021. Now, first question related to a QuickBooks Online Course is, how do I get access to QuickBooks Online so that I can practice with it. Two major scenarios there. One, you don’t have access to QuickBooks Online at all, or two, you do have access to it, but it’s through work or through your company file. And what we really want is a separate clean QuickBooks file that we can use to do data input in and practice with, without messing up the current company file that we may have access to.

Statement of Cash Flows 235

Corporate Finance PowerPoint presentation. In this presentation, we will discuss Statement of Cash Flows Get ready, it’s time to take your chance with corporate finance statement of cash flows. So remember when we’re thinking about the financial statements, we can think about them as answering two major questions to users of the financial statements. For examples, if we’re thinking about investing to the company in some type of way, and are using the financial statements to help us make a decision with regards to that, we want to know where does the company stand at this point in time, what’s basically their worth at this point in time. For that we get help from the balance sheet, which is going to give us the assets liabilities, equity, assets, minus liabilities equals equity, which is basically the book value as of a point in time.

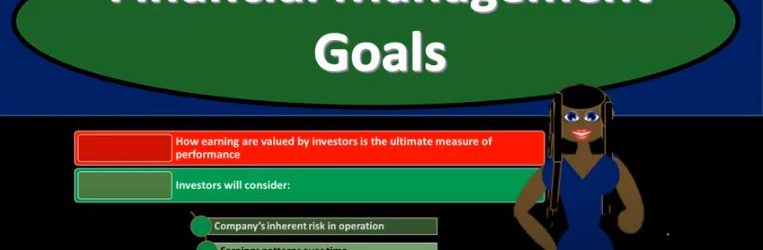

Financial Management Goals 125

Corporate Finance PowerPoint presentation. In this presentation, we will discuss financial management goals Get ready, it’s time to take your chance with corporate finance, financial management goals. Now, as we’re thinking about the financial management goals, we’re thinking about corporate finance, we’re typically thinking about a corporate structure. So management, how does management fit into the structure of a corporation, the owners of the corporation are going to be the shareholders of the corporation. So if you think about a large corporation, then you’re thinking, well, the shareholders shares are trading all the time, possibly on an exchange for a large corporation.