In this presentation, we will calculate the bond price using present value tables. Remember that the bonds is going to be a great tool for understanding the time value of money. Because of those two cash flow streams we have when with relation to bonds, meaning we’re going to pay the bond back the face amount of the bond, and we’re going to have the income stream. And those are going to be perfect for us to think about time value of money, how to calculate time value of money, our goal being to get a present value of those two streams. So we’re going to think of those two streams separately generally, and present value each of them to find out what the present value of the bond will be. We can do that at least three or four different ways. We can do that with a formula actually doing the math on it. We can do it now, which is probably more popular. Now. Do it with a calculator or with tables in Excel, I would prefer Excel or we can use just tables pre formatted tables. The goal here the point is to really understand what we’re doing in terms of what what is happening, what can it tell it? What can it tell us, and then understand that these different methods are all doing the same thing.

01:10

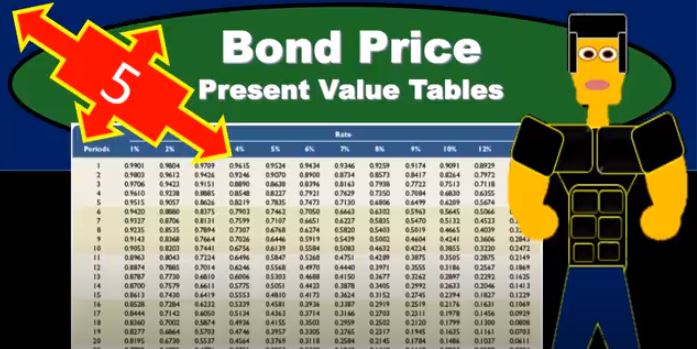

So that whatever you’re being taught or whatever you have to work with, whether it just be paper and pencil on a test, or in practice, where you have a calculator, it’s all the same type of calculation is coming from the same place. It’s coming from the math, of course, but us here are we’re How can we apply that? Now, accounting textbooks often use tables, so we’re often going to use a table looks something like this. And the confusing thing about tables is one, they’re just a lot of numbers. So that’s confusing, but once we understand them, that’s not that bad. The other thing that’s a little confusing, it’s just to know which table we need to work with. Remember, there’s two different types of streams that we have here. And one is going to be doing with the present value of one typically called the present value of one or equivalent to this formula. So the table is going to have the time periods Gonna have the rates, that’s going to look the same on any of these kind of present value or future value tables, what’s going to different, we got to make sure that we look at the name of the table and are picking up the correct one for what we’re doing. So if anything says future value, that’s not the one we want. Right now, we’re not trying to calculate what the future value is, what we’re trying to do is calculate what the present value is. So you can eliminate those two tables and you’re left with a present value of one or present value of an annuity.

02:29

When you’re considering the present value of just one payment, such as the bond payment that we’re going to pay back the hundred thousand at the end of four time periods or two years, we know that the present value is going to be less than the face amount of the bond if we’re going to pay 100,002 years from now. In other words, the current value today is going to be less than 100,000. So if you just look at this table, you could say, well, this makes sense because I’d have to multiply that times something less than one in order for the payment to be something Less than the amount that we’re paying out, because time value of money would state that the amount today is worth less than the amount we actually pay out two years from now or four time periods from now. So this then is the table we’ll use when we do the face amount of the bond calculation. The other component of the bonds that we’ll have to deal with in terms of present value is the interest component, we’re going to pay interest and we’re going to pay interest every six months, in this case, 4000. So we’re going to pay 4000 each six months for four times.

03:33

And that’s going to be an even we call that an annuity. So we’re going to have the present value of an annuity type table, it looks really the same, because we’re going to have the same periods we’re going to have the same interest amounts that we’ll be using to figure out what the rate what this amount will be, we’ll be using for a calculation. However, if you look at the table, of course, you’ve got all these numbers that are greater than one now. And if you think about it, that of course makes sense because if we’re talking about an annuity we’re trying to present value an annuity, that what we’re doing is we’re saying, well, there’s 4000, that’s going to be paid four times, in this case, every six months for four time periods. So if we multiply that times four in dollars, we’re actually going to pay 16,000. So it’s going to be something less than 16,000. But it’s going to be something greater than 4000. So what we’re going to do here is we’re going to take the 4000 have to multiply it times something. And we would expect the result to be something less than 16,000, more than 4000 less than 16,000. And so that would make sense that these numbers, of course, are greater than one in order to get a calculation.

04:41

That would make sense. So if we do this, then we’re going to say okay, well, how can we figure this out? First, we’re going to take a look at the face amount calculation, it’s the same calculation we did with the formulas, we have to think about the face amount calculation, we’re going to pay at the end of the time period and then the interest. So if we take a look at The face amount calculation, we’re going to pick up the amount from the table for the present value of one, the amounts that are less than one. And we’re picking up 5% and four periods. Why? It’s two year bond, and we’re going to pay it semi annual. So just remember to make sure that you don’t pick up once a year, we’re paying every six months. So if it’s two years, and we pay twice a year, then we’d have four time periods. Where does the 5% come from? Well, the market rate and we will be using the market rate here to present value things because we’re present valuing using the market rate is 10%. And that would be four per year, but we’re paying every six months. So we’re going to say there’s four time periods. And this six month rate then would be the market rate divided by two. This is often one of the most confusing components by the way. So just make sure to think through that every time we see an interest rate it means per year divided by two. So then we’re going to take the bond face amounts 100,000 We’re going to just multiply it times that rate. So they’ve done the math for us here and broke it down into just this percentage.

06:07

And so all we have to do is take that times the percentage, we get the 80 to 270, that wouldn’t match the math if we did the math to do the same thing. So all that means is, of course, that we’ve got 100,000 that we expect to pay for two years from now or four time periods for six month time periods. Then if that was the only thing happening, and we weren’t paying any interest, today, we would expect to get 82,002 70. In other words, if I was just going to pay 100,000 at the end for money today, then you would think the market would say I would get 80 to 270 from somebody today willing to give me 80 to 270 for me to pay back 100,000 at the end of four time periods or two years. Then we have the other component which is going to be having to do with the interest which we’re paying 4000 which is 1000 times to eight percent. So we’re going to pay interest of 100,000 times point oh eight, that would be the yearly rate stated on the bond divided by two 4000. That’s what we’re actually going to pay every six months for four periods two years. So we’re going to use our table again, but this time for an annuity, and you can tell it’s an annuity table, because they’re greater than one, the amounts are greater than one. And we’re going to pick the same area that 5% for periods for periods, two years times two, for semi annual 5%, because we’re taking the market right now.

07:36

And we’re dividing it by two so that it’s not a yearly rate, but a per six month rate. And then we’ll just take our interest per period 4000 and just multiply that times 3.5460. They did the math for us, that’s the point of a table. And if we get multiply that out, we get 14 184. In other words, if if we wanted to get money today We’re said we’re going to pay back 4000 each time period for money today, we’re going to pay back 4000 times 416, we would expect to get 14 184. Today, in order to pay back 4000 every six months based on the current market rate. So the bond has both of those components, it has the face amount, we’re going to pay back, worth 80 to 270. In today’s dollars present value and the 4000, we’re going to pay back in an annuity every for every six months $16,000. And that’s worth 14 184. Of course, if we add those two up to 82 to 7214 184, we get the 96 for 5454. So then the journal entry would just be if we issued this bond, we’re going to get 96 454 for it, and we’re going to put the bond on the books 100,000 that’s what we owe at the end of two years. The difference then is that discount 3005 46. So of course the cash is going up. We’re saying the bonds going on the books for the 100,000 and then we discounted it by that 3005 46. So the actual value of the bond is 100,000 minus the, or the carrying value, the book value minus the 3005 46.