Corporate Finance PowerPoint presentation. And this presentation we will discuss the differences between finance, accounting and economics, the differences between the fields of finance, accounting and economics Get ready, it’s time to take your chance with corporate finance, there’s a lot of overlap and differences between the fields of finance, accounting and economics, what we want to do is think about those differences. And where that overlap is, as we do so we will do so from the perspective of corporate finance, because that’s the objective of our viewpoint here for this particular course.

So from the perspective of corporate finance, what are the differences in terms of perspective of the fields of finance, accounting, and economics. Now, as we go into this, note that these three fields are very large fields in and of themselves. So there’s a lot of information, you can go into a lot of detail about particular areas within each of these fields of finance, accounting, and economics. But in general, from a corporate finance perspective, from our perspective, as if we’re doing corporate finance, for a business, a company, a corporation operating within an environment, raiment, that’s kind of the perspective we are looking at here.

01:14

So we think about the economics, then economics is generally going to give us the broad or big picture of the economic environment. So when you think about economics, from a corporate finance perspective, you’re kind of thinking about about taking a step back, and looking at the area or the field in which the corporation is operating the environment in which the corporation is operating. Now, economics is a huge field in and of itself, it’s typically broken out into two main categories being macro economics, and micro economics, macro economics, talking about things like GDP and inflation, and whatnot, which is clearly going to affect decision making policies from my corporate finance perspective. So we need to know those items from a corporate finance perspective, micro economics will start to get into into industries and behavior of, of companies, but it’s usually applied in terms of General, more general kind of perspective. So it’s still a little bit more broad than we would go into with corporate finance, although again, there’s going to be overlap. In those kind of calculations we might do from an economic perspective, especially from a micro economic perspective, possibly with a corporate finance perspective, then we have the accounting field.

02:28

So accounting typically provides historical financial data, and that historical financial data being typically the financial statements that including the balance sheet, the income statement, and the statement of cash flows. So these are the primary statements will typically be using in corporate finance as well, we’ll be using the accounting data, the difference typically will be if you’re talking about financial accounting, financial accounting is typically concerned with the creation of the financial statements and the accuracy of the financial statements. So when you’re thinking about accounting, if they’re if you’re in a corporation, you have the accounting department within the corporation, they are concerned with taking the financial data, looking at the actual transactions, making sure they record the transactions correctly, making sure that they compile those transactions properly into financial statements that are free of material misstatements. If you’re looking at public accounting, then they might be dealing with audit or attestation, in which they’re reviewing the financial statements providing a opinion on the financial statements, once again concerned with the accuracy of those financial statements.

03:37

So when you go into the finance, then you’re thinking more about the decision making process. So finance, instead of looking looking at the data, as it’s being processed to make sure that we’re recording the data that has happened properly, then we’re taking the data that has been recorded, and we’re typically looking forward to decision making processes in the future. So finance is going to be dealing with the decision making process. Looking forward. Now, this is going to be similar. There’s also overlap here within within finance and basically managerial accounting. Because when you’re looking into the future, you’re typically trying to predict what’s going to happen into the future to help aid managerial decisions, future oriented decisions, you’re going to make the future oriented decisions in part based on past performance, meaning income statement, statement of cash flows that are provided from the financial data, and based on where we stand at this point in time balance sheet type of information.

04:33

So both accounting and finance will rely on then that financial data so they’ll have that in common that financial data is going to be very important, but the accounting field will focus a lot more on constructing that financial data actually building it up making the financial data whereas the finance, the finance department will typically not be involved so much with the creation of the financial data. If If you go to the transactional perspective, they might not know, you know how to actually build the financial statement from scratch, they’re going to be using the financial data in order to make decisions in the future. So they’re going to take the end product, they’re going to be working more with ratio analysis and whatnot, to try to predict what to do in the future. So in order to do that, they’re going to take both the economic and accounting data to make decisions. So in the finance, again, you can kind of think of it’s similar to the decision making process, which would be similar to managerial accounting or management type of decisions.

05:34

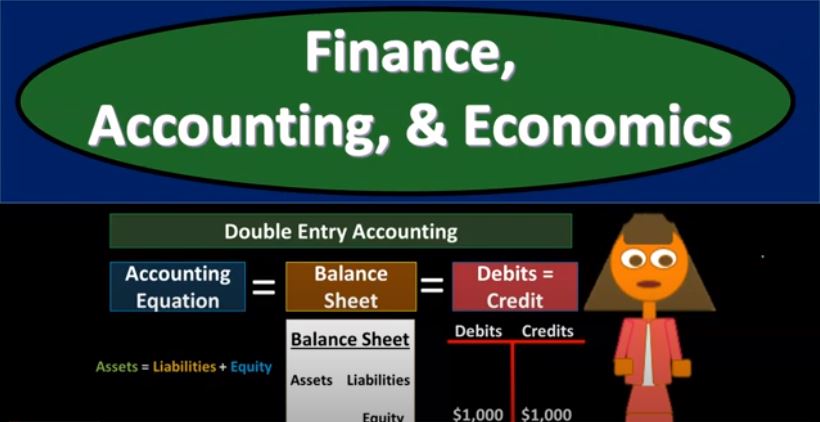

Because you’re thinking about a corporate a future oriented decision making process, in which you’re going to take a look at the current economics and project economic conditions into the future, you’re going to take a look at the current financial position, balance sheet and performance in the past to predict future performance in the future. And the tools that you’ll be using to do that will be, you know, the economic data and the accounting data to do that. So if we take a look a little bit more breakdown of these two, accounting and finances is often where people kind of have a confusion in terms of the overlap, because again, we’re using a lot of the same data, the finance, when you’re thinking about corporate finance, you’re going to be using the financial statements. And when you’re thinking about accounting, you’re going to be using the financial statements. So, so a little bit more breakdown on the detail between these two items. Notice when we think about the financial statements, we’re thinking about a double entry accounting system, in order to put together the financial statements.

06:32

So that’s what we’re using a double entry accounting system, both finance and accounting need to have an understanding of that, typically, the accounting will have more of a, you know, a deeper or different ways of looking at the double entry accounting system in because they’re going to be constructing these items including the accounting equation, you can think of the account, or the balance sheet is going to be also another way to see the double entry accounting system, and then the use of debits and credits. Now account this is really where things differ here is with these debits and credits, the debits and credits are the building blocks of the financial statements, we pretty much have to have them you got to learn debits and credits, if you’re going to break things down to actual financial transactions, and know how the financial transactions are being fed into the general ledger, the general ledger being used to make the trial balance, the trial balance than being made used to make the financial statements. So these are like the bricks that you have, you have to learn how to have these things are put together from the accounting perspective.

07:31

Therefore, the double entry accounting system for accountants needs to be broken down into these building blocks so that we can then record them on financial transactions. This is something that finance people typically don’t deal with, they don’t go down to the to the point of financial transactions, they’re going to basically be starting with the balance sheet, right. So the building of the actual transactions is where the corporate department of the accounting department will be looking into. And if you’re in public accounting, then you’re going to be you’re going to be reviewing what has happened. So you’re going to be you’re going to the thing has already been constructed by the corporate accountants, now you’re going to be looking at it from an audit perspective, you might be then taking the end result and drilling back down again into the actual financial transactions, which include actual debits and credits. And using the double entry accounting system, if you go if you go into finance, again, they’re probably not this whole debits and credits thing isn’t going to be isn’t going to be something that the focus is going to be on.

08:33

However, they still will be using the double entry accounting system, they’re going to be using it in the form of the accounting equation, assets equal liabilities plus equity. Now, that will typically materialize itself Most commonly, it’ll be in the balance sheet. So the balance sheet is is the assets equal to liabilities plus equity, it’s now in a in an equation or kind of format, which is what the which is what the finance department will be working with. So the accounting department will typically Build it up with debits and credits. Because it’s easier to do that it’s easier to work with, then convert those debits and credits from the double entry accounting system of debits and credits into an accounting equation, which is basically assets equal liabilities plus equity, and then demonstrate that present that to the readers and the way that’s most commonly or easily understood by the people that are going to consume the financial statements. And that includes the finance management and possibly investors and bankers and whatnot. So and that would be in terms of the accounting equation assets equal liabilities plus equity.

09:39

So notice that both both areas are going to be using this double entry accounting system finance and accounting have to understand the double entry accounting system. Finance needs to understand the double entry accounting system with regards to basically the balance sheet with regards to the accounting equation, understanding the relationship between assets, liabilities, and equity. They don’t take typically need to be spending a lot of time thinking about the building blocks or understanding the double entry accounting system in terms of a transaction by transaction basis as much, or in terms of the debits and credits themselves, the better we do understand the actual transactions, at least from a double entry accounting method for accounting equation, you’ll have a bit if you the better you have an understanding of how the actual transactions create the financial statements, then you’ll have a better understanding of the relationship of the financial statements possibly, and you’ll have a better understanding of what the ratios are telling us. But again, we don’t typically go back to the you know the transactions with as much detail on the finance what the finance will do is take a look at these these ratio analysis a lot, take a look at the financial statements and try to look at the trends that are taking place within them.

10:51

Which means we’re going to be spending a lot of time with the financial statements, analyzing the relationships between the numbers on them to make predictions between them and comparing and contrasting them to related companies to past performance and to industry trends. So bottom line here is when you look at the accounting department within the corporation, they’re starting from the transactions using debits and credits to build the financial statements and the audit department is basically using the financial statements to verify the accuracy of financial transactions going back to the debits and credits, when you think about the finance, finance is starting basically with with the end products with the financial data that have been created, using it to analyze where we stand at this point in time where we stand in respect to other companies with relation to the economic environment and then using it to make predictions into the future with that financial data so the finances using the financial data for you know this future oriented decisions. the accounting department is typically concerned with accurately creating and building the financial data.