In this presentation, we’re going to discuss special journals and subsidiary ledgers, both of which play crucial roles in accounting systems. These tools are particularly useful when dealing with manual accounting systems, as they streamline data input and make financial reporting more efficient. However, they also offer valuable insights for understanding and customizing automated systems.

Posts in the Accounting Instruction category:

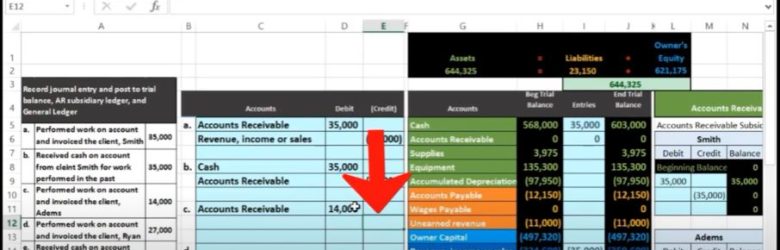

20 700.20 Accounts Receivable Subsidiary Ledger 700 Part 2-Accounting Instruction

In this blog post, we will discuss the process of posting journal entries to various accounts in the accounting system. Specifically, we will focus on transactions involving accounts receivable, revenue, and cash.

Average Deviation, Standard Deviation & Variance for Population with Salary Data 1443

In the world of data analysis and statistics, the understanding of key concepts such as average deviation, standard deviation, and variance is crucial. These metrics provide insights into the dispersion and distribution of data. In this blog, we will delve into these statistical concepts using Excel, focusing on a population of salary data as an example.

Histogram Examples Statistics & Excel 1070

Data is all around us, and extracting meaningful insights from it can be a challenging task. One powerful tool in the data analyst’s arsenal is the histogram. Histograms allow us to visualize data and gain a better understanding of its distribution. In this blog, we will explore the concept of histograms and their applications in various domains. We will also provide practical examples of creating histograms using Microsoft Excel.

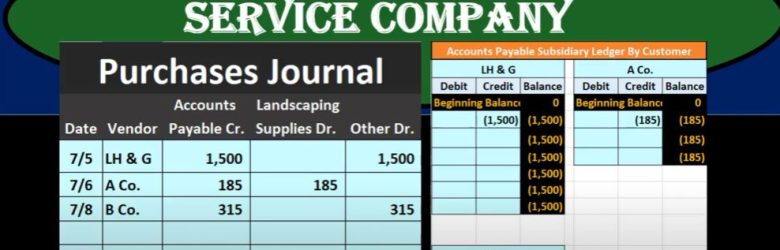

30 Purchases Journal Service Company

In this blog post, we will dive into the concept of the Purchases Journal and its significance for service companies. The Purchases Journal plays a crucial role in accounting for businesses that regularly make purchases on account, which typically results in accounts payable transactions. We will explore the purpose of this journal, its applications in both manual and automated accounting systems, and the process of recording transactions and maintaining the accounts payable subsidiary ledger.

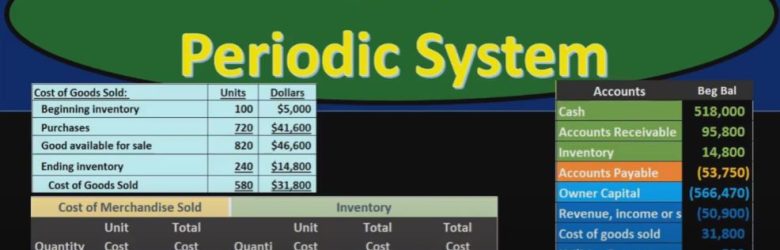

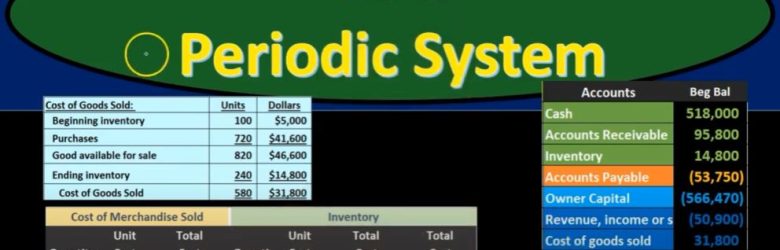

Last In First Out LIFO Periodic 44

In this presentation, we will delve into the intricacies of the Last-In, First-Out (LIFO) inventory system, focusing on the periodic inventory method rather than the perpetual one. Throughout our discussion, we will draw comparisons between LIFO and other systems, such as First-In, First-Out (FIFO) and the average cost method. Additionally, we will explore the differences between the periodic and perpetual inventory systems. To illustrate these concepts, we will use a comprehensive worksheet, which will prove invaluable for addressing various inventory flow assumption problems.

600 CPA Exam Part 1 – Inventory Methods FIFO, LIFO, Average – CPA exam & other accounting test prep

In this blog post, we will delve into the world of accounting, specifically inventory accounting. We will work through several practice problems to understand how to calculate the per unit value of ending inventory, using both the weighted average perpetual inventory system and the FIFO (First-In-First-Out) perpetual inventory method. We’ll also explore how to adjust inventory figures when errors occur. So, let’s dive right in!

Typing Mathematical Equations in Microsoft Excel 1410 Statistics & Excel

Welcome to the world of statistics and Excel! In this blog post, we’ll guide you through typing mathematical equations in Microsoft Excel, a handy tool for performing statistical calculations and data analysis. If you’re new to Excel, don’t worry—we’ll start from scratch and build our way up.

First In First Out (FIFO) Periodic System 42

In this presentation, we will delve into the concept of First In, First Out (FIFO) inventory valuation, comparing it within the context of both periodic and perpetual inventory systems. FIFO is one of the most widely used methods for valuing inventory, and understanding how it operates under different systems can be crucial for effective inventory management.

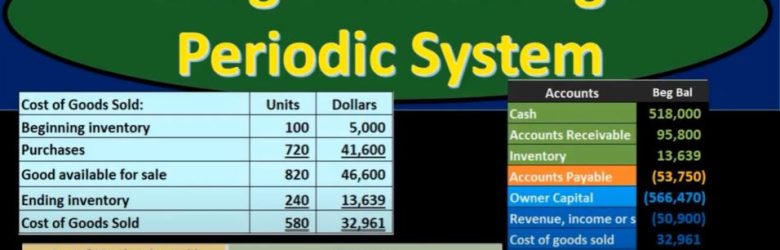

Weighted Average Periodic System 46

In this presentation, we will delve into the weighted average inventory method using a periodic system. We’ll also explore the weighted average method in contrast to the first-in, first-out (FIFO) or last-in, first-out (LIFO) methods, as well as the differences between periodic and perpetual inventory systems. To better grasp these concepts, we’ll work through an illustrative worksheet.