Hello in this presentation we will be discussing the transaction rules financial transaction rules as they relate to recording financial transactions with regard to the accounting equation. At the end of this, we will be able to list transaction rules explained our reasons for the transaction rules and apply transaction rules to recording financial transactions. First rule, at least two accounts will be affected. It’s going to be whenever we record any transaction and whether we’re talking about a transaction for recording payroll record an accounts receivable, recording accounts payable, all those normal things that the accounting department does on a day to day basis.

Posts with the Liabilities tag

Statement of Owner’s Equity 131

Hello in this presentation we will describe the statement of equity objectives, we will be able to at the end of this describe the statement of owner’s equity, list the components of the statement of owner’s equity and explain the reasons for a statement of owner’s equity. When we consider the statement of owner’s equity, we are like the income statement and unlike the balance sheet, talking about a timeframe, meaning we have a beginning and end point, unlike the income statement, the beginning point is not zero meaning we are going to start at the beginning point of the net value or the equity section of the prior balance.

Balance Sheet 120

Hello in this presentation that we will discuss the balance sheet objectives at the end of this presentation that we will be able to describe the balance sheet, list the components of the balance sheet and define and explain each component of the balance sheet. When considering the balance sheet, we will be looking at components equivalent to those in the accounting equation. the accounting equation as we have seen in a prior presentation is assets equal liabilities plus equity, these will be the components of the balance sheet.

Accounting Equation 115

Hello in this presentation we will discuss the accounting equation. At the end of this we will be able to name the accounting equation, explain the components of the accounting equation and explain the balancing concept related to transactions. The double entry accounting system can be recorded in a few different ways, at least three different ways. It’s useful to understand these three different ways. The first way the one we will be concentrating on here will be in the format of the accounting equation, assets equal liabilities plus owner’s equity or just equity.

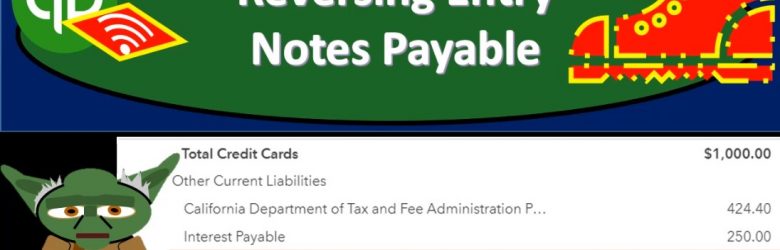

Reversing Entry Notes Payable 10.17

In this presentation, we’re going to enter a reversing entry related to notes payable. Let’s get into it within two, it’s QuickBooks Online. Here we are in our get great guitars file, we’re going to start off by opening up our report on the left hand side favorite report balance sheet reports what we’re going to be starting off with, let’s open up that balance sheet. Let’s change the dates up top to those familiar dates we’ve been working with remember and emphasizing the cutoff date, oh 10120, the cutoff date being Oh to 29 to zero because that’s when we’re going to be entering our adjustments.

Short Term Loan Adjusting Entry 10.10

This presentation we will look into recording and adjusting entry related to a short term loan. Let’s get into it with Intuit QuickBooks Online. Here we are in our get great guitars file. Let’s first take a look at our reports our balance sheet report for this transaction that we’re going to be recording or this adjusting entry, we’re going to be opening up our favorite report that being the balance sheet report, we’re going to change the dates up top the dates from let’s make it a 1012020 229 to zero. Now, when we think about the adjusting entries, we’re always going to be thinking of them as kind of like the cutoff dates, we’re trying to make things correct as of the cutoff date, which in this case, it’s going to be the end of the second month.

Balance Sheet Liability Section Creation From Trial Balance

Balance sheet, liability section from trial balance. Creating the liabilities section of the balance sheet from trail balance.

Why Learn Accounting – Financial Accounting / Managerial Accounting

https://youtu.be/uaWDB1YdA1k?list=PL60SIT917rv52SlrB3FFn2WMyZEkj6uBI

101 Double Entry Accounting System Explained – Accounting Equation

https://youtu.be/66e9QbrkE4g?list=PL60SIT917rv52SlrB3FFn2WMyZEkj6uBI

101 Cash vs Accrual – Cash Method / Accrual method differenc

https://youtu.be/i2O0cexCrqc?list=PL60SIT917rv52SlrB3FFn2WMyZEkj6uBI

101 Revenue Recognition Principle

https://youtu.be/M_pauBGz5Jc?list=PL60SIT917rv52SlrB3FFn2WMyZEkj6uBI

Double Entry Accounting System Explained – Balance Sheet

https://youtu.be/kOItl8E3fNA?list=PL60SIT917rv52SlrB3FFn2WMyZEkj6uBI

101 Income Statement Introduction

https://youtu.be/1k11H8icQxc?list=PL60SIT917rv52SlrB3FFn2WMyZEkj6uBI

101 Accounting Objectives – Relevance Reliability Comparability

https://youtu.be/mO8tPzFmN8o?list=PL60SIT917rv52SlrB3FFn2WMyZEkj6uBI

101 Transaction Rules – Accounting Equation

https://youtu.be/0vy6W_WTO2I?list=PL60SIT917rv52SlrB3FFn2WMyZEkj6uBI

101 Transaction Throught Process / Steps – Accounting Equation

https://youtu.be/SlTo3EXDuqU?list=PL60SIT917rv52SlrB3FFn2WMyZEkj6uBI

101 Owner Deposits Cash Transaction Accounting Equation

https://youtu.be/lPZoImc88eU?list=PL60SIT917rv52SlrB3FFn2WMyZEkj6uBI

101 Work Completed for Cash Transaction Accounting Equation

https://youtu.be/ll5xIHVdrVs?list=PL60SIT917rv52SlrB3FFn2WMyZEkj6uBI

100.110 Pay Employee with Cash Transaction Accounting Equati

https://youtu.be/bSa3NuVpkwc?list=PL60SIT917rv52SlrB3FFn2WMyZEkj6uBI

200 Debits & Credits Normal Balance – Double Entry Accounting Sy

https://youtu.be/alSWKuWPlxU?list=PL60SIT917rv52SlrB3FFn2WMyZEkj6uBI

200 Debits & Credits – One Rule to Rule Them All

https://youtu.be/RL3BFjL1eyE?list=PL60SIT917rv52SlrB3FFn2WMyZEkj6uBI