Advanced financial accounting PowerPoint presentation. In this presentation we will discuss the consolidation process and a situation where the subsidiary issues stock dividends we have stock default dividends issued by the subsidiary what will be the effect on the consolidation process get ready to account with advanced financial accounting. We’re talking about a consolidation process where the subsidiary then issued stock dividends. So we have stock dividends are issued to all common stockholders proportionally, therefore, the relative interest of the controlling and non controlling stockholders is not changed. So that relative interest isn’t changed, so we don’t have to worry about that which is nice. The carrying amount on the parents books is also not changed. So we’re not going to have to change anything on the books of the parent with basically an adjustment to the investment account using you know, typically the equity method, which is nice stockholders equity accounts for the subsidiary do change. So we do have a change to the stock There’s equity on the subsidiary, but total stockholders equity does not. So in other words, if we take stockholders equity as a whole, there’s no change there, even though there’s changes within the stockholders equity of the subsidiary. So we’re here we’re going to say this stock dividends represent a permanent capitalization of retained earnings. That’s basically what is happening, permanent capitalization of the retained earnings.

01:22

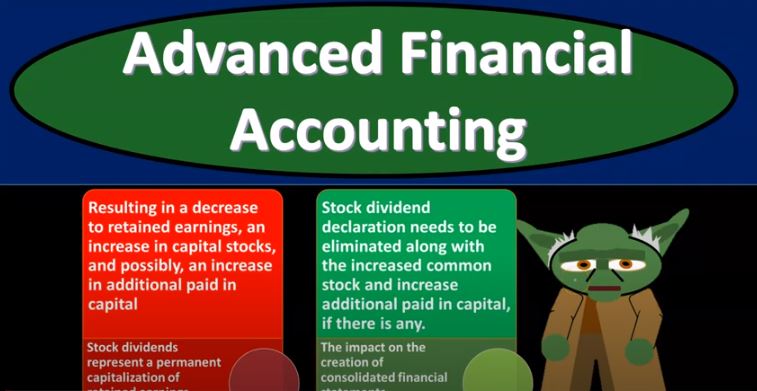

So resulting in a decrease to retained earnings and increase to the capital stock and possibly an increase to additional paid in capitals. So that’s what happens when you have to stock dividends for the subsidiary, that what’s going to happen is the retained earnings, we’re going to decrease the retained earnings because we are basically capitalizing the retained earnings and increase in the capital stock. So therefore, it goes into the capital stock, right? So what are we going to then do about it? So we’re going to say the impact on the creation of the Consolidated Financial Statements what’s going to be the impact for us within the consolidation process, the stock dividend declaration and needs to be eliminated along with increased common stock and increase additional paid in capital if there is any. So we’re going to do the elimination process. We’ve got the elimination process because we want to eliminate basically this capitalization of the retained earnings. But it shouldn’t be as difficult as you might imagine, because we don’t have the adjustments or differences or change to the relative you know, stock ownership typically with the stock dividend