Corporate Finance PowerPoint presentation. In this presentation, we will discuss patterns of financing, get ready, it’s time to take your chance with corporate finance patterns of financing. As we think of financing patterns, let’s first think of our accounting equation assets equal liabilities plus equity assets are what the company has, we have those assets in order to help us to generate the revenue, we need to finance those assets, either with liabilities or equity, equity being the retaining of earnings over time, the earnings that have not been paid out in dividend and or investments that have been put into the company for the distribution of stocks.

00:35

In the case of a corporation, the liabilities being the third party debt, we’re going to be focusing more on the liabilities in order to do financing our assets and think about what the optimal strategies might be to do so. So we must select optimal external sources to finance the assets, financing patterns, we’re going to be matching assets build up and financing terms lengths. So in other words, we’re going to be considering our assets, and looking at the structure of the assets that help us to think about the liabilities that we’re going to be needing in order to finance those assets. So we’re going to go back to our schedule here we saw in the prior presentation, we’re thinking about the idea the concept of us breaking up our assets, we can have the the fixed assets, which are basically going to be fixed in nature, as you would basically expect, and you would expect them then to be financed with more equity, or long term debt type of financing.

01:32

The current assets are a little bit more confusing, however, because although they’re current we’re going to be breaking them out into as we discussed last time, the temporary current assets and the permanent current assets, the permanent current assets being those items that are going to always be replaced. So in this case, we see them they’re increasing things like accounts receivable or inventory, which although they turn over all the time, they’re always replaced by other sales items. And therefore, we can think about them having some type of baseline.

02:03

Now if it’s a period of growth, as we can see here, then that permanent current asset level may increase over time in a steady rate with the growth but we can have like a linear type of relationship, whereas the temporary current assets are those such as inventory, and accounts receivables, that are going to vary along with changes in sales level, possibly for like a seasonal type of business. So they are going to fluctuate. So when we then apply our loan strategies here, it might look something like this, we might say, well, the fixed assets, the things the property, plant and equipment, they are what they are, we’re going to be financing them with equity and debt. And we’re going to know what typically more long term we’ll know exactly what’s going to be happening with the financing of the property, plant and equipment, because those are long term in nature.

02:51

But then we have the current assets, which we might use the long term financing to finance the permanent current assets or lean more towards the long term financing to finance the the permanent current assets, because they’re always going to be turning over and we’re always going to have them there. And then the short term financing might be something that we then have more flexibility to use, when we’re thinking about the financing of the short term assets that are going to be fluctuating over shorter time periods. Now, we don’t have to use this exact breakout between this type of financing structure. This would be like the baseline type of financing structure, however, that you want to think about when breaking out the assets into temporary, permanent, and then the fixed assets. And then you can do variance from there. So in other words, typically, when we finance something with short term financing, we might have lower rates most of the time, but it’s going to be more of a risk, because we’re financing over shorter time periods.

03:51

And if we need the financing, for a longer point than we might be subject to flexibility in the interest rates that we’re going to be paying worth the long term financing is going to help us out for longer periods of time, it may be more expensive in terms of the rate, but it cannot It will also be able to be a fixed kind of rate over a longer period of time and therefore be be subject to less risk generally. So we could then we could then use different variants of this taking on more risk, and me being more aggressive with regards to the loan financing. So you want to start thinking about the loan financing between these two components, short term and long term, breaking out your loan financing and in your mind between short term and long term. The short term typically been more aggressive, but taking on more risk, the long term being less aggressive, but could be more costly.

04:46

And that’s the trade off that we’ll have so creating a financing plan. categorizing current assets into temporary and permanent can be challenging. So when we do the financing plan, notice what we’re doing here is we’re breaking out those current assets which are on the balance sheet there already. Kind of an estimate, because they’re just a timeframe of how liquid they are. And now we’re breaking them out into current and long term, which is just a structure that we’re going to use, it’s not perfect, just like many of the kind of structures that we have, when we try to make the decision making processes, we got to do the best we can on it. So that’s going to be a challenge. In order to do that, it’s also not easy to predict the exact timing of assets liquidation. In other words, when we think about those temporary current assets that have the peaks and hills and the peaks and valleys, when they’re going to basically self liquidate, it’s not easy to know exactly when that’s going to happen, we have a pretty good idea based on the seasonal pneus of the business, possibly we knew, we know half past history on it.

05:40

But it’s not a perfect thing. Therefore, when we use the temporary assets in order to finance them, we are taking more risk with regards to that. Determining the amount of short term and long term financing available can also be challenging. So when we think about this, in theory, of course, we’re thinking short term long term financing as if, you know, there’s two things that are just two options that are basically right in front of us, it could be a little bit more of a challenge in practice, to think of the different types of financing options with regards to short term and long term financing. So long term financing helps secure capital needs over a longer timeframe. So the point is, we’re going to have capital needs over the longer term timeframe will typically impossibly be able to lock down the rate over that longer term period, for example, which might make it a more secure kind of method to be using as opposed to short term, which will not secure over as long a time period.

06:29

And therefore if we need it over a longer time period, we would have to possibly roll over the financing being subject to rate change as of that time when we do that can be used to cover some of the short term needs when necessary. So we may be able to use long term financing to cover some of the short term needs. In order if we were to do that, then that might be more of a kind of less aggressive or more conservative type of strategy that we can be using to have the set financing covering some of those short term assets. So we may use long term financing to finance like fixed assets, obviously, those fixed assets are going to be fixed over the long period of time. And we might use the long term financing to cover those the permanent current assets, we might use long term financing to cover the permanent current assets, which you would expect. And we could even use some of the long term financing to cover more of the temporary current assets, which again would be a less aggressive strategy or a more conservative type of strategy.

07:26

So it might look something like this, we saw the last time that we broke out our short term financing and long term financing based on long term financing for the permanent current assets. It’s possible, say, to expand our long term financing, and then be covering some of the temporary current assets. And you’ll see what will happen then is the need that we have for financing, we’re dip below the long term financing when it goes in our troughs here. But we will also have more security with our financing needs. In case that there’s you know, some kind of problems that are that are taking place as as well. if anything changes, like some of the problems we thought in the prediction process. So this will be more, you know, conservative or less aggressive in that case, short term financing.

08:09

First thing to note that smaller businesses may not have access to as much long term financing and there might be more subject to the short term financing, they may not have the tools such as the issuance of corporate bonds for the long term financing. So the interest rates are generally lower for the short term financing. But there’s often more risk that’s going to be involved due to it being short term covering a lot a shorter period of time. And then once you have to roll over the interest or rollover the financing, if you need to take the financing out, you’re subject more to the fluctuations of the interest rates in the market at that point as well. Short term financing generally used for temporary current assets and part of the permanent capital needs. So once again, you could then expand the temporary current financing as well as a temporary financing, we saw the temporary financing typically being used our base point to cover the temporary current assets.

09:06

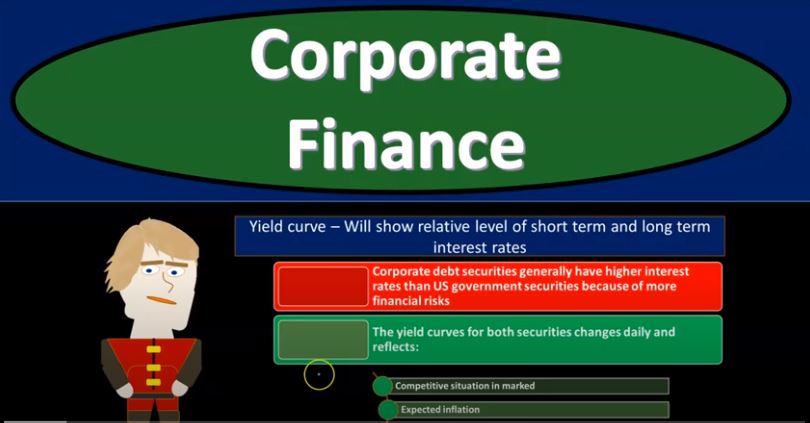

But if you want it to be more aggressive due to the fact that the temporary financing could result in lower interest rates, even though it has kind of some more risks, possibly due to needing the financing for a longer period of time and then being subject to the market for the interest rates in the future, you could then be more aggressive and take on a larger chunk of the short term financing. And that would be a more aggressive type of strategy. So just note that we saw that first slide being the baseline, meaning you’re going to have short term financing for the current assets, more long term financing for the permanent current assets. So the temporary current assets typically using short term, permanent current assets using long term but you could vary and in this case, you could be more aggressive varying towards the short term, and that could lower the interest rates but take on a bit more risk. So we have the yield curve. will show relative levels of short term and long term interest rates. corporate debt securities generally have higher interest rates than US government securities, because of more financial risk.

10:11

So when you’re thinking about the type of interest that will be charged, if there was like the issuance of debt, you have competitive interest rates at which you would need to be having in order to be able to issue the debt on the market. And you can look at corporate securities like treasury bonds. And I mean, you can look at the US securities like t bills treasury bonds, and you can look at the corporate securities and the corporate securities generally having higher interest rate, because there’s more risk involved with them than you would expect for the government bonds, the yield curve for both securities changes daily, so that yield curve is going to be changing daily. And it’s going to be changing based on the competitive competitive situation in the market, expected inflation, and changes in economic conditions. So during a recessionary time, if we’re thinking about our process going through, we’re thinking about the financing, we’re thinking about items that can be taking on risk, we’re basically breaking out our financing into short term and long term financing.

11:12

And then what you would then think about is a normal times what would happen, and what would happen in terms of worst case, or best case scenarios in times of recession, and times of upward growth. So if there was a recession, of course, you would think there would be a decline in the sales, the the cash receivables and inventory you would think would fall during every session. So caches are going to be going down, the receivables hopefully will be paid off and not be in default, but they will still be going down because they’re not going to be replenished with the new sales that are taking place. And inventory will typically fall as we as we don’t purchase more inventory due to the fact that we don’t have any, you know, if there’s a decrease in the sales, so then the short term debt could then rise in the case of a recession. And there might be a limits as to how much financing would be available in the point in the case of a recession. So if you’re too highly leveraged at that time, if you took on too much risk, if you have a lot of short term financing, that is going to be coming due.

12:14

And then there’s a recessionary period could be more difficult than to re up that financing. Whereas if you took if you take a more conservative approach and you had the long term financing, then you may be over financed in those cases, but you may be you may, you may be able, obviously to have the financing that would be needed over over the time period, and not deal with the fact that the financing might be more difficult to come by at that point. So during upward trend, if there’s an upward trend in the market, things are going well, the cash receivable and inventory you would think would then increase obviously cash would be going up receivables, the baseline would be going up because we would be making more sales at that time would be increasing the receivables, we would be increasing the inventory in order to meet the higher level of sales that are taking place, short term debt can fall or be replaced by low cost long term debt.

13:09

So in the case of this, this increasing process, we would be thinking that the receivables that are permanent, if it’s a long term type of process, the more permanent current receivables possibly would be going up, and possibly then we would be replacing some of the temporary financing we had with more permanent financing. In those situations. Strategies a firm comfortable with risk may choose more short term borrowing and luxury of liquidity while I firm more risk averse or conservative may choose more long term financing and have a higher degree of liquidity. So we’ll take a look at some some comparisons and some example problems highly recommend going through some example problems here. So note we’re talking about two different things here in terms of the liquidity of your assets, we’ll talk about the liquidity of the assets, and then how you’re going to be financing those assets.

14:03

So in other words, if you’re talking about the asset side of the accounting equation, we’ve got the assets equal the liabilities, plus the equity, on the asset side of things, we got the current assets and long term assets. Now you might be in an industry where you have the question as to whether or not you want to be leaning towards more towards the current assets, or long term assets. For example, you might be an industry where your your competitive advantage is to put your assets into property, plant and equipment, for example, which would be more long term type of assets, those assets are going to then be locked down at that point, which could lead to more leverage. In the future. We talked about basically operating leverage and whatnot, it could be beneficial and give you that competitive advantage that you’re looking for.

14:51

But it also comes along with more risk because more of your assets are going to be locked up in the fixed assets. And so if there’s flux In the markets, you when there’s a downturn, then you could have problems with that, as opposed to having a more flexible strategy. So you could choose that to enter a market, possibly one that is more flexible or more volatile. And say my strategy is to be that I’m going to have more liquid assets, take on less risk by fixing the assets in say, property, plant and equipment and be able to very possibly with the use of labor or something like that, where I can increase and decrease the hours as needed with the volatility of the market. And that would be a more, that would be a less risky kind of strategy, because you don’t have like the operating leverage that would be involved with that.

15:39

And you can fluctuate with the market. So that’s one thing that you can change the asset mix, and think about, and obviously, those two things would change with regards to the industry that you’re going into. So some industries will simply be higher, need more fixed assets, or permanent assets or property, plant and equipment than other assets. And some will be dealing with the strategy that you will be taking when you go into that. And then the next thing to think about is the is the financing. So when you think about the financing, you can be more or less aggressive with the financing. And we basically brought the financing into two categories. We have the the short term financing, and the long term financing that we’re basically considering. If you lean more on the short term financing, you’re taking on more risk, but you may have you may be get more better rates there. So that could be a more aggressive strategy. If you’re focusing more long term financing, you’re locking down your financing needs for a longer period of time, which makes you more secured for that degree that you’ll have the financing needed for a long period of time and possibly, but possibly have the longer rates even though they will be locked down.

16:43

So less risk, but it could be more costly there. So those are the two kind of variables. And you can see there will be combinations between those variables, right short term, you can have more liquid versus less liquid acid structure, obviously, it’s more of a spectrum than one or the other type of thing. But you could start thinking about you know, high or low. And then when we go to the to the liability side of things, more short term versus long term, and we can think about that on as two spectrum type of components and then start to mix and match and you can think about the projections and you can imagine the projections that could be brought about into projecting into the future based on these variables and we’ll take a look at some of those in our practice problems.