Corporate Finance PowerPoint presentation. In this presentation, we will discuss types of business organizations, including the corporation, partnership, and sole proprietorship Get ready, it’s time to take your chance with corporate finance types of business organizations. Now, as we go through here, note that we’re focusing in on corporate finance, and therefore on the corporate type of business organization, but many of the concepts that we will learn will be applicable to all types of business organizations. Therefore, we want to have a general idea of the different main kind of components or main types of business organizations. So those will include a sole proprietorship, partnership, and a corporation.

Posts with the Sole Proprietor tag

Closing Process Step 1 of 4 – Journal Entry 1 of 4

Hello, in this lecture, we’re going to talk about the closing process step one of the step four process. Last time, we talked about the objectives of the closing process, which in essence was to close out the temporary accounts, all the accounts from the draws, and the revenue and expenses on down to zero. Putting that balance into the capital account, we talked about how we were going to do that, we’re going to do a four step process, including closeout, the income to the income summary, and then close out the expenses to the income summary. And then we’re going to close out the entire income summary to the capital account. And finally closeout draws to the capital account. We’re going to start off with step one of those four step processes. In order to do this. We are adding this new account you’ve probably been wondering, income summary account, what is that? Where did it come from? Why is it there? The income summary can be called a clearing account, meaning it’s going to start at zero and it’s going to end at zero right when we’re done with this four step process which we’re going to do basically at the same point. Time.

Why Learn Accounting 100

In this introductory presentation, we will start where every introductory presentation should start, and that is what is in it for us. Why would we want to learn accounting? What are the reasons for learning accounting? We are going to start off to answer that question and say because it’s, we will return to this after we see the objectives. The objectives been, we will be able to at the end of this presentation, list and describe reasons for learning accounting, list and explain types of accounting list and describe types of entities. Back to our question, why would we want to learn accounting? I’m gonna say the first reason is, because it’s fun.

What Entity Type Should My Business Be?

There are many useful ways to separate and categorize business entities, one being by business form, by type of business structure, another being by a business’s relation to inventory, whether the business is selling inventory and whether they produce the inventory they are selling.

Three broad categories of business structure are a sole proprietorship, partnership, and corporation.

Sole Proprietorship Business Structure

A sole proprietorship is a business owned by one person and is the most common type of business in the United States. The benefits of a sole proprietorship are that they are easy and inexpensive to form. An individual who starts acting as a business, generating revenue, is a sole proprietor by default unless they create some other type of organizations. The income from a sole proprietor is taxable but will be reported on the individual tax return, on Form 1040 supported a supplemental Schedule C.

The disadvantages of a sole proprietor include limited personal liability protection and a limited ability to generate capital when compared to other types of organizations.

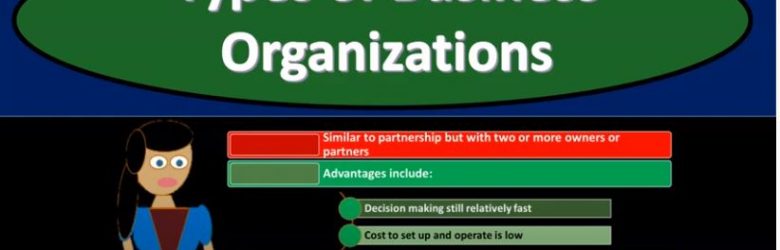

Partnership Business Structure

A partnership is similar to a sole proprietor except that the business now has two or more partners. A partnership has the same benefit of easy formation and the same drawbacks of liability exposure and limited capital generation options.

A partnership is similar to a sole proprietor except that the business now has two or more partners. A partnership has the same benefit of easy formation and the same drawbacks of liability exposure and limited capital generation options.

Corporation Business Structure

A corporation is a separate legal entity. Corporations are less common than the sole proprietorship but generate the largest percentage of total U.S. revenue.  The benefits of a corporation include that they provide liability protection through being a separate legal entity, the theory being that the assets of the corporation are at risk but personal assets are not, personal assets having more protection when compared to other types of organizations. The disadvantages of a corporation include that they are more costly to form, more complicated to maintain, and can result in double taxation.

The benefits of a corporation include that they provide liability protection through being a separate legal entity, the theory being that the assets of the corporation are at risk but personal assets are not, personal assets having more protection when compared to other types of organizations. The disadvantages of a corporation include that they are more costly to form, more complicated to maintain, and can result in double taxation.

Strategy for Learning Accounting Transactions

Much more can be said about types of entities, but this will provide a starting point. A good way to learn accounting concepts is to start out examining transactions related to a sole proprietorship and then move to a partnership and then a corporation. The reason for starting with the sole proprietorship is that it is a business form that most people can relate to and because many of the transactions found in a sole proprietorship will be the same for all entity types.

Once we understand transactions related to a sole proprietorship we can then move to a partnership, concentrating on the areas that are different from a sole proprietorship. Many of the transactions and processes will be the same, both entities needing to record the paying of the rent, employees, and utilities, both entities recording revenue. Transactions will differ, however, in the equity section because a partnership will have two or more owners, so the equity section is where to spend much of our time learning new concepts.

Once we understand a sole proprietorship and partnership we can then move to a corporation, concentrating on the areas that are different. Many transactions will remain the same, but the equity section is one area that will differ, the owners now being stockholders.

How and Why to Categorize Businesses by Inventory Use

Another useful way to categorize businesses is by industry or by whether they  use inventory and whether they produce inventory. A service company does not sell inventory, a merchandising business purchases and sells inventory, and a manufacturer produces inventory to sell.

use inventory and whether they produce inventory. A service company does not sell inventory, a merchandising business purchases and sells inventory, and a manufacturer produces inventory to sell.

A company’s relationship with inventory has a significant impact on many accounting transactions and reporting. A useful strategy for learning accounting concepts is to start out with a service company, using similar logic as we did when starting out with a sole proprietorship. Service companies have many of the same transactions as companies that deal with inventory, but they do not need to track inventory. We can then move to merchandising companies, companies that buy and sell inventory, adding the items that are different, items related to inventory. We can then move to manufacturing companies, companies that produce inventory, adding things that differ, the tracking of inventory from raw materials to work in process and then to finished goods, goods ready for sale.

For more check out the book available on Amazon

http://accountinginstruction.com/

http://www.youtube.com/c/AccountingInstructionHelpHowToBobSteele