Corporate Finance PowerPoint presentation. In this presentation, we will give an introduction to ratio analysis. Get ready, it’s time to take your chance with corporate finance, Introduction to ratio analysis. So once we have the financial statements, then we want to think about how best to use those financial statements for decision making purposes. So remember, then the two primary financial statements being the balance sheet and the income statement, we can think of them answering primary questions that a user of the financial statements may have, such as an investor or someone who’s thinking about investing into the company may want to know where the company stands as of a point in time, that once again, is the balance sheet.

00:42

If we’re an investor, we’re thinking about the accounting equation, possibly as the value of the company at this point, which you can think of is the book value as assets minus liabilities equals equity, therefore, equity being the book value as of a point in time, then we have the time frame question in terms of the question would be for an investor, how much money will they make in the future? How much earning potential Do they have, we can’t have a financial statement for the future because it hasn’t happened yet. But we can base the future on past performance. Therefore, we need the past performance statement, that typically being the income statement is the primary statement we would think of as past performance, we then have the statement of retained earnings, which is kind of linking together balance sheet and income statement. And then we can kind of think of the statement of cash flows as a reworking, in essence, the financial statements from an accrual basis to something on a cash basis, so then we can zero in on the cash flow. When thinking about financial analysis, we are usually comparing the balance sheet and the income statement.

01:42

So we’re taking numbers on the balance sheet and the income statement. So when we look at these two statements, we can look at them in and of themselves. But then when we want to see them within context, we want to be comparing them to other companies. So if we’re an investor, we want to compare them to other companies to see how they stack up with relation to other companies, both in terms of where they stand at this point in time, as well as what their future earning potential may be. If we’re a bank and thinking about giving a loan or something like that, we want to see whether or not they’ll be able to pay back the loan. So we want to know, you know, similar information, but where do they stand? Do they have the ability to pay back the loan with earnings that they are likely to make in the future, if we’re management within the company, then we want to be benchmarking to other companies and see how we’re performing with relation to those other companies to see if we can increase our performance.

02:32

All of those things are going to are going to need information from the financial statements. But we’re also going to need ratios. And this is often very intimidating to many people, because many people don’t aren’t comfortable with ratios. And what ratios can tell us and many people are actually skeptical about the information given by ratios because because we worry about people basically lying to us with statistics presenting statistics in a way that doesn’t represent the true story. But note that we have to have statistics statistics is the only way to have any kind of fair measurement between performance measures such as job performance, or sports performance, or business performance. The statistics are just a fact of the matter. But notice that facts can be used to deceive. And that’s the problem.

03:18

And that’s the same with any kind of fact, any kind of rhetoric, if someone is using rhetoric, in order to deceive, what they’ll do is they’ll take some piece of truth, and then they’ll build a fictitious story around that one little kernel of truth. And with rhetoric, we get pretty good at being able to pick that out. We’re like, well, you kind of took one little piece of truth there. And then you made a whole story that makes no sense around that little piece of truth. Well, the same thing can be done basically, with statistics, if someone gives you one piece of statistic, then they can build a story around it even though that statistic is true. But the story doesn’t make sense. Because they are not giving you the whole story. They’re withholding this the whole story and just giving you one piece and then constructing a different narrative than what one that may be factual. So just like with rhetoric, we need to do with statistics, we got it, we got to expand the story and say,

04:07

Okay, I see we’re, you know that that one piece of truth, I agree with that. But I’m not sure that the rest of the story lines up. And that’s why we need more facts. And we need to take a look at this information from more angles. That means that no one statistic, just like no one piece of fact, can be used to construct an entire narrative, what we’re trying to do usually is predict into the future, which is something that’s unknown. And therefore we’re gonna, we’re gonna need multiple different angles, multiple different kinds of statistics that we’ll take a look at, in order to project into the future. Now, you might also say, Well, why can’t I just use the numbers on the balance sheet in the income statement and look at the change or compare my balance sheet numbers to balance sheet numbers of other businesses? You can’t You can’t do that because other businesses might have a different frame that they’re working in.

04:53

Meaning, if you’re trying to benchmark to a company that is larger than you are, then you can’t really bend Mark your dollar amounts to them or their change in dollar amounts. But you can compare certain relationships between your numbers to their numbers in a similar way, as if you’re majoring someone’s job performance, such as measuring the job performance of a baseball player, and you’re trying to measure how many hits they have, you can’t compare to people that that didn’t have the same amount of at bats, they didn’t have the same amount of chances to hit the ball. But you can make you can take a statistical average. And then you can make a measurement of it, that and notice that baseball is just one format of job performance. So the same thing is going to be true with any job. So any kind of review, if someone’s trying to give you a review of your performance versus some other person’s performance, they’re going to have to use ratios in some way to do it accurately.

05:47

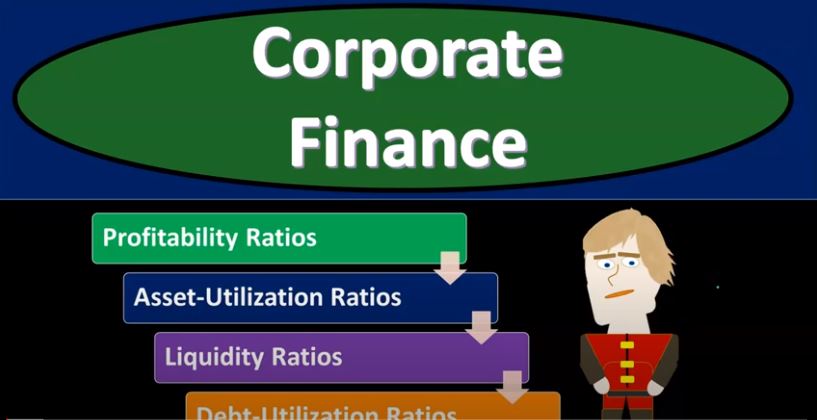

And once again, you what you want to do is be able to understand ratios in general, so that you can then be able to expand the picture and explain or note when people are not representing ratios fairly or are given, you know, one ratio and construction an entire narrative based on limited information. So those are some of the objectives we have with the ratio analysis. So financial ratios are going to be used to calculate it to analyze operating performance of a company used to compare performance against companies in a similar industry. So remember, once we have the financial statements set up, we want to compare, and we want to compare to our past performance, we want to compare to industry performance. And to do that we need we need ratio analysis. So the financial ratios are typically broken down into categories, I’m going to go over the categories first, then we’ll list the ratios within the categories.

06:40

And then we’ll break down those ratios a little bit more about what they’re going to do. And then we’ll give you the actual formulas for the ratios. And then I highly recommend going through multiple problems we’ll get we have a ton of problems that you can go through and actually calculate these ratios. And once you start doing them, once you get used to them, these ratios will become more familiar with you and you and you’ll there’ll be more natural, they’ll be something that you’re comfortable talking about. And so we have the profitability ratios, we have the asset utilization ratios, liquidity ratios, and debt utilization ratios. So let’s take a look at the profitability ratios, we’re just going to list them out first, and then we’ll go into them in a little bit more detail. Once again, you really pick this stuff up from actually doing the calculations, which we got will have a lot of problems on that you can take a look at those and work with the ratios for a while until you you’re comfortable with them.

07:33

So we have the profit margin, we’ve got the return on assets or investments are oae. We’ve got the return on equity for the profitability ratios, we got the asset utilization ratios, we have the receivable turnover, the average collection period, the inventory turnover, the fixed asset turnover and the total asset turnover. Then we have the liquidity ratios, which include the current ratio and the quick ratio. Then we have the debt utilization ratios, which include the debt to total assets, the times interest earned and fixed charge coverage. So profitability ratios, we’re going back up to the top now looking at the profitability ratios, which include profit margin, return on assets or investment, and return on equity. So these are going to measure a company’s ability to earn sales, assets and investments. So when you’re when you’re thinking about the profitability, you’re thinking about kind of performance measures.

08:31

So notice, you’re typically dealing with things on the income statement or thinking about how much earnings you had with comparison to the resources that you had in order to basically generate those earnings. Then we have the asset utilization ratios. Those include these items on the left, which we listed out prior receivable turnover average collection period, inventory turnover, fixed asset turnover, total asset turnover, these measure the speed that a company turns over the accounts receivable, inventory, and long term assets.

09:04

So in other words, we want to turn these things over faster. Accounts Receivable represents the money that is owed to us, we want to turn over the receivables, meaning collect on them sooner, because that’ll increase the cash flow and that will be more make it more likely that we will actually collect on the receivables inventory, we want to turn those things over we want to turn over the inventory quicker, because the more we can turn over the inventory, the less inventory we will have on hand at any point in time, less cost of handling the inventory. And we’re going to if we turn it over faster, we’re going to be generating more revenue. However, we have to balance that out with with basically making sure we have enough inventory to cover any kind of any kind of problems that could happen so that we can meet our sales obligations. So there’s kind of a balancing act here going but then long term assets.

09:54

Once again, if we’re talking about property, plant and equipment, we want to see you know how how well we’re using Basically the property, plant and equipment, how well we’re turning over the property, plant and equipment. And then the total asset turnover will kind of be a summary of these reports, because then we’re going to be comparing total assets to sales, which will kind of summarize the receivables, the inventory and the fixed asset turnovers. So those will be great. And then we got the liquidity ratios. These include the current ratio, and the quick ratio, these are probably some of the two that people learn quickest, because liquidity is going to be one of the big problems, or one of the big concerns, that’s always a concern, meaning Do we have enough money to pay off the debt that’s going to be coming due within the next 12 months.

10:42

So it’s going to measure the ability to pay off short term obligations, those due within 12 months. So you want to get used to this term of liquidity. liquidity can be applied to basically assets in general, how liquid are the assets, meaning the most liquid asset is cash. So you can kind of think of cash as the benchmark of liquidity. Why is it liquid, because you can use it to basically do whatever you want to do, you can use it to pay off your debts, you have the most flexibility with cash. So then we’re going to be comparing other assets to cash such as accounts receivable, less liquid than cash, but we expect to receive cash soon on it. And therefore it’s fairly liquid. If you got investments and stocks and whatnot that you can trade or sell fairly quickly, then those are still going to be fairly liquid.

11:29

So we’ll be comparing, we’ll be taking a look at the liquidity of our assets, and then how liquid basically the company is in general, and then how how well the company can then pay the debts, then we have the debt utilization ratios, which include the debt to total assets, times interest earned and the fixed charge coverage, which provides information about the overall debt position of the company. So debt position, notice when you talk about financing the company, you got assets equal liabilities plus equity. So the equity the assets represent what the company has liabilities and equity represent how you how who has claimed to those assets are how your assets are financed. And so you’re kind of thinking about the the financing of the debt as compared to the equity and times interest earned how how well can you pay off, the interest is going to be concerned with the bank on that, you know, if you’re the bank, given a loan, that’s gonna be something you’re concerned with.

12:25

So ratios by user of financial data. So if you think about different users, what’s going to be the ratio of groupings that are most important to those users? So we have the potential investor or an securities analyst. So if you’re thinking about basically the from the standpoint of an investor, looking at the financial statements, what are the ratios you’re most concerned with? Typically, profitability ratios are your main consideration. Why? Because if you’re thinking about investments, you want to think about what the return is going to be in the future. And whether or not an investment in the company is going to the risk of your investment is worth the potential return that could be in the future. liquidity ratios are a secondary consideration, because you want to make sure that, that they’re going to be able to, you know, pay off their debts. The banker is concerned, like with liquidity ratios, mainly. So if you’re thinking about the banker, especially for short term obligations, the banker wants to know, hey, can can the the company pay off the obligations that are coming due soon?

13:26

And then the long term creditors for the organization, and they’re concerned with the debt utilization ratios and profitability ratios? So what’s the debt, you know, your debt as when you’re financing the company, the debt financing as compared to equity financing, and what’s your profitability, are you going to be able to pay off your obligations. So now let’s just take a quick look, we’re going to run through this pretty quickly in terms of just the equations, I’m not going to get into a lot of detail with it. But we’ll get into a lot more detail when we actually use these equations in practice problems. That’s where you want to spend your time and we’ll talk about that a lot more there. So once again, profitability ratios, so the profit margin is going to be calculated as net income divided by sales.

14:11

Notice we’re talking about the net profit margin bottom line of the income statement as as opposed to like a gross profit margin here. You can also take our gross profit margin or operating profit margin. So this is comparing the top line of the income or the bottom line of the income statement to the top line of the income statement, seeing how much of the money we’re actually basically keeping for unit sales. So how many for every dollar sales? How much are we keeping after all expenses, we have the return on assets or investment. That’s going to be the net income, bottom line of the income statement, divided by total assets. Now I’m going to mention this all the time when we go through our practice problems, and that is when you’re comparing an income statement account and a balance sheet account. You’re comparing two accounts that have different time frames.

14:58

The income statement is represented as January through December, if it’s for a year, and the balance sheet is as of a point in time, if you’re looking at the balance sheet, it’s as of the end of the period end of the year. So these two things, you’re trying to line up to things that aren’t using exactly the same time frame. And therefore, one way to try to fix that is to is to say that we’re going to divide by total our average total assets. So anytime that’s the case, you might take the balance sheet account, and try to average it in some way, the most common average that’s going to be out there will be taking the beginning balance, the beginning balance of the Year for the balance sheet account, plus the ending balance, and then dividing by two. Now note this, the sheet sounds somewhat arbitrary, it’s still kind of an arbitrary thing, because all we’re trying to do is come up with a number that is representative of some point in time type number, that we that is the best number we can use to compare to an income statement number.

15:56

So it may or may not actually be better, you know, in general, to take the beginning or the end of the year, we’re trying to come up with some average. And we’re taking those two points, because they happen to be the furthest away by time in in the time distribution that we’re looking at. But notice, they may not be the furthest away with regards to to the biggest and smallest amounts at any given time for total assets. So you can think about different type of averages that you could try to do, in certain circumstances to try to figure out the best average to use. Now note, if you’re coming from a standpoint from financial accounting, then you’re probably familiar with generally accepted accounting principles. And when people start saying, hey, the ratio, you could use this number or that number, depending on what you want to do.

16:42

Your tendency, if you deal a lot with generally accepted accounting principles is to say, well, what’s the standard? What is the regulation tell me to do. And notice when you’re doing when you’re doing analysis, especially from a from a financial analysis, there are no rules such as that there are some standards, some standards, that whatever you’re looking at, will be standard, whatever you’re looking at, you want to make sure that you know what their standard is. But there may not be any kind of when you’re just doing analysis, there may not be the same kind of standard. Because you’re able to use the numbers however you want to do whatever type of analysis you think is best. So if you want it to average the total assets in some other way, because you thought it was a better representation, you can do so when you’re looking at some kind of standard information that’s being provided by to you, then you want to understand what what the calculation they are using, will be. So again, if you’re coming from generally accepted accounting principles, that can be a little bit frustrating.

17:39

So in practice, you want to use the best ratio that you think is most applicable in in a book problem. If you’re taking a test or something like that, you want to make sure that you understand what their common practices or their standard is, for any ratio that they’re commonly going to be using. Okay, we have the return on equity, which is the net income over equity. Once again, we have a balance sheet and income statement accounts. So you might see it as net income divided by average equity. Then we have the asset utilization ratios, we have the return on receivable turnover, which can be sales divided by receivables. Once again, all of these are gonna have an income statement number and a balance sheet number. So you might see it as sales divided by average receivables, we can break down this turnover number. So these turnovers are the are the main kind of components that you kind of compare.

18:29

But you can break out this this receivable turnover, which will be somewhat abstract of a number that you will receive very good for comparing to industry standards and to trend analysis. But it’s nice to be able to break down a number that estimates how long a receivables are outstanding in days. And that’s what this average collection period does, which you can do by calculating accounts receivable divided by the average daily credit sales. Or you could take the days in a year and divided by the receivable turnover ratio that we would get up top here. Then we have the inventory turnover, you could see this in two ways. You might see it as sales over inventory, typically ending inventory in this format. Or you could see it as Cost of Goods Sold divided by the inventory or average inventory. So again, the bottom line might be inventory might see Cost of Goods Sold divided by inventory, Cost of Goods Sold divided by average inventory.

19:23

So just we may go into another presentation as to why someone might use sales over inventory and cost of goods sold over inventory the pros and cons of those. Just note in this course, we will typically be using the sales over inventory. But when you’re doing this in a book problem, for example, just make sure that you know what what you’re using it might be cost of goods sold compared to the inventory, we will mention that every time. We do the calculation for this pretty much every time I’m pretty sure when we work with practice problems. Then we have the fixed asset turnover, which is going to be the sales over the fixed assets which once again, you might say As averaged fixed assets, then we have the total asset turnover, which is the sales over the total assets, which you might see as average total assets. Once again, this one notice total assets is kind of encompassing these other turnovers.

20:14

So you can, you might hear these call just turns the turns ratios or something like that, you had the total asset turnover, which is, which is kind of encompassing fixed asset turns inventory turns receivable turns, then we have the liquidity ratios. liquidity ratios, as we saw include the current ratio and the quick ratio. Current Ratio is current assets divided by current liabilities. So, we’re trying to see how many times the current liabilities divide into the current assets. And so that’s going to give us an indication of how well we’re able to pay off the debts, the quick ratio is going to be basically restricting the numerator to something even more restrictive, basically taking out inventory. So that now we’re trying to see how many times current liabilities could be paid off in the quick assets, which does not include inventory any more. So then we have the debt utilization ratio ratios, debt to total assets.

21:10

So we have the total debt liabilities on the balance sheet divided by the total assets, comparing the liabilities to the assets, then we have the times interest earned, which is going to be income before interest in taxes, which sounds like a complex number. But really, you’re just taking net income on the income statement, backing out the taxes that are affected and the interest, so that you can then take your income before those items to see how many times over your revenue could have paid off the interest obligation, which is like the rent on money. So which is what would be concerned for, for a loan or bank or something like that, then you got the fixed charge coverage, which is the income before fixed charges and taxes divided by fixed charges. Now fixed charges are those that don’t change over time. And those will be something like the rent. So when when you increase or decrease the sales volume, the rent doesn’t really change, right? It’s gonna be fixed.

22:09

So we’re going to take the income before the fixed charges made, basically taking net income, and removing the fixed charges and taxes, and then seeing how many times over we can pay off the fixed charges. Now, once again, these are just a list of these, I know these can be overwhelming when you just see a list of ratios, the best way to understand these is just to do them over and over, I highly recommend doing them in Excel, but you don’t have to. But I recommend doing that we will do them both in Excel, and we will do them outside of Excel. So you can see see them some of these ratios will often be presented in a percentage format, sometimes they some of them will not be represented in a percentage format. So you kind of want to know the convention of one or the other when it’s a percent when it’s not a percent, you want to get good at being able to convert from a percent to a decimal and make sure that you understand that as well as be comfortable with rounding differences.

23:02

Because these are all estimates. And they’re not. In practice, they’re not going to almost ever be even numbers that you’re going to be working with. So you want to see what those rounding differences do. And I highly recommend doing them in Excel. So you can understand how to change the cells from or Google Google Sheets. So you can see how to change a cell from a percent to a decimal and you can see what the impact will be when you add decimals or subtract decimals or multiply using a cell that has an unrounded number in it. So those these are all things that you just you will become second nature if you just work the problems enough times.