QuickBooks Online 2021 advanced customer deposit payment. Let’s get into it with Intuit QuickBooks Online 2021. Here we are in the get great guitars practice file, we’re going to be recording a pre payment from a customer or a deposit sometimes called unearned revenue. So let’s first open up our balance sheet and income statement reports. We’re going to go up top right click on the tab up top, duplicate, we’re going to duplicate again, right click on the tab up top and duplicate again. So we got the double duplications.

Posts with the Revenue tag

Sales by Customer or Income by Customer Reports 4.20

QuickBooks Online 2021. net sales by customer or income by customer reports. Let’s get into it with Intuit QuickBooks Online 2021. Here we are in our free QuickBooks Online test drive file, which you can find by searching within your favorite browser for QuickBooks Online test drive, we’re in Craig’s design and landscaping services. Going down to the reports on the left hand side, we’re going to be opening up reports for sales by customer, this is going to be supporting a line item on the income statement. So let’s scroll on down. We’re looking for this sales type of reports.

Profit & Loss, P&L, Income Statement Overview 3.10

QuickBooks Online 2021 Profit and Loss P and L income statement overview. Let’s get into it with Intuit QuickBooks Online 2021. Here we are in our free QuickBooks Online test drive practice file, which you can find by searching in your favorite browser. For QuickBooks Online test drive, we’re in Craig’s design and landscaping services practice file, we’re going to go into the profit and loss or income statement by going to the reports down below, we’re going to be opening up the standard profit and loss which should be in your favorites because it is a favorite report, profit and loss report, otherwise known as an income statement, sometimes called or referred to, in short as the P and L,

Customer, Sales, Revenue, or Accounts Receivable AR Cycle 1.30

QuickBooks Online 2021 customer sales revenue or accounts receivable AR cycle. Let’s get into it with Intuit QuickBooks Online 2021. Here we are in our Google search page, we’re going to be searching for QuickBooks Online at test drive, then we’re going to be clicking on the QuickBooks Online test drive for Intuit, the owner of QuickBooks, verifying that we are not a robot and continue. Here we are in our Craig’s design and landscaping services practice file, we’re going to hit the New button on the left hand side last time or in the prior section, we took a look at the items under the vendor section now we’re going to be taking a look at the items under the customers section. Remember that every business transaction has two sides to it.

Fund Raising Purposes 121

In this presentation, we’re going to set up and analyze the function of purposes within our accounting software, the purposes are going to be similar or serve a similar function as the items like inventory items and service items in a for profit organization. Get ready, because here we go with aplos. Here we are on our not for profit organization dashboard. Last time, we were over here in the accounting section, and we set up our chart of accounts and we set up our tags. Now we’re going to be going into the donations section we’re going to go into the donations, this is going to be our revenue type of site of section if you’re thinking about this as a comparison to a for profit type of organization, is how we’re going to be generating revenue with those donations.

The Nature of Asset Growth 605

Corporate Finance PowerPoint presentation. In this presentation, we will discuss the nature of asset growth, get ready, it’s time to take your chance with corporate finance, the nature of asset growth, we’re going to start off with working capital management, what is working capital management, the financing and management of current assets of the company. So when we consider this, let’s think about the accounting equation assets equal liabilities plus equity, remember that the assets are what the company has, why does the company have them in order to help generate revenue to get a return on the assets in order to help generate revenue?

Financial Leverage 520

Corporate Finance PowerPoint presentation. In this presentation, we will discuss financial leverage, get ready, it’s time to take your chance with corporate finance, financial leverage. Now remember, when you hear the term leverage, you’re typically thinking of two different categories, that being financial leverage. And then the operating leverage the financial leverage, usually the one that most people think of when they think of leverage having to do with the leverage related to the debt, the operating leverage having to do with their leverage related to the cost structure between the variable cost and the fixed cost, the operating leverage having the leverage component when you have the in the fixed costs.

Leverage Overview 505

Corporate Finance PowerPoint presentation. In this presentation, we will give an overview and an introduction to the concept of leverage. Get ready, it’s time to take your chance with corporate finance, leverage what is leverage use of special forces or effects to magnify outcomes given certain conditions. Let’s break that down a little bit more detail use of Special Forces sounds kind of mystical here. But there’s a couple different things that we think about with leverage. And we typically break it down into operating leverage and financial leverage. Most people when they think about leverage, they’re thinking about debt, they’re thinking about the leverage related to the debt will also have leverage related to operating leverage, which has to do with the mix between fixed costs and variable costs. So on so we have these special forces or effects have magnify outcomes. So that could magnify outcomes.

Pro Forma Balance Sheet 420

Corporate Finance PowerPoint presentation. In this presentation we will discuss a pro forma balance sheet or budgeted balance sheet. Get ready, it’s time to take your chance with corporate finance pro forma balance sheet. As we think about the pro forma or budgeted balance sheet, let’s take a step back and see where it fits in with our projections with our pro forma statements, you’ll recall that the place we need to start then is going to be the sales projections, we need the sales projection, we’re first going to think about how far we’re going basically the activity type of statement. And then we’ll take that change that activity statement how far we went, like miles driven in and our income statement, and then we’ll tack on the beginning balance where the odometer was at at the beginning to get to the ending point, which is going to be the ending balance sheet.

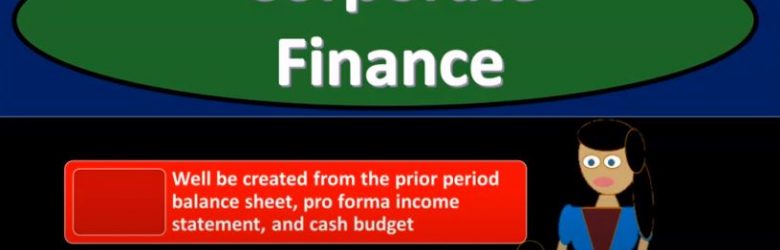

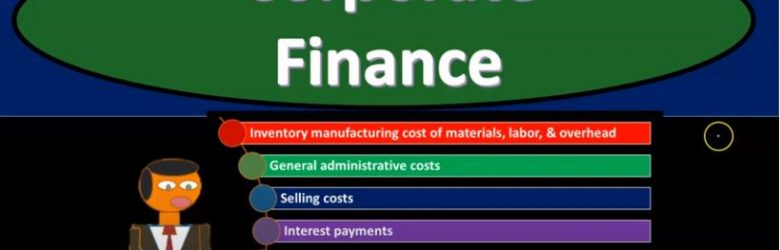

Cash Budget 415

Corporate Finance PowerPoint presentation. In this presentation, we will be discussing the cash budget Get ready, it’s time to take your chance with corporate finance, cash budget, as we consider the cash budget, let’s take a step back and think about the budgeting process. So we can think about where the cash budget will fit in it. So we got to start off with the sales projection, that’s going to be our first step. So we can think about the production plan if we manufacture inventory, or we think about the purchasing plan. If we purchase and sell inventory, then we can think about the pro forma income statement. Now the pro forma income statement is going to be on an accrual basis. But we also want to be considering the cash budget. So obviously, once we have once we start to construct the income statement, on an accrual basis, we can also think about what the cash flows will be.