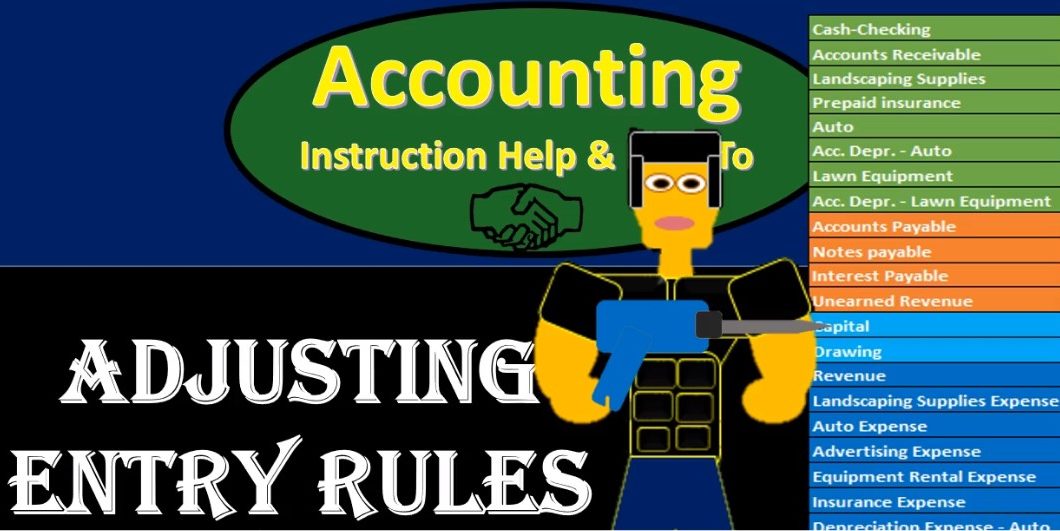

Hello in this presentation we’re going to talk about adjusting entry rules. In order to talk about adjusting entry rules. We first want to distinguish what adjusting entries are from normal journal entries. Normal journal entries being those transactions we will be recording throughout the month including the payment of the utility bill pain of wages, purchasing something on account the things that the accounting department typically does. Within the adjusting process, we’re going to draw a line or head and say the adjusting department is done in a separate department or as a separate process have a separate set of rules. Some of those rules being the same as for every journal entry, some different, the adjusting process is going to adjust accounts such as prepaid insurance, depreciation, unearned revenue, those types of accounts that need to be adjusted as of the end of the time period as a financial statement date in order to make the accounts on an accrual basis as of that date.

00:59

The rules for everything transaction including adjusting journal entries or normal journal entries will include every transaction has at least two accounts affected. So if this is our chart of accounts, we would need at least two of these accounts involved in every transaction, maybe more, but the minimum would be two. Why? Because we need an equal number of debits and credits in each journal entry. So each journal entry would need at least two accounts in order to achieve the goal of every transaction having an equal number of debits and credits. Then we have rules that are going to be specific to adjusting journal entries. These are going to be really important because we’re going to construct our thought process based on these rules, slightly different thought process in constructing the adjusting journal entries. Then we have when constructing just normal journal entries, rules for adjusting journal entries.

01:49

Again, these only apply to adjusting journal entries include dated end of the period. So if it’s the end of the year, we’re going to say 1231 or the end of the month. The date over the financial statements the balance sheet date, that point in time generally will be the date of the financial statements. We have no cash involved when we are making journal entries for adjusting journal entries. This is important because cash is involved in just about every or many transactions for the normal journal entry process and it’s one of the first accounts that is the first account we typically think of when trying to construct a normal journal entry not going to be there for the adjusting journal entries. Cash is going to be done as far as what needs to be done to cash the bank account will generally be reconciled before the adjusting process, no change to cash within then the adjusting process, we’re going to have one balance sheet account and one income statement account.

02:43

So in our trial balance the balance sheet accounts it’s going to include the capital but typically everything above the capital account. We’re going to pick one of those accounts related to the transaction the adjusting entry we are working on, and we’re going to have one income statement account the accounts below The capital account of the drawings, your revenue or expense accounts, there are typically going to be one of each Why? Because those are the timing accounts down here. And when we do the adjusting entries, we’re dealing with timing. We’ll talk more about the reasons for these rules in a future presentation however, so the rules recapped here are going to be rules for all transactions, including adjusting journal entries, every transaction has has at least two accounts affected, every transaction will have an equal number of debits and credits rules for the adjusting entries, only that we want to keep separate in our minds. For the adjusting entry process dated at the end of the period, no cash involved one balance sheet account and one income statement account.

03:45

We’re going to use these rules to construct a new thought process one that will be used for the adjusting entries will really help us to create the adjusting entries even if we don’t know exactly what the journal entry is doing. So we can actually put it together and it’ll help us to start through that process. So even if we don’t know exactly why we are doing what we are doing, then of course we’ll think about more why we are doing what we’re doing when we construct the adjusting journal entries.