https://youtu.be/OdjLcvkWPfY?list=PL60SIT917rv6ERsGZxM9V_IZLVybpgfNU

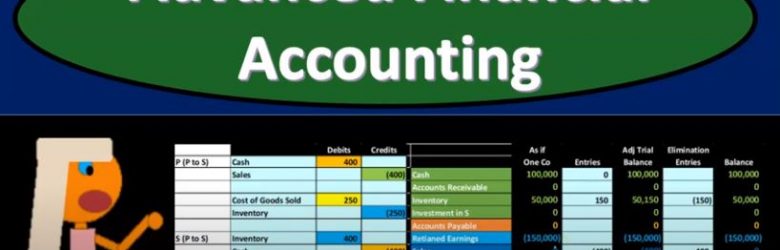

This presentation, we’re going to discuss the closing process for our accounting system. Get ready, because here we go with aplos. Here we are in our not for profit organization dashboard, let’s head on over to our Excel file to see what our objective will be, you’ll recall, we’re going to be in tab 10. By the way, we’re over here in tab 10. You’ll recall that we’ve been looking at each transaction with the accounts that will be affected, posting those over to our Excel worksheet to see the effect on the trial balance on the accounts. Now, we did this in terms of posting to our first trial balance up top and so row one. And then we said, okay, what if we break this information out, and I want to break this information out by not just the expenses by their nature, but by their function. Now, in aplos, we have a nice system to do that we’re going to use the phones and the classes, or the funds and the tax to do that here.