In this presentation, we will enter a transaction related to the receipt of a government grant into our not for profit organization. Get ready, because here we go with aplos. Here we are in our not for profit organization dashboard, we’re going to head on over to our Excel file to see what our objective will be, we’re going to be in tab four. So we’re in tab four, where we have a contribution that’s going to be for the school over to our description up top. So this is going to be the government grant to be used for education. So we’re going to get money, we got money from a government grant. And we have to use it for a specific reason, they put a restriction on it in other way.

Author: Bob Steele CPA - Accounting Instruction, Help & How To

Pledge 135

This presentation, we’re going to enter a transaction related to a pledge and our accounting system. Get ready, because here we go with aplos. Here we are in our not for profit organization dashboard, let’s jump on over to Excel to see what our objective will be. We are in Excel, we’re in tab number three, we’re now recording a pledge. Now the pledge is going to be similar to the contribution. However, we haven’t got the money yet. So it’s a promise to pay. If you compare this to a for profit type of organization, the contribution would be similar to us doing the goods or services at the same point in time that we get paid. And you can imagine given a sales receipt, like at the register, at that point, and then the pledge is going to be similar to us doing a service or providing goods before we get paid.

Cash Donation 130

In this presentation, we’re going to record a cash donation or contribution into our not for profit organization. Get ready because here we go with aplos. Here we are in our not for profit organization dashboard, we’re going to be jumping on over to Excel first to see what our objective will be. So here we are in Excel, we’re on tab two in our Excel worksheet, we’re going to be recording a cash donation. Now note, we’re going to be recording this as a one lump sum donation. But you can imagine we have multiple donations, that would be of a similar format.

Office Space Donated 125

This presentation, we’re going to record a transaction related to the contribution or donation of office days to our not for profit organization. Get ready because here we go with aplos. Here we are in our not for profit organization dashboard, we’re going to jump on over to Excel to see what our objective will be, we’re going to be on tab one. So I’m on tap one here, and number one says it’s going to be office space donated. So it’s going to be a bit of a tricky transaction for the first transaction here we got a contribution, but that contribution isn’t cash and which would be the normal type of contribution what was contributed instead, the use of the facilities the use of office space.

Fund Raising Purposes 121

In this presentation, we’re going to set up and analyze the function of purposes within our accounting software, the purposes are going to be similar or serve a similar function as the items like inventory items and service items in a for profit organization. Get ready, because here we go with aplos. Here we are on our not for profit organization dashboard. Last time, we were over here in the accounting section, and we set up our chart of accounts and we set up our tags. Now we’re going to be going into the donations section we’re going to go into the donations, this is going to be our revenue type of site of section if you’re thinking about this as a comparison to a for profit type of organization, is how we’re going to be generating revenue with those donations.

Set up Funds & Tags 120

In this presentation, we’re gonna set up and customize our funds and tax features within our accounting software. Get ready, because here we go with aplos. Here we are in our not for profit organization dashboard, we’re gonna go into our chart of accounts over here. Now, we’re going to go into the fund accounting tabs and the fund accounting tab up top, then you’ll see another bar here with our drop downs, we want to go to the accounting drop down on the far left hand side, we’re going to first go to that first item, which is going to be the accounting tab, we’re going to be going into the accounting tab. And then right up top, we have our funds features.

Aplos – Set Up Free Trial 105

In this presentation, we’re going to take a look at the setup process for the free trial of aplos. aplos is an accounting software that’s designed specifically for not for profit organizations they typically have and at this time do have a free trial component for it, which is a great tool to get used to the software and go through a practice problem as we will do here. Get ready, because here we go with aplos.

Patterns of Financing 610

Corporate Finance PowerPoint presentation. In this presentation, we will discuss patterns of financing, get ready, it’s time to take your chance with corporate finance patterns of financing. As we think of financing patterns, let’s first think of our accounting equation assets equal liabilities plus equity assets are what the company has, we have those assets in order to help us to generate the revenue, we need to finance those assets, either with liabilities or equity, equity being the retaining of earnings over time, the earnings that have not been paid out in dividend and or investments that have been put into the company for the distribution of stocks.

The Nature of Asset Growth 605

Corporate Finance PowerPoint presentation. In this presentation, we will discuss the nature of asset growth, get ready, it’s time to take your chance with corporate finance, the nature of asset growth, we’re going to start off with working capital management, what is working capital management, the financing and management of current assets of the company. So when we consider this, let’s think about the accounting equation assets equal liabilities plus equity, remember that the assets are what the company has, why does the company have them in order to help generate revenue to get a return on the assets in order to help generate revenue?

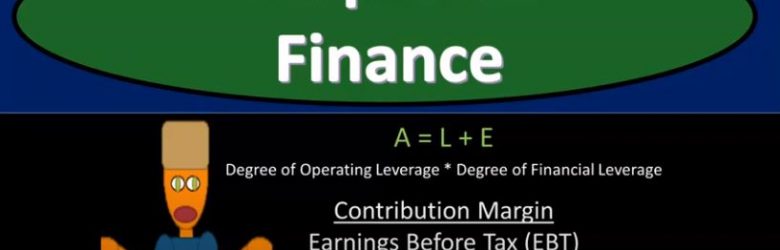

Combined Leverage 525

Corporate Finance PowerPoint presentation. In this presentation, we will discuss combined leverage, get ready, it’s time to take your chance with corporate finance, combined leverage. Remember when we’re thinking about the term leverage, there’s typically two types of leverage that come into our minds. One is going to be the financial leverage the others the operating leverage the financial leverage, probably the one that pops into most people’s mind, if they’re familiar with leverage that being related to the debt in the organization and the risk and reward related to different levels of debt depending on the circumstances. And then we have the operating leverage, which has to do with the mix between the variable costs and the costs and the in the fixed costs.