In this presentation, we’re going to take a look at an accounts receivable reversing entry. So the story goes like this, we had an invoice that was entered into the system in March after the cutoff date, we pulled it back before the cutoff date. So that income was reported correctly as of the cutoff date, which is going to be February 29. Now we’re going to do a reverse in entry, so that everything is correct and the following period in February as of the date of the original invoice. Let’s get into it with Intuit QuickBooks Online.

00:31

Here is our get great guitars file. We’re going to start off by opening our report. So I’m going to go to the reports on the left hand side we’re going to be opening up the balance sheet First, let’s open up that favorite report that balance sheet report. We’re going to be changing the dates up top change the dates from Oh 101202 and I’m going to make this over 310 to zero and that’s going to be the date that we made the invoice as a job and then I’m going to run this report. So that’s when the original invoice date was as up We’re going to keep it there.

01:01

I’m going to right click on the tab up top, we’re going to duplicate the tab that I’m going to go back to the tab to the left, we’re going to now go down to the reports again, we’re going to be opening up now the P and L, the profit and loss, the income statement. So then I’m going to go back up top, we’ll run the day ranch here, which is going to be a 101202. Let’s make it over 310 to zero. And so again, that’s going to be at the the invoice. The original invoice was in there in March, and we pulled it back to February, which was the cutoff date. And then I’m going to duplicate this tab up top right clicking on the tab up top and duplicated.

01:39

Let’s do this one more time with the TV the trial balance the trust the trial balance, we’re going to go down to the reports again, we’re going to type into the searching field up top, the trial balance, there it is we want to pick up that trial balance. We’re going to be changing the dates then from a 101202 or 310 to zero. We’ll go ahead and Run that report, and then we’re going to duplicate it, I’m going to right click on the tab up top and duplicate that report.

02:07

Okay, let’s go back to the balance sheet. Now I’m going to open up the balance sheet or go to the balance sheet where the balance sheet is on that tab, and then I’m going to close the hamburger, I’m going to hold down Control we’re going to scroll up just a bit to that one to five, we’re at the one to five. Now the story you’ll recall is we entered the accounts receivable or the invoice which affects accounts receivable. If we go into the accounts receivable, the original invoice that had been entered into the system was in there as of March, which it shouldn’t have been because the work was already done or the invoice was sent as of sometime in February.

02:40

Therefore, we’re going to pull this back with the adjusting journal entry into February. So that’s what we did here. We pulled it back as the cutoff date with the adjusting entry in February. But now of course by the by March, we have it in there twice. So it’s correct then as of the cutoff date, because that’s when we did the work and when it should be recorded on an accrual. basis, but it’s incorrect as of March when we when the other invoice was in place. So we’ve done everything right to make the financial statements correct.

03:08

Now we got to do what we got to do in order to make the bookkeeping correct for the following months, and not mess up the accounting department. So we want it. In other words, if we keep these two things separate, you think about these two things separate. We didn’t want to change the date on the invoice. We don’t want to like delete the invoice or anything like that, that would be messing up the accounting department side of things from our side of things, the adjusting department side of things, you could think about them as two separate items.

03:34

Even if you’re doing the same process, what we want to do is be correct as of the cutoff date for the accrual purposes, that’s our job, and then reverse it so that we don’t cause any frustration to the normal bookkeeping flow so they can do whatever is logistically easiest to do in their side of things. So what we’re going to do then is reverse this journal entry but we’re going to do so after the first day of the next month, as all of our reversing interest will be done as of the first day of the following month of the cutoff period.

04:05

So that’s going to be the same for all other accounts on the invoice. And this is our the accounts affected. So we kind of had to look at a journal entry to think about this because there’s a lot of accounts affected here, even though we still use the registers to enter the adjusting entry. So this was it, we had accounts receivable go up, we had the sales tax payable go up, and that’s where the credit we had the sales or the revenue go up. And that’s where the credit Cost of Goods Sold went up with a debit and then the inventory went down with a credit.

04:32

Now when you think about the reversing entry here, it’s easiest to think about exactly what happens first and then just reverse it exactly. And I wouldn’t even change the account ordering. Notice that I have the debit on top, obviously in the credits on the bottom here. But you know, you could make this all one journal entry and then the two debits on top would be accounts receivable and cost of goods sold, which is what the way they used to teach it which is kind of crazy but kind of silly because most people see it this way, even though it can be written in a different way.

05:03

So I’m going to do the same thing. Here, I’m just going to keep the same outline and say okay, the reversing process, then if I just copy these over, I’m not going to try to reorder the accounts, I’m just going to say I’m going to do the exact opposite. I’m going to credit the accounts receivable, I’m going to debit the sales, tax payable, debit the sales, I’m going to credit cost of goods sold, and I’m going to debit inventory. So that’s going to be our reversing process. All I did was flip what we did here, I’ll hide these cells and hide and that’s what we’re going to do right.

05:40

So let we’re going to enter that into the system. Now we could try to use the registers again. So if I go back to the register I have I’m forced to use the sales tax payable register, which is that kind of clearing account but we’ll we’ll get to the invoice and no matter what we do because with there’s three accounts affected, but let’s check it out. We’re going to hold down Control, scroll back down a bit. We’re going to then go down to the accounting down below, we’re looking for the the chart of accounts. So worth the chart of accounts as is the first tab, we’re looking for that sales tax payable, which is going to be a liability, other current liability.

06:14

So we’re in the types category, here are the other current liabilities, here’s the sales tax liability. That’s the one we want. Going to go into that one. And we see that we had this 123 their increase, we now want to decrease it, I’m going to choose to do so with a journal entry. So I’m gonna say I want a journal entry. And I want to make it as of the reversing entry date, which is the first day following the cutoff date. cutoff date was at the end of February to 29. Because there’s 29 days and 2020 apparently, and this then is going to be as of Oh 30120301 to zero memo, we can say it’s a reversing entry so that the accounting department that they know that’s what the Crazy adjusting department people did and I have not my business, you know if that’s because they’re separate, you know, in your head, we’re taking them separate.

07:10

So we’re going to say that this is going to go down by the 123, point five. So we’re going to say it’s going to go down when the decrease 123, point five. And then the other side, I only have one account over here. So what I’m going to do is I’m going to say, where’s the other side, I need two accounts. So I’m going to say let’s try putting it to the sales and then adjusting it, which means it’s going to go to the journal entry.

07:34

So when I put it to the sales of the product, I’m going to post it. It’s not right yet, but then I’ll just open the journal and I’m going to say I don’t have a split field here. I can’t put more than one account. How can I do that? Well, I can say let’s save it like that, and then go back into it. Where we have this reversing entry. I can click on the split here now. So if I select select the split, then I have more options they give me at this point, which Would be nice if they gave them to me originally. But now I’m going to go to the editing option. And that’ll take me to the journal entry form.

08:07

So basically, we pretty much have to go to the journal entry because we have three accounts that are going to be affected here. So here I’m going to say All right, now I’m just going to put this in here the way I have it here. accounts receivable, I’ll put that on top, even though it’s going to be a credit which typically goes on the bottom. So we’re going to say it’s accounts receivable. And that was for I’ll just change this up to the credit of 142 350. So it’s going to be over here 142 3.5 it’s gonna be a reversing entry. And we’re going to put that I think it was Anderson, we have to put a customer remember when you’re dealing with accounts receivable, and then the second account is going to be that sales tax payable. So I’m going to put sales tax payable or sales tax liability.

08:55

That’s going to be that 123 point five on the debit side. As we can see in our little journal entry over here, and then we have the sales. So and I’m going to put the same memo and all three lines, I’m just going to copy that. We don’t need a customer here on the wall, maybe we do on the sales tax liability, it should be the California Department of tax would be the vendor. And then we need the sales tax liability, which is the income line. And there’s the income line. Now this should look funny because we’re kind of deep, we’re decreasing income that doesn’t typically happen. This whole entry should look a little strange because it’s, it’s backwards, and there’s the 1300 but that’s because it’s a reversing entry of course, and that’s going to be 1300.

09:42

So there we have that. Okay, so that’s gonna be the first half of this. Let’s go ahead and save and close this. So let’s go save and close. Everything looks good. I just double check it does it look okay. I think it does. I think it does. I’m going to save and close. Something’s wrong. See what’s wrong, this one to this should be one. I knew something was funny there 123 point 512 3.5. And that should balance out the old debits and credits. Okay, let’s try that see I’ll QuickBooks won’t let us post something before. It’s not in balance, which I totally demonstrated on purpose.

10:19

So now we’re going to go down here and save and close again and see if it lets us do so. So there we have it. So now we’ve have that now I’m going to post the second half, which is going to be this one cost of goods sold and inventory. I’m going to use the inventory register this time because I have to use the inventory register because the cost of goods sold is on the income statement, therefore has no register. So I’m going to go back to our chart of accounts. We’re looking for the inventory, that’s going to be an asset up top it’s going to be other current assets.

10:51

I think they break out inventory up here inventory asset, this is the one we want the inventory asset not not choosing the second one down here, but To be or the first one inventory asking, it’s not the investment but the inventory. Alright, so now I’m going to open up the view register, we’re going to make another journal entry.

11:12

So in the drop down have a few more options here we want the journal entry. journal entry is going to be as of with 30120, that’s going to be the reversing entry dates as always, we’re going to call it a reverse scene entry. And then I’ll check the spelling because some funny somewhat reversing entry, I think that one’s the one and this is going to be the inventory is going to be going up by 4010 or 1040. And then the other side is going to be going to cost of goods sold, it was going to go to cost of goods sold which is the expense account. And then we have that now we could save that. And if I want to look at it in journal entry format, we can select a split item here and see if we got everything going the right way and then edit it. And it’ll take us to that journal entry.

12:04

So the inventory, then the inventory is going to be going up and I have it I have it in there in the wrong direction. So that’s good thing we checked it here it should be going 1040 and then the cost of goods sold is going down because it’s the reversing entry 1040. And then we have the reversing entry, reversing entry. Okay, so then if I go back over, that’s what it’s cost of goods sold is credited, inventories debited cost of goods, so credited inventory debited, let’s go to go to, let’s save that. And then I’m going to close the journal. And that’ll take us back to the register, just so we can see it on the register now. So then within the register, I’m going to sort it by date, go by date here and there.

12:56

There it is. So this is going to be our Here it is the journal entries down here, reverse an entry it’s going to be an increase, it’s going up on the increased side and in the split is going to go to the other side cost of goods sold. Here’s the split items, inventory and cost of goods sold. All right, now let’s go back to our balance sheet. And we can check things out and see if this makes sense. So we’re basically looking out to see if we’re okay, as of March, we saw last time with the adjusting entry that we’re okay as as the cutoff date after the adjusting journal entry.

13:30

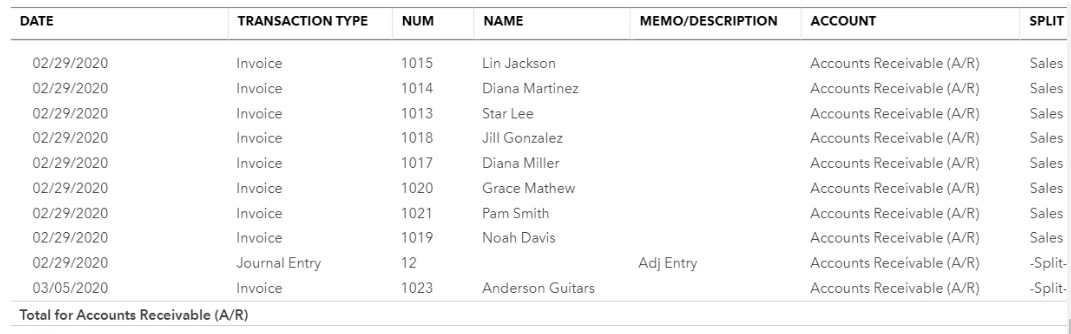

Now we want to make sure that we’re okay as of the end as of March so that the normal bookkeeping isn’t there, right and, and in essence, we don’t have things in there. twice, we don’t have a doubled up. Alright, so let’s take a look at the accounts receivable. Then scrolling down to the accounts receivable we have on the 29th. We had the adjusting entry that brought it in to the current time period, then we simply reversed it back out and that puts that that puts it back to where it should be. And that happened after the cutoff date. So this was correct as of the cutoff date, we reverse it back out after the cutoff date. And then at this point, this is when the original invoice was in there at three, five.

14:12

Therefore it’s not, you know, we have that gap between three one and three, five, right, because we’re not going to put, I’m not going to put the reversing entry as as of three, five, I’m going to put all reversing entries as of the first day of the next time period, just so everybody knows where the reversing entries are, even though there’s going to be that gap between the three, the three, one and the three, five. In other words, if it was a perfect world, you would think I would reverse it as a three, five But no, I want all reversing entries as of the first day the next time period so that I know that we’re all the reversing entries are and I can print them out easily and find them simply.

14:48

So I’m going to go back to our balance sheet. Other side is going to be on the p&l profit and loss. I’m going to close the old hamburger appt up. Then we’re going to go down to the sale of product income. I’m going to open That up, scroll down the bottom of it. And here we have our adjusting journal entries. So here’s our adjusting journal entry, bring it in there, then are and that makes it correct as of the cutoff date, then we had the reverse and entry which is going to be in there March 1, right? You’ll see that this happened in March 1 after the cutoff date in the next month. And that happened on the first and then we’ve got a few days until the fifth when the actual invoice which includes these two items that add up to that 1300 was input so so that’s we reversed it back out and put it back in place.

15:37

We’re okay then it’s not being double entered as of this as of this time period, so everything should reverse out and be okay. Going back up top. We’re going to go back to our income statement. So back to the income statement, and then we’re going to go to the balance sheet again.

15:55

The difference between those two was to the sales tax payable, sales tax. payable, which we put to the account, sales tax payable here which is kind of a contra account to the sales tax when you’re processing the sales tax which is the they put to the vendor which for our cases California, so sales tax liability, we put then the entry and they’re the adjusting journal entry here, adjusting journal entry is here, then it reversed back out, and then the sales tax for the current time period the invoice went to the not this area, but if I go back up top, the original invoice is going to be going here to the California Department and so on so forth.

16:40

That’s where the original invoice will be, which is going to include these items for Anderson. For Anderson guitars. There’s the invoice on three, five, scrolling back up top then we have the inventory going down. So if we take a look at the inventory then it should be up top somewhere right in between Lori’s up in the assets section, here’s the inventory. If I select the inventory, then scrolling back down for the inventory, we had the adjusting entry here and I kind of was thrown off because I put it in there as up to 28. And there’s 29 days in this current month.

17:18

So I’m actually going to fix this. Now, I would like the adjusting entries as of the last day of the month, which for 2020 isn’t the 28th, but the 29th. So I’m going to go in there, I’m actually going to fix this at this point, I’m going to go into that adjusting entry. Notice it wouldn’t really hurt anything if I didn’t fixed it. But I want to be able to run a report as will do at the end of the section to see the adjusting entries, and it’ll be a lot easier to do. So if all adjusting entries are in there as of the last day of the time period. That’s why we’re doing this last day of the time period.

17:47

Notice what we’re not doing I’m not really concerned the fact that we’re not on perfect accrual basis, any other time during the month. I’m concerned about it went at the month end when we need to do the financial statements to be on a perfect kind of accrual basis. The rest of the month, I’m concerned with logistics for the accounting department to do their job, you know, basically as easy as possible. And so you got to kind of balance those two things out. So any case, we got the 29th. So there it is, and then we have the reversing entry.

18:14

So here’s the reversing entry. So we’re correct as of the cutoff date, then we have the reversing entry. And then we have the actual invoice that went in place once again, in March. So as of the march 5, we’re back in in place and we haven’t we don’t have that double entry. We don’t have any problem with having entered something two times. Alright, so now let’s go to the other side of it. I’m going to go back to the balance sheet, we’re going to go to the P and L the profit and loss that of course being the cost of goods sold. Let’s go into the cost of goods sold. And we scroll back down we’ll have the similar kind of story here.

18:50

We have the adjusting entry, the adjusting entry bringing it making us correct as of the cutoff date, then we reversed it, first day of March and then we Have the original invoice that was in there in March, therefore not having that double entry once again, going back up top. I’m also want to open the inventory report at this time. So I’m going to go back to the first tab, I’m going to open up the old hamburger holding down control and scrolling down.

19:18

So QuickBooks doesn’t do anything funny scrunch anything up in any kind of weird way that I’m going to type in inventory. And we’re looking for the inventory valuation the or summary, the summary one, I’m picking up the summary one. And if I look at, as of let’s make it 1230 120, just the end of all time here, we’re down to the 672. you’ll, you’ll recall that this one was not in balance as of the cutoff date because we made a journal entry that that affected inventory but didn’t have inventory items affected and therefore the items list here the inventory items did Line up to the actual inventory on the financials.

20:04

Now that we’ve done the reverse and entry 672 should tie out to if we go to the trial balances go to the TV this time just for something different. And will I have to refresh it then have to refresh it if I want to do something different. Now it’s fresh. So if we go down, we have the inventory assets, there’s the 672. So we’re tied out there, everything matches up there. That looks good. Then let’s go back to our data. One more time, I’m going to open up the hamburger and the other report that we’re concerned about when we did when we do this process is the customer balance report.

20:41

So a customer balance detail let’s look at the detail one, the customer balance detail, because we’re dealing with accounts receivable when we when we dealt with that invoice, I’m going to close up the old hamburger. And you’ll note here that now we have the Anderson where we Had a journal entry the journal entries actually in this report, because we were forced to recall to enter the customer when we entered the adjusting journal entry as well as the reversing entry, which makes it go up and then back down. And here’s the original invoice that was on 335. If we go down to the bottom, we’re at 11 and 934.

21:20

Here, if I go to the TB trial balance, we’re at the 11 934. And just a reminder, it’s that we went back and forth before between the balance sheet and profit and loss when analyzing the accounts, you can go directly to the trial balance, because you know, it’ll have the balance sheet account and the income statement accounts on the one report. So sometimes that’s an easier one to work with easier one to see