Welcome to the world of QuickBooks Online 2024, where we simplify the vendor expense cycle to make your bookkeeping journey smooth and efficient. In this blog, we’ll explore the essential steps in the Accounts Payable (AP) cycle using QuickBooks Online, focusing on vendor transactions and expense management.

Author: Bob Steele CPA - Accounting Instruction, Help & How To

Accounting Process & Forms Overview 1080 QuickBooks Online

Navigating through QuickBooks Online in 2024 is a breeze, making accounting tasks seem almost criminal in their simplicity. In this blog, we’ll take a closer look at the accounting process and forms overview using QuickBooks Online, making the entire experience easy and efficient.

Bank Feeds & Your Accounting System 1017 QuickBooks Online 2024

Welcome to the world of QuickBooks Online 2024, where we’ll explore the intricacies of bank feeds and seamlessly integrate them into your accounting system. Join us on this journey to Cloud Nine as we delve into the QuickBooks Online test drive, the primary tool for the first part of our course.

Increase Screen Size, Duplicate Tabs, & Open Multiple Browsers 1013 QuickBooks Online

Welcome to the trailhead of QuickBooks Online 2024! In this expedition, we’ll explore the enhanced features, increased screen size, and the power of duplicate tabs to conquer the accounting landscape. Grab your gear and a bag of trail mix, because we’re embarking on a journey through QuickBooks Online – the audit trail to success.

Deposits From Undeposited Funds 7160 Excel Accounting Problem 2021

Alright, let’s create a practice problem for Excel accounting based on the provided scenario. This problem will involve recording transactions related to undeposited funds and checking account.

Record Deposits from Owner and Loan 7020 Excel Accounting Problem 2021

In this Excel accounting practice problem, we are entering transactions related to a business startup. The transactions involve recording deposits from the owner and a loan obtained for business purposes. We are using an Excel worksheet with two tabs: “Example” as an answer key and “Practice” for recording transactions.

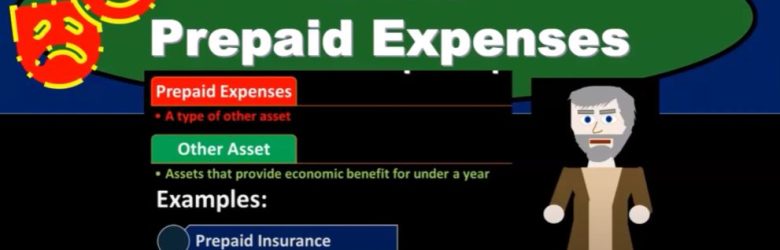

Audit Prepaid Expenses 14110

In this comprehensive presentation, we will delve into the intricacies of auditing prepaid expenses, with a primary focus on the audit process related to prepaid insurance. Prepaid expenses, categorized under other assets, pose unique challenges in the audit process due to the nature of payment preceding the receipt of benefits.

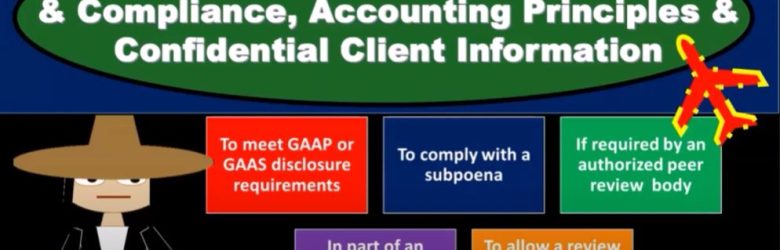

General Standards & Compliance, Accounting Principles & Confidential Client Information 9150

In the dynamic world of accounting, professionals are tasked with the critical responsibility of ensuring financial transparency, adhering to established standards, and safeguarding confidential client information. This presentation dives into the intricate web of general standards, compliance accounting principles, and the delicate handling of confidential client data.

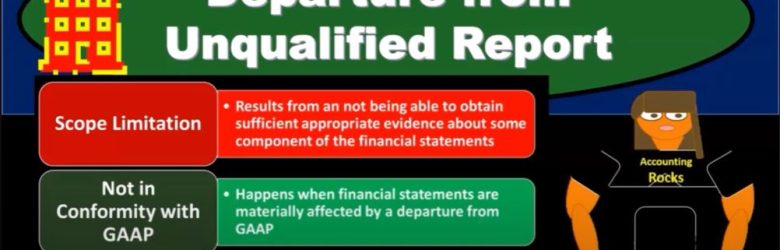

Departure from Unqualified Report 18120 Auditing

In the complex world of financial auditing, the standard unqualified report stands as the pinnacle of assurance, affirming that the financial statements are in conformity with generally accepted accounting principles (GAAP). However, auditors often encounter situations that lead to departures from this standard, raising flags and demanding a closer examination. In this presentation, we delve into the scenarios where deviations occur, the types of reports they may trigger, and the implications for both auditors and the entities being audited.