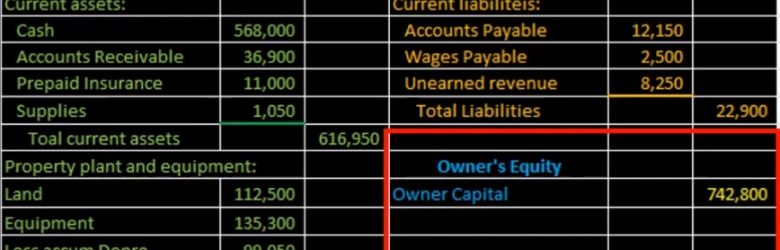

Hello in this lecture we’re going to be creating the equity section of the balance sheet. In prior lectures, we have taken a look at the current assets section, the property plant and equipment section and then the liability section. This will be rounding out the balance sheet where we will finally get to total assets being equal to total liabilities and equity represent in the double entry accounting system. In terms of the balance sheet in terms of the accounting equation, we of course, are pulling these numbers from the adjusted trial balance. the adjusted trial balance also represents the double entry accounting system. However, it represents that double entry accounting system in the format of the building blocks of debits and credits. All we’re doing is taking those building blocks in terms of debits and credits, rearranging them to the accounting equation, so that readers who don’t understand debits and credits can then read them. Now when we look at the equity section, this is a bit confusing when we convert from the trial balance to the equity section.

Posts with the Liabilities tag

Balance Sheet Liability Section Creation From Trial Balance 14

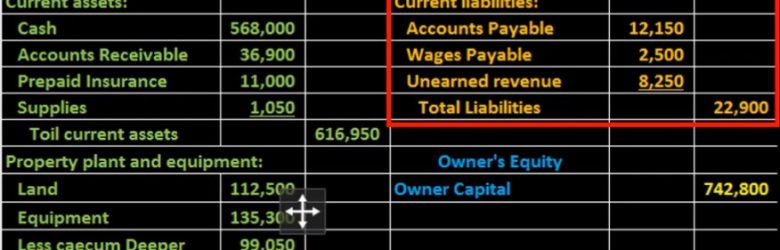

Hello in this lecture we’re going to create the liability section of the balance sheet. In prior lectures, we have taken a look at the assets in terms of first current assets and then property, plant and equipment and given us the total assets at that time, then we are now going to move on to liabilities, and that will be part of the second part of the balance sheet meaning it’ll then sum up to total liabilities and owner’s equity. We are going to be taking this information of course from the adjusted trial balance the adjusted trial balance in the format of debits and credits, we are now formatting it in the format of the accounting equation. Still the double entry accounting system just in two different formats, just reshuffling the puzzles so that different readers can understand the financial statements even though they don’t understand debits and credits.

Balance Sheet Current Assets from Trial Balance 12

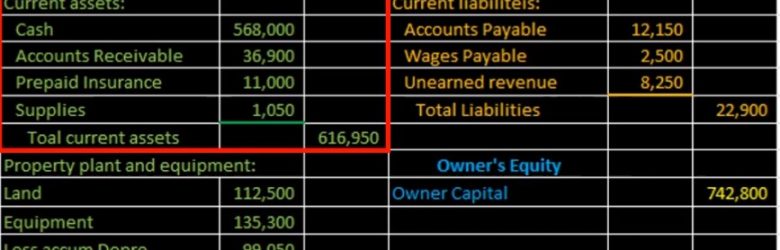

Hello in this lecture, we’re going to create the current asset section of the balance sheet, we’re going to create this current asset section from a trial balance, we’re going to piece together the financial statements piece by piece as we go through a series of lectures, the trial balance being here at this is going to be the adjusted trial balance. And what will happen is we will then find a home for all of the accounts on the financial statements. Once we then do that, that means that we have then converted this from the double entry accounting system being in the format of debits minus credits equaling zero or debits equaling the credits to the assets equals liabilities plus the owner’s equity, basically the accounting equation, which is reflected on the balance sheet. So we’re going to start off by doing the current assets section, which will just be this part we’re going to find a home for these first few accounts.

Adjusting Entry Wages Payable 7

Hello, in this lecture, we’re going to record the adjusting entry related to payroll, we’re going to record the journal entry up here on the left hand side and post that post that to the trial balance over on the right hand side trial balance in terms of assets and liabilities, then equity and the income statement, including revenue and expenses, all blue accounts, including the income statement being part of equity, we’re first going to go through and see if we can find the accounts that will be related to a payroll adjusting entry. And then we’ll go explain why we are going through this process. So just if we have the trial balance, and we know it’s an adjusting entry related to payroll, we know that there’s going to be at least two accounts affected. And we know that because it’s an adjusting entry, it will be as of the end of the time period. In this case, let’s say it’s the end of the year 1231.

Accounts Payable Journal Entries 240

Hello in this presentation we will be recording a business transactions related to accounts payable or the purchases cycle recording these transactions with debits and credits. At the end of this we will be able to list transactions involving accounts payable, record transactions involving accounts payable using debits and credits and explain the effect of transactions on assets, liabilities, equity, revenue, expenses and net income. We’re going to be recording these transactions up here in the left hand side in accordance with our thought process. We will then be posting these not to the general ledger but to a worksheet format so that we can see a quick calculation as to what is the impact or effect on the individual accounts as well as the effect on the account groups as a whole. Remember that all the groups for the accounts will always be listed in order when you’re looking at a trial balance. Which is why I recommend looking at a trial balance.

Debits & Credits 205

Hello in this presentation we will discuss debits and credits. Objectives at the end of this we will be able to define debits and credits list account normal balances and explain how debits and credits work. First we want to take a look at the double entry accounting system and recognize that the double entry accounting system can be represented in multiple different ways including as we have seen before the accounting equation meaning that assets equal liabilities plus equity, we can record transactions using this accounting equation as we have done in the past. That accounting equation is the basis behind the balance sheet where we have the assets liabilities and equity representing the fact that the balance sheet then would be in balance.

Accounts Payable Transactions Accounting Equation 170

So there’s gonna be problems later on where they’ll basically say, you know, you got to pay off something on account and you have to assume that the prior transaction took place. You got to kind of know in your mind how these things are related. So if we go through them by cycle that will help to achieve that goal. first transaction, we’re going to say purchase supplies on account. If we go through our list of questions, we’re going to say is cash affected? In this case? No, because we purchased it on account, then we’re going to ask what we’ve received, in this case supplies. So we got supplies, that is here, it’s going to be an asset. Therefore the asset is going to go up because we got more of them, then the only question is, what is the other account? It’s not a decrease to cash because we didn’t pay cash. And therefore we must be doing something somewhere else. That will be accounts payable, so accounts payable is going to increase by the same amount.

Accounts Receivable Transactions – Accounting Equation 167

Hello in this presentation we will record transactions related to accounts receivable recording the transactions using the double entry accounting system in the format of the accounting equation that equation of assets equal liabilities plus equity objectives at the end of this we will be able to list at transactions involving accounts receivable and record transactions involving accounts receivable using the accounting equation. We will go through some examples of the accounting equation and recording transactions related to accounts receivable quick review of the accounting equation we have assets equal liabilities plus equity as the accounting equation. We then need to start memorizing those accounts that fit into those subcategories of assets, liabilities and equity.

Cash Transaction – Accounting Equation 165

Hello, in this presentation we will be taking a look at business transactions involving cash we will be recording these normal business transactions in the format of the accounting equation and later be using the same or similar transactions to record with regard to debits and credits. Objectives. At the end of this we will be able to list transactions involving cash record transactions involving cash using the accounting equation. first transaction, we’re going to list through these transactions and we’re going to record these transactions with the accounting equation, learning these accounting equations and these transactions using our normal rules and thought process. So remember that this is our accounting equation, we’re going to have assets liabilities and equity.

Financial Transaction Thought Process 160

Hello in this presentation we will be discussing the transaction thought process, a thought process used to record transactions in a systematic way. Objectives. At the end of this we will be able to list steps for recording transactions. Explain reasons for using a process when recording transaction and apply a thought process to recording transactions. First, we’re going to recap those rules we talked about in the prior presentation. If you have not seen the rules for the prior presentation, we recommend taking a look at that these rules are the rules we are going to use in order to construct a thought process. The rules being something that are just part of the process things that have to happen, the thought process being a system that we are going to use in order to learn this information as quickly and efficiently as possible and be able to record transactions as quickly and efficiently as possible.