Corporate Finance PowerPoint presentation. In this presentation, we will discuss the pro forma income statement, get ready, it’s time to take your chance with corporate finance pro forma income statement. Let’s first take a step back and think about the pro forma financial statements in general, remembering the fact that we got to do them in some type of order in order to do them in a logical fashion. And that would mean that we would first need the sales projection information, the production plan, we can use those in order to create the pro forma income statement.

00:31

Remember that the pro forma income statement is the activity statements kind of like the budgeted statement into the future, that’s what we think is gonna happen in the future. If you’re thinking about timing, you’re going to think about if you’re comparing this to a situation where you’re trying to figure out how many miles someone drove in like an hour or something like that, that’s gonna be like the income statement, it’s gonna tell us how far we went in terms of revenue generation, expense generation, and the net income. So that’s gonna be our performance statements. And then we also are going to need the cash budget, which we might need to take into consideration other budgets, including capital budget budgets, which would include capital purchase plans for things like property, plant and equipment.

01:10

Once we have the performance statement, which was the main one being the income statement, then we can think about, okay, that’s how far we went, how many miles we drove, for example, if we then want to see how where we will be at at the end of driving those many miles, then we have to think about where the odometer was before we started driving. And that’s going to be the prior balance sheet. That’s where we stood before we have the income statement. And then if we add the income statement to it, that will then give us basically our beginning or our ending balance sheet, which will basically be where we are at at the ending point. We’re focusing here on the income statement, as we do so we’re going to be considering these two components for it. Remember, they have to be done. In order to make the income statement, you got to start with basically the sales projections, thinking about our first line on the income statement, because with regards to basically everything we do, we’re trying to we’re trying to do it in order to generate, you know,

02:01

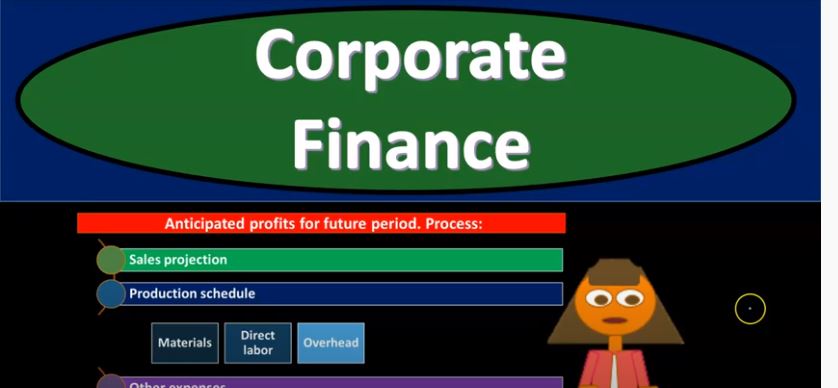

sales, sales is going to be the driving component. for it, even the balance sheet activity, everything that assets, the reason we have it is because we think that they’re going to be generating the sales in the future. So that’s the first thing that we’re going to be needing to project out. And then we can start thinking about our expenses, the main expense related to sales being if we sell inventory, the cost of the inventory, if we produce inventory, then the cost of us making that inventory. So we have the pro forma income statement, it’s going to be anticipating profits for future period. So obviously, we’re thinking about what’s going to happen in the future period, period, how far are we going to go profits, meaning revenue minus expenses, performance statements, sales and expenses, statements that need a time frame, in order to make any sense. So we have the sales projection, that’s what we’re going to start off with how many sales do we think we’re going to make top of the income statement, you’ll need that in order to do anything going forward on the pro forma financial statements, then we can think about the production plan.

02:59

So once we know what our sales are going to be, if we actually make inventory, then we’re going to have to think about what what we’re going to need to make whatever is going to be necessary for us to provide the inventory that we think are going to be sold. production plan will then take into consideration materials labor, and overhead, because that’s what goes into the production of inventory. However, if we simply are a retail business, then we might just buy and sell inventory. And then we would just think about our you know what we need to purchase in order to cover the sales. So then we have the materials labor and overhead. Remember, if you’re making inventory, or anytime you think about inventory, you’ll want to think about it in these three components, what’s the what’s the material going into it? What’s the labor in it, what’s going to be the overhead in it. Now, if you just purchase the inventory, and then resell it, that’s fine.

03:47

But when you think about inventory in general within the the marketplace and the production process, and you break it down into its components, the first breakdown of its components will typically be these three components, materials, labor, overhead, and then we have the other expenses that we’re going to need to be considering. Notice when we go down the income statement, we’re going to first think about sales and then the most important expense. The one that’s usually the largest, if we sell inventory is going to be the cost of goods sold related to the sales, we’re gonna have to figure out first, it’s also necessary to figure that out first, because that will be directly tied to the sales volume typically, meaning sales increasing and decreasing will adjust the amount of, you know, inventory that we’re going to need and will have a direct impact on the materials labor and overhead that are going to be necessary.

04:34

When we then go to the other expenses, which would include things like selling and admin expenses, it’s much more likely that these expenses will be less dependent on sales, more period type of costs, possibly more fixed in nature, and therefore we can we can figure these out. Possibly, you know, sometimes they’re a little bit easier to figure out because they might be similar to the prior period as we go forward in the future period, because they’re not as tied to us. Complete the fluctuations in the sales volume oftentimes. And then we’re going to calculate the projected profits, of course, the projected net incomes once we get the income and expense numbers down. So when we think about the number of units to produce, so now we’re back up here and the materials we’ve got the sales figured out, then we’re going to figure out okay, well, how many units do we need to produce, this is often going to be something that’s going to be a bit confusing, you’ll have a similar kind of thought process, if you’re simply a retail store that’s buying inventory, because you got to think about, okay, I know how many I’m going to sell here, or how many I think I’m going to sell.

05:35

But what if I sell more, I want to have that inventory units on hand, or I’m going to be able to make the inventory units that I’m going to need in order to sell more if I need to. And what about the fact that I already have beginning inventory already, I need to take that into consideration when thinking about how many more I need to purchase. So we then have to look at this, we’re going to say okay, well, we’re first going to think about the projected sales number. And then we’re going to add to that the Desired Ending Inventory. Desired Ending Inventory means that because we’re projecting sales, we want to have some cushion in case more sales happen. So we’re going to say I’m gonna always have some Indian inventory on hand, I want a Desired Ending Inventory, something that’s always in stock, in case there’s a run on the sales, and we’re able to make a lot of money all of a sudden, because for whatever reason, we sold more, right, we want to have some cushion involved there, that cushion will vary greatly depending on the industry we are in.

06:32

For example, if we are in a just in time type of system, if we can purchase our inventory very quickly and rapidly and rely dependently on our suppliers, then we might have a very small Indian inventory. And then we’re running really leanly, meaning we’re not having to have costs to track the inventory and things like that, we can simply rely on the purchases of the inventory as we go, that would be great. But you have to have a very good system and be relying on your vendors to do that. If you are not as reliant on the vendors, then you probably going to want a greater cushion of the inventory that will be enhanced. And so if we add these two together, that’s going to be the amount of units that we’re going to need. But then we have to take into consideration that we already have something in beginning inventory, most likely, because if you think about our strategy, we always want this Desired Ending Inventory. That means that at the end of last time period, we probably still have some in the desired ending inventory, which are now the beginning inventory.

07:31

And so those we need to subtract out, right, because we have the sales plus what we want in ending inventory, minus what we already have, that’s going to then give us the amount of units that we’re going to produce. And if you think about a retail store, how many units are you going to purchase, you can think about a similar scenario, right, you got the amount you’re going to sale sale plus the desired ending inventory plus the units that you already have on hand, that would be the desired the units that you would need to be purchasing. So then we have the cost of goods sold, which is going to be a major component, the biggest, you know, expense component on the income statement, Cost of Goods Sold being related to the cost of the inventory, that’s going to be sold on the income statement. So cost for inventory units sold during the period, cost flow procedure or assumptions.

08:19

So when we think about the cost of goods sold, and we’re projecting out into the future, then we have to think about, you know how we are identifying the units that we’re selling, we got to think about our flow assumption. So remember our flow assumptions here, if you if you have a kind of system where you’re making custom products, and all the units are different, and possibly there for that are more expensive, so maybe you’re making custom things, then you’re specifically identifying the inventory. So in that case, you know exactly what inventory that you’re selling. But if you’re selling things that are all the same in your standardizing what you are selling, then you’re going to lower the cost per unit because they’re all going to be standardized. And then when you sell them, you probably don’t know which exact unit you are selling. And you have to use some kind of assumption. So the common assumptions are going to be the first in first out assumption, the last in first out and the weighted average.

09:14

So we’re going to concentrate here when we do the practice problems on the two most common assumptions, or the most common assumption being the first in first out assumption, and then and then we’re going to concentrate on its opposite or the furthest away from it being the last in first out. So again, if you think about these assumptions, you’re tracking your inventory. If you have large inventory, expensive inventory or inventory and inventory, usually these things kind of go together that is different in nature than you will specifically identify the inventory and you’re gonna have to specialize your your projections. On the on the case that you have more specialized inventory, all the units are the same. You’re typically going to use one of these three. If you use one of these three most people will pick possibly the first in first out and then possibly With a weighted average, because it makes the most sense to them, because that’s going to mimic what you would hope the flow of the actual inventory would be. And then we’ll compare the first in first out and the last in first out.

10:12

Because these are kind of the opposites, or the furthest apart the two assumptions that are the furthest apart, you assume that you’re going to be selling, the first one that you that you have is the first one that you’re going to sell, as opposed to the last one that you have or make or purchase is the first one that you’re going to sell. But they’re just both assumptions, because you don’t know which one you actually sold. So in theory, either assumption is just as valid, right, and we’ll see what the effect then will be on, you know, ending inventory and the cost of goods sold and the net income between these two assumptions. And and that can have an effect on the taxes. So oftentimes, I think about it this way. The first in first out is what you would typically use for bookkeeping purposes. Most likely, if you wanted to look worse in a case of rising prices, then you might use lastin. First out, why would you Why would you want to look worse, possibly for taxes. So this could be in a case of rising prices lastin. First out will typically result in the company basically looking worse, oftentimes having less net income, possibly less taxable income, resulting in less taxes, and then the average would be somewhere in between, it would lie somewhere in between in terms of the value of your assets in inventory, and the cost of goods sold.

11:28

So these are the same kind of flow assumptions, same kind of problems that you’ll find in any kind of inventory flow assumption types of problems, we got the same kind of things that need to be taken into consideration when projecting them out into the future. Then we have the other expenses that could include the selling and admin expenses that we’re going to have to project out. Now remember, the selling and admin, unlike the, the cost of goods sold is usually going to be more not not so much based on the number of sales, although you could have sales commission or something like that, or bonuses and whatnot, they could be in here that could be tied to the sales number. But oftentimes, you’re going to have a lot more that’s, that’s going to be fixed in nature. That could be like selling salaries and stuff like that. Same with the administrative expenses, these are typically going to be things that will be similar from period to period, because they’ll include things like fixed costs, like salaried employees, like the executive salary and whatnot.

12:24

And those will typically be fixed in nature. So these are usually be easier to project out into the future, because they’re not going to change as much most likely with the change in sales volume, as is the case with the the cost of goods sold. And then we’ll have to calculate the interest is something that we’re going to be considering, of course on the debt, and then the tax expense are going to be items that we’ll take a look at. So the income statement, if we have a projected income statement, it’s going to look similar to a normal kind of income statement, right we’re going to the projected income statement will look similar to what we’ve been constructing in terms of an income statement. It’ll just be projected right? income, Cost of Goods Sold gross profit, selling and admin, depreciation operating profit, and then the interest expense earnings before taxes, then the taxes the earnings after the taxes.

13:10

This is our performance statement. If we were projecting this out into the future, if this is a projected income statement, it’s thinking about how far we think we’re going to go, it’s going to be one of the components that we will need to see where we will end up which is going to be what we’ll do on the balance sheet. So on the balance sheet, we’re going to take our beginning balance sheet that has already happened. Look at our income statement, how far we went to see the ending balance sheet or put together what we think the ending balance sheet balance sheet will be where we will stand at the end of the period.