Hello in this section we will define the post closing trial balance. When seeing the post closing trial balance, it’s easiest to look at it in comparison to the adjusted trial balance and consider where we are at in the accounting cycle in the accounting process. When we see these terms such as the adjusted trial balance and post closing trial balance, as well as an unadjusted trial balance, we’re really talking about the same type of thing. We’re talking about a trial balance, meaning we’re going to have the accounts with balances in them. And we’re going to have the amounts related to them. And of course, the debits and the credits will always remain in balance. If it is a trial balance, no matter the name, whether it be just a trial balance on an adjusted trial balance and adjusted trial balance or a post closing trial balance.

Posts with the accounting tag

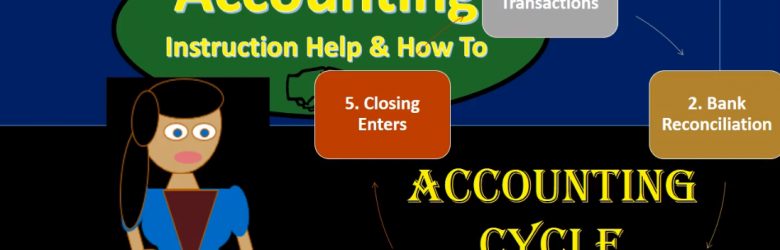

Accounting Cycle Steps in the Accounting Process

Hello, in this presentation, we’re going to be talking about the accounting cycle or the accounting process, that process that the accounting department will go through on a systematic basis over and over and over again, typically thought of as a monthly process. Although it could be thought of as a yearly process or some other process in terms of the amount of time that will pass. But these are going to be the steps that we’ll be going through in terms of the accounting process, always keeping in mind that in goal of financial accounting, which are the financial statements, some texts will have more steps than five as we have here. Some texts will have less than five steps. But the goal here is to really have a broad picture big picture, so that when we think about the accounting process, we can break down that that big picture view, five is a pretty good number for us to be able to memorize and keep in our mind if we have more than that, it can start to kind of muddy the picture.

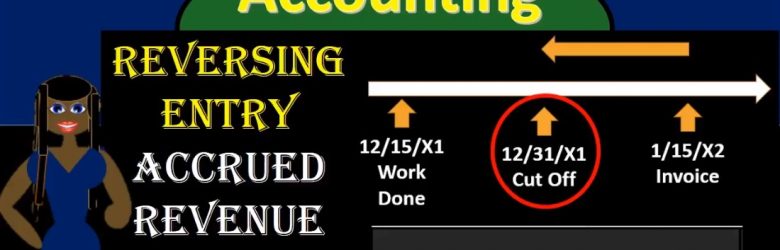

Reversing Journal Entries – Accrued Revenue 11

Hello. In this presentation we’re going to talk about reversing journal entries as they are related to accrued revenue. When considering reversing journal entries, we’re talking about those journal entries made after the financial statements have been generated after the adjusting process has been done. Remember that the adjusting process happens after all the normal transactions for the month have happened. Then at the end of the month, we have that adjusting process. All journal entries being made as of the same date as of the end of the month in order to make the financial statements correct so that the financial statements can be made. As of that point in time, in this case, the end of the year being 1231 that the cutoff date that the point in time that we make the financial statements, then we want to consider if we want to use reversing journal entries.

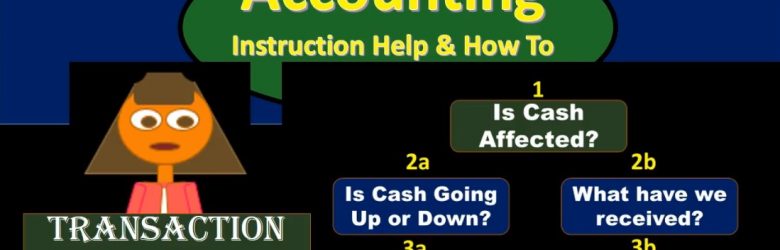

Journal Entry Thought Process 215

Hello in this presentation that we will discuss a thought process for recording financial transactions using debits and credits. Objectives. At the end of this, we will be able to list a thought process for recording journal entries. explain the reasons for using a defined thought process and apply thought process to recording journal entries. When we think about a thought process, we’re going to start with cash as the first part of the thought process is cash affected. We’ve discussed the thought process when we have considered the double entry accounting system in the format of the accounting equation, the thought process will be much the same here we now applying that thought process to the function of debits and credits recording the journal entries with regard to debits and credits.

Debits & Credits 205

Hello in this presentation we will discuss debits and credits. Objectives at the end of this we will be able to define debits and credits list account normal balances and explain how debits and credits work. First we want to take a look at the double entry accounting system and recognize that the double entry accounting system can be represented in multiple different ways including as we have seen before the accounting equation meaning that assets equal liabilities plus equity, we can record transactions using this accounting equation as we have done in the past. That accounting equation is the basis behind the balance sheet where we have the assets liabilities and equity representing the fact that the balance sheet then would be in balance.

Accounts Payable Transactions Accounting Equation 170

So there’s gonna be problems later on where they’ll basically say, you know, you got to pay off something on account and you have to assume that the prior transaction took place. You got to kind of know in your mind how these things are related. So if we go through them by cycle that will help to achieve that goal. first transaction, we’re going to say purchase supplies on account. If we go through our list of questions, we’re going to say is cash affected? In this case? No, because we purchased it on account, then we’re going to ask what we’ve received, in this case supplies. So we got supplies, that is here, it’s going to be an asset. Therefore the asset is going to go up because we got more of them, then the only question is, what is the other account? It’s not a decrease to cash because we didn’t pay cash. And therefore we must be doing something somewhere else. That will be accounts payable, so accounts payable is going to increase by the same amount.

Cash Transaction – Accounting Equation 165

Hello, in this presentation we will be taking a look at business transactions involving cash we will be recording these normal business transactions in the format of the accounting equation and later be using the same or similar transactions to record with regard to debits and credits. Objectives. At the end of this we will be able to list transactions involving cash record transactions involving cash using the accounting equation. first transaction, we’re going to list through these transactions and we’re going to record these transactions with the accounting equation, learning these accounting equations and these transactions using our normal rules and thought process. So remember that this is our accounting equation, we’re going to have assets liabilities and equity.

Change In Estimates – Financial Accounting

We will discus the accounting for a change in a financial accounting estimate related to depreciation. The calculation of depreciation is an estimate of the cost allocated to the useful life. There are a few components of the calculation that are estimates that can change as we get better information over time. One component of the depreciation calculation that is an estimate is the useful life, how long the depreciable asset will be used in operations. Another estimate in the depreciation calculation is the salvage value. When these estimates change over time it is often best to account for the change at the point it is found and going forward rather then going back and recalculating depreciation for prior years. For more accounting information see website. http://accountinginstruction.info/cou…

8.90 Rental Income Accounting Excel u

We will cover the financial transaction related to rental income. We will first take a quick look at QuickBooks and then enter the financial transaction into Excel using debits and credits. For more information about QuickBooks see our QuickBOoks 2018 course. MOre information about the online course at the link below. http://accountinginstruction.info/qui… For more information about a comprehensive Accounting and Excel course see our Accounting and Excel Course. More information about the online course at the link below. http://accountinginstruction.info/qui…

Excel vs QuickBooks 8.80 Payroll

We will enter the financial transaction related to payroll. We will first enter the accounting transaction into Excel and then enter the financial data into QuickBooks. For more information about QuickBooks see our QuickBOoks 2018 course. MOre information about the online course at the link below. http://accountinginstruction.info/qui… For more information about a comprehensive Accounting and Excel course see our Accounting and Excel Course. More information about the online course at the link below. http://accountinginstruction.info/qui…