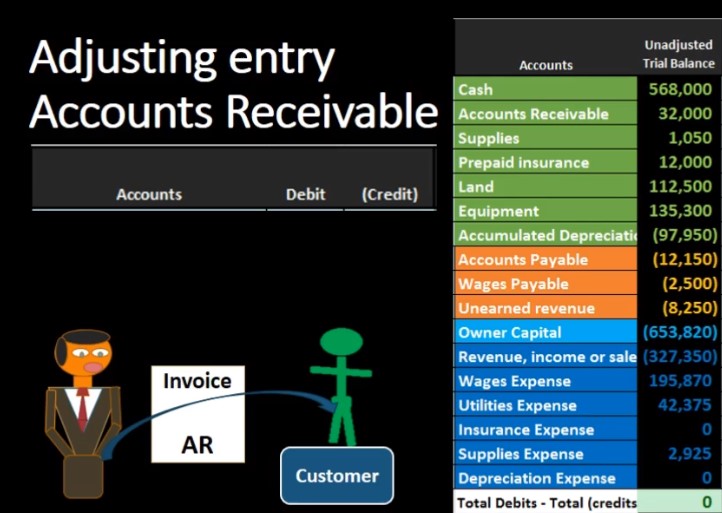

Hello in this lecture, we’re going to record an adjusting transaction related to accounts receivable. We’re going to record the journal entry over here on the left hand side and then post it to the trial balance on the right hand side trial balance and format of assets in green liabilities in orange equity in the light blue and the income statement in the darker blue including revenue and expenses, we’ll first walk through which accounts will be affected and then explain why that is the case. So we know that it is an adjusting entry and knowing that it’s an adjusting entry means it’s slightly different than a normal journal entry in that it does have two accounts like normal journal entries, but it also generally has one income statement account below the blue line and one balance sheet account above the blue line the light blue line, so it’s going to be one account above owner’s equity, one account below owner’s equity.

00:46

If we know that and we have the trial balance, we can kind of look for those accounts first, and then work from there. So we’re going to say okay, what accounts going to be related to accounts receivable in this case? How about accounts receivable and then on the income side In the account below the blue line, we’re gonna say what accounts can be related to accounts receivable a little bit more tricky to figure this out. And it kind of depends on what the wording of the problem would be. But typically the account related to accounts receivable is revenue, that’s going to be the income statement account that’s related to accounts receivable accounts receivable. So note, we can figure that out just by knowing it’s an adjusting entry and know when it’s related to accounts receivable. We can even know which way the accounts are going how well this is an income statement account down here, income statement accounts only go went one way they go up revenue has a credit balance represented by the bracket.

01:32

Therefore in order to make it go up, we’re going to do the same thing to it, which in this case would be a credit. So we’re going to credit revenue and if we’re going to credit revenue, then we’re going to have to debit the other account, which of course, we said is accounts receivable. So we know all that just by knowing it’s an adjusting entry related to accounts receivable without knowing really what’s going on. Now, let’s talk about what’s really going on. Why are we doing this. The thing that can be confusing about this in terms of an adjusting entry is that it looks just like and it is the same as a normal trend. transaction. When we make an a sale on account, if we did work on account, we would then issue an invoice. And normally when we invoice the client, that’s when we record this exact journal entry, we debit accounts receivable and credit sales. Why then hasn’t the accounting department done this, this seems like their job to do this type of journal entry. And what happens is there’s a timing difference, just like all the adjusting entry accounts.

02:22

And you can think about this in terms of like a legal office or a CPA office, where we have to gather the time together. Before we enter the invoice, we got to go through all the people in the office that worked on billable hours and put them together and then multiply that times the rate in order to get the invoice together to be sent out. Therefore, it’s very possible that the invoice went out, for example, in January next year, even though we’re making the financial statements as of 1231. And the work was done in December. So the work may have been done in December, but we didn’t build it until January. We’re not going to receive the cash until sometime after that of course because we sent the bill out and then we’re going to receive the cash Therefore, the accounting department did it right, it’s just that it took some time in order to issue the invoice.

03:06

And we’ve got to pull that back into this time period, because we need to recognize revenue when it has been earned under the revenue recognition principle, that’s going to be the idea here. Now, they’re gonna usually just give us the number here, someone’s going to give us the number, we’re going to say that’s going to be that 4900. And what happened of course, what we’re saying here, that invoice did not yet go out, it went out next month. So that’s what is happening. And we’re gonna have to reverse this entry next month, so we don’t double count it but as of the cutoff date, we need to pull that income into the financial statements as of the cutoff date. Therefore, we’re going to debit the accounts receivable 4900 and the revenue by that 4900. If we post that out, then we have accounts receivable at 32,000 before we’re debiting a debit balance account by 4900.

03:53

Bringing the account up to 36,900. We have the revenue account at a credit of 327 350 we’re going to credit that account by the 4900 doing the same thing to it and revenue goes up as it always does to 330 to 250. We can look at the accounting equation assets went up, of course, because accounts receivable is an asset, and it increased, nothing happened to the orange liability accounts and that means that equity two has gone up why income went up, bringing net income up net income is part of total equity. Therefore total equity went up as well. If we consider just net income by itself at this point, we can see that we had net income before of 86 180 revenue credit minus expenses debits meaning credit credits, our winning income of 86 180 and then we brought it up by 4900 to 91,080 from this journal entry