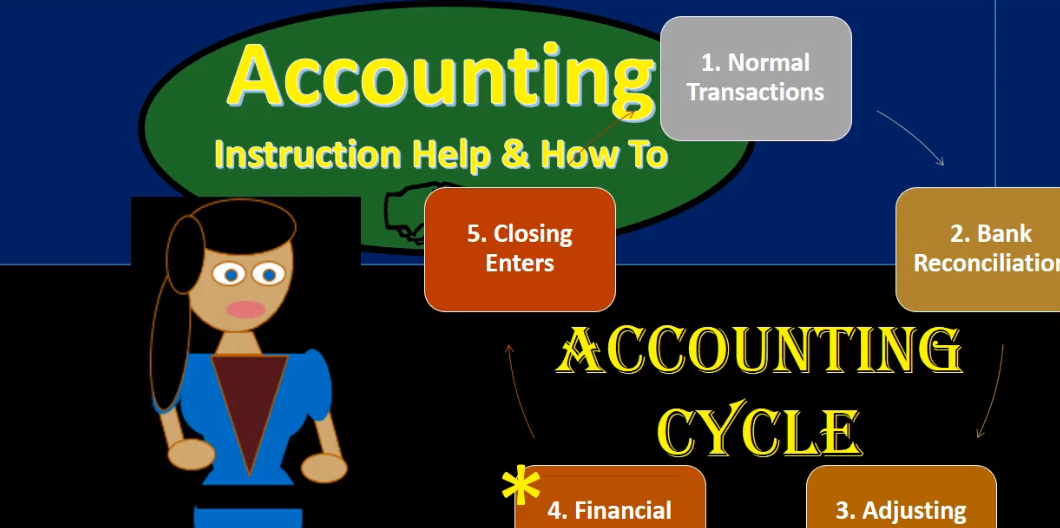

Hello, in this presentation, we’re going to be talking about the accounting cycle or the accounting process, that process that the accounting department will go through on a systematic basis over and over and over again, typically thought of as a monthly process. Although it could be thought of as a yearly process or some other process in terms of the amount of time that will pass. But these are going to be the steps that we’ll be going through in terms of the accounting process, always keeping in mind that in goal of financial accounting, which are the financial statements, some texts will have more steps than five as we have here. Some texts will have less than five steps. But the goal here is to really have a broad picture big picture, so that when we think about the accounting process, we can break down that that big picture view, five is a pretty good number for us to be able to memorize and keep in our mind if we have more than that, it can start to kind of muddy the picture.

00:58

So once we get into each of these individual steps, we want to get into more detail, obviously. But when considering the overall picture, five is a good amount of steps. And it’s enough for us to understand those different steps and understand the big picture view of what is going on as we go through the month. First step, we’re going to consider are there going to be the normal transactions, those are the things that the accounting department is doing, entering the invoices, entering the bills, and dealing with payroll, all the stuff that we generally think of in terms of the accounting department, we’re going to group into step one. So in terms of timing, step one is far greater than any of the other steps because that’s what’s happening throughout the entire month. Everything else is basically happening pretty much at the end of the month.

01:43

For example, at the end of the month, we’re going to then reconcile the bank accounts, I’m going to include the bank accounts as a step in and of itself, because it’s really a huge internal control, second only to the double entry accounting system itself. And it’s really defining that point in time. In which we’re moving from the normal business transactions to the next step, which will be the adjusting journal entries. The adjusting journal entries will then be used to create the the adjusted trial balance, which will be on an accrual basis or as close to one as possible. And all of this happens again as of the end of the time period, as opposed to what happens for most of the time period, which are those normal transactions. Once the adjusting entries have been done, we can finally make the financial statements. This is the end goal.

02:34

We have the Asterix here because this is the end product that we’re really looking for this what the external users of the financial statements and most of the reports for managerial accounting, are wanting those financial statements. But notice it’s step four of five. It’s not the end, although that’s the main event. We still have the cleanup process, the closing process, and that’s going to be our final process. We’ll have to close things out to get it Ready for this whole system to start again, at which time it will start again. So let’s go through those steps in a bit more detail. We’re starting off once again, with the record normal business transactions. That’s our step one, really what is going on, and that entails mainly everything that we’re doing throughout the entire month, which is the payroll department, the accounts receivable, the accounts payable, entering all the transactions, bills, invoices, everything is going to be all included in this step one.

03:27

So in terms of timing, this step is way bigger than the rest of the steps, the rest of the steps are really going to be the things that we’re gonna have to do to refine this information down to make those financial statements and then be ready for the next time period. So these are going to be the steps where we have the normal journal entries, we’re compiling the data from the financial transactions that are happening. We’re recording all of those transactions to the general ledger. The general ledger is being used to make the trial balance. Those are gonna we might have a an automated In doing this, we might not be entering journal entries. But the journal entries are being entered in some way when we make an invoice, a journal entry happens when we make a bill journal entries happen when we you know, write a check, a journal entry is happening.

04:13

This is what’s going on, we’re recording the data throughout the month, at the end of the month, then that’s when we got to decide, okay, the month is now going to close. We have to think about that cutoff. We’re going to want to make the financial statements. That’s the end goal as of the end of the month. And so step two bank reconciliations once we have all the transactions in there, because cash is so crucial and involved in so many transactions. It’s a huge check a huge internal control for us to reconcile the bank accounts. We don’t want to go to the adjusting process until we reconcile the bank accounts. So once we’re done with the month, we’re going to say let’s reconcile the bank accounts meaning compare the bank balance of cash to our balance of cash determine exactly what the differences are made. any adjustments we need to make, and then reconcile in terms of what is outstanding?

05:05

What are the outstanding checks? What are the outstanding deposits, that gives us assurance that our transactions are in there correctly, both our cash transactions and because so many other entries are involved in cash, it’s a huge check on our on our entire financial system, then we want the accounting cycle in terms of the recording the adjusting entries. So the adjusting entries are going to be those that are made as of the end of the month, in this case 731. All of them are made as of the end of the month. Those are our timing journal entries, meaning we’re making sure that our financial statements are correct on an accrual basis. Looking at those accounts that always need adjustment, those accounts like prepaid insurance and accumulated depreciation, and we have interest payable and unearned revenue. Those accounts typically are going to need some type of adjustment. And that’s just the The system is built.

06:01

So we’re going to put those journal entries in there in order to make our financial statements correct as of the date that the financial statements are being generated, then we’re going to take this adjusted trial balance, the one that is now been adjusted in terms of those adjusting entries to make them on an accrual basis or as close to it as possible and use them to create the financial statements, the end product, this is what we’re trying to get to the balance sheet, the income statement, and the statement of owner’s equity in terms of financial accounting. This is our product that is going out to the external users. Also the product that’s mainly going to be the basis for most of the managerial accounting reports used on an internal basis as well. So this is the main event and you might think it should be the last step then it been the main event, but it’s not the last step after we have the financial statements. We are then going to do the closing process.

06:55

And this is kind of like if we have the main events being a Super Bowl or something like that. In the closing process is cleaning up all the stadium afterwards in order for us to start the process over again. That’s what we’re doing in the closing process. We’re going to take that adjusted trial balance, which we used to make the financial statements. And we’re going to close out those temporary accounts, those accounts that are kind of like the scoreboard accounts, those revenue accounts, those income statement accounts and those drawls accounts, those are going to be these items down here. And those then, are going to be zero at the end. Why? Because as of the first day of the next month, we want them to be at zero, just like we want the scoreboard and the new game to be zero so that we can start counting up again from that point forward. So those are going to be the five steps you want to keep in mind. And when you have a broad view and thinking in terms of what the accounting process is going to be.

07:51

You want to have these five steps in mind so you know what is going on from that level, meaning starting with the normal business transactions Again, in terms of time, that’s what’s going on most of the time the whole month. That’s basically what goes what goes on the end of the month. Obviously a busy time for the accounting department because we need to reconcile the bank accounts, then do the adjusting journal entries, then the financial statements, the main event, and then we do the closing process in that point, and then we can start over and do the next process. Again, in that order. At this point, just want to note that note that smaller companies may not be required to issue publicly, you know, financial statements to the public.

08:35

And therefore, they may not be as diligent in terms of their their bank reconciliations and their adjusting entries and the creation of the financial statements as they should be. And they might be depending typically, possibly yearly to get help from an outside CPA firm, at least to make the financial statements to generate the tax returns. So just realize that if you’re in a smaller company, that There could be some differences in terms of the the just exactness of the accounting process from month to month. The larger the company that will be the, the more systematic, we’re going to have the process basically down from month to month.

09:13

Although of course there will also be more detail involved when we get into the more detail of each of these steps within the process. If you would like more information about the accounting cycle and related topics, we recommend accounting instruction reference number 300, which will provide the topics in a relevant order so you can zero in on those topics you would like to get more information on and look at the references and materials needed in order to get more information on them within the text as you zero in on what you want to look into. We also are going to have links in just about every image which will give more free information about that topic, including instructional videos, more text games, and puzzles