Hello, in this presentation we will be taking a look at business transactions involving cash we will be recording these normal business transactions in the format of the accounting equation and later be using the same or similar transactions to record with regard to debits and credits. Objectives. At the end of this we will be able to list transactions involving cash record transactions involving cash using the accounting equation. first transaction, we’re going to list through these transactions and we’re going to record these transactions with the accounting equation, learning these accounting equations and these transactions using our normal rules and thought process. So remember that this is our accounting equation, we’re going to have assets liabilities and equity.

Posts with the Equity tag

Financial Transaction Thought Process 160

Hello in this presentation we will be discussing the transaction thought process, a thought process used to record transactions in a systematic way. Objectives. At the end of this we will be able to list steps for recording transactions. Explain reasons for using a process when recording transaction and apply a thought process to recording transactions. First, we’re going to recap those rules we talked about in the prior presentation. If you have not seen the rules for the prior presentation, we recommend taking a look at that these rules are the rules we are going to use in order to construct a thought process. The rules being something that are just part of the process things that have to happen, the thought process being a system that we are going to use in order to learn this information as quickly and efficiently as possible and be able to record transactions as quickly and efficiently as possible.

Financial Transaction Rules 155

Hello in this presentation we will be discussing the transaction rules financial transaction rules as they relate to recording financial transactions with regard to the accounting equation. At the end of this, we will be able to list transaction rules explained our reasons for the transaction rules and apply transaction rules to recording financial transactions. First rule, at least two accounts will be affected. It’s going to be whenever we record any transaction and whether we’re talking about a transaction for recording payroll record an accounts receivable, recording accounts payable, all those normal things that the accounting department does on a day to day basis.

Balance Sheet & Income Statement Relationship 132

Hello in this presentation we will discuss the balance sheet and income statement relationship. Objectives at the end of this we will be able to define the balance sheet and list its parts, define the income statement and list its parts and explain how the income statement relates to the balance sheet. When considering these concepts in terms of the balancing concept of the balance sheet in particular, we want to keep in mind the idea of the double entry accounting system. The double entry accounting system being the main system the main internal control, that we are always keeping in mind that internal control helping us to safeguard against making errors that’s our first line of defense against making errors is the double entry accounting system, which can be expressed in a few different ways. (more…)

Income Statement 130

Hello in this presentation we will discuss the income statement objectives. At the end of this presentation, we will be able to describe what an income statement is list the parts of the income statement and explain the reasons for an income statement. First, we’ll start off with a question will which will explain the timing of the income statement or introduce us to an explanation of the timing of the income statement? And that is the question of asking somebody, how much do you make when we were to if we were to ask somebody how much they make, they would mentally make some type of assumption in order to answer that question, or they would ask you the question if they chose to answer at all.

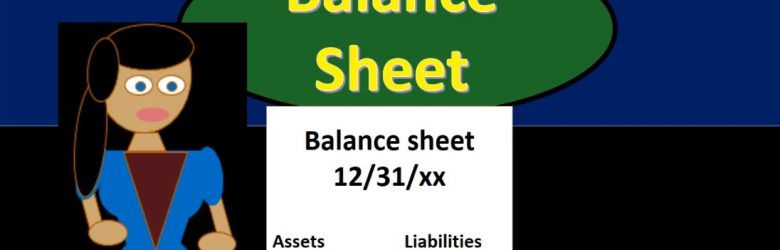

Balance Sheet 120

Hello in this presentation that we will discuss the balance sheet objectives at the end of this presentation that we will be able to describe the balance sheet, list the components of the balance sheet and define and explain each component of the balance sheet. When considering the balance sheet, we will be looking at components equivalent to those in the accounting equation. the accounting equation as we have seen in a prior presentation is assets equal liabilities plus equity, these will be the components of the balance sheet.

Accounting Equation 115

Hello in this presentation we will discuss the accounting equation. At the end of this we will be able to name the accounting equation, explain the components of the accounting equation and explain the balancing concept related to transactions. The double entry accounting system can be recorded in a few different ways, at least three different ways. It’s useful to understand these three different ways. The first way the one we will be concentrating on here will be in the format of the accounting equation, assets equal liabilities plus owner’s equity or just equity.