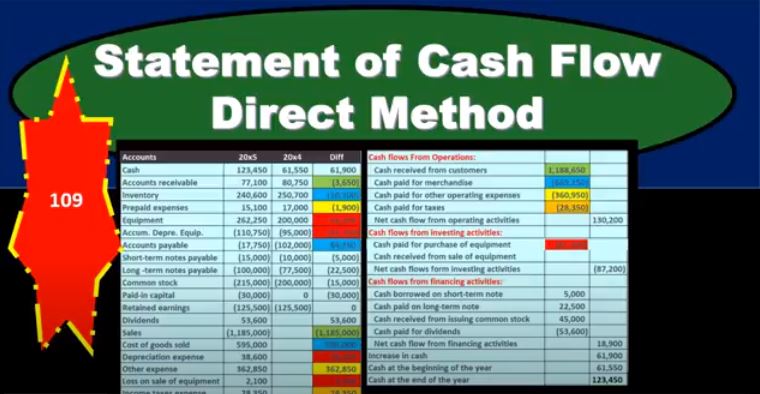

In this presentation, we will take a look at the statement of cash flows using the direct method. Here’s going to be our information we got the comparative balance sheet, the income statement and some additional information. And we will use this information to put together our worksheet which will be the primary source used to create the statement of cash flows using the direct method. This is going to be our worksheet. Now most of this worksheet will be similar to what we have done for the indirect method, in that we took the difference in the balance sheet accounts. So we’re taking the current year and the prior year, the current period, the prior period, all the balance sheet accounts, we’ve got cashed down to the retained earnings for the balance sheet accounts. But we’re also in this case going to give us the income statement accounts for the current period. So in other words, we’re going to break out the retained earnings the amount to its component parts, meaning we’ve got net income being broken out on the income statement. We’ve got sales cost of goods sold, the income statement accounts. So it’s going to be our same kind of worksheet here, we’re going to be in balance, we’ve converted it from a plus and minus format, we’ve removed all of the subtitles as we did under the indirect method.

01:16

And we converted it from a plus and minus format, as it is here on the financials to a debit and credit format, to verify that we are in balance in a trial balance. And remember to do that, we got to make sure that we’re breaking out the retained earnings to its component parts to the income statement. So this is the kind of the tricky thing to get this worksheet in place, meaning you took the balance sheet, and we’re saying we’re, we’re reconstructing the trial balance now kind of going in reverse. And that means that the retained earnings really is now the beginning retained earnings and all the activity dividends, net income, sales and expenses are not yet closed out to it. So you’ll note that in comparing that to 2000 the prior period there, we’re not going to show the income statement because I don’t need the income statement for the prior period, because it was closed out to retained earnings. So we’re gonna say that is closed out to retained earnings. But we’re going to show all the activity that happened in this in this time period, the current period, in terms of the revenue accounts not being closed out.

02:21

Why are we doing that? Why are we having this difference? Because when we look at the first component of the direct method, which is going to be the operations flow, cash flow from operations, we’re in essence going to reconstruct the income statement because that’s basically getting to net income, we’re basically going to get to this net income number, not using an accrual basis, but using more of a cash flow basis. So that’s what we’re going to try to do. So in order to do that. We’re going to list out this information that detail and what we’re going to do is go through these income statement accounts, sales, sales, and converted and say, well, it’s not sales anymore. It’s gonna be cash received from customers. And we’ll go through these accounts. And we’ll basically kind of convert them from an accrual basis to a cash basis, that’s going to be our goal. Now, note that the only difference between the direct and indirect method is in the cash flows from operations. So the indirect method takes net income and kind of backs into the cash flow on a cash flow basis from operations. Whereas the direct method is going to try to convert each line item, in essence to its cash flow basis.

03:33

So this is kind of it’s more direct, because it makes more sense. If you look at it, you can see I’m basically reconstructing here an income statement on a cash basis rather than rather than an accrual basis. So to do that, what we’re what we’re going to do is we’re going to say, okay, cash received from customers, that’s going to be kind of like, our sales item here. To pick up the cash received from customers. You’re going to say, Well, yeah, we’re going to pick up that sales item. But that’s not the only thing we’re going to pick up. Why because That sales item is on an accrual basis. How do we convert it to a cash basis? Well, if you think through it, you’re going to say, Well, what you know, what is sales happen? What happens in sales? There’s two journal entries that would happen? Well, the process of recording sales typically has that the sales cycle would be that we would debit the accounts receivable and credit sales, that’s the increase in this number, and then we would get the cash later on, which means we would debit cash and credit accounts receivable. Now anything that is still in receivable here is then not on a cash basis, meaning in this case, the receivables went from 80,007 50 down to 77,100. That would mean that we got more cash than we made sales in aggregate.

04:54

So that would mean that we’d have to adjust this account the sales account for that. So we’re going to take This 1001 85, add the 3006 50. Because we must have gotten, we must have gotten paid here, we got paid over and above the sales we made in 2005. So we’re going to have to basically net those two out and that’s going to be making then the cash received. So we’ve converted the sales to cash received by looking at the other account, that’s an accrual account related to sales. Then we’re going to do cash paid for merchandise, we’re going to do a similar process here and say, Okay, well what’s going to be involved with the cash paid for merchandise? Well, that’s going to mean that we’re going to have of course cost of goods sold. But we also have the inventory, it’s going to be part of that process, and we’ve got the accounts payable. So this is going to be more of a kind of a confusing process. We’re going to have to put these together in order to see what the cash paid for merchandise is going to be. And again, you can Through this by thinking of the journal entries, what’s the cycle for merchandise? Well, typically we would purchase the inventory debiting inventory crediting accounts payable. And then then we would pay for the merchandise we would credit cash and debit accounts payable.

06:16

And then at some point we would sell the merchandise, which means we would debit cost of goods sold. And that and that would be part of the sales process when we sell the merchandise. So these three accounts are going to be combined together to give us this 669 150. So we’ve got a deal when we have to cash pay for merchandise, you can see this gets to be a little bit confusing, because this cost of goods sold represents an accrual basis at the point of when the sale happened. Of course, when we paid for the cash, when we paid for the inventory, it’s going to be a different different scenario because the cash basis will differ from the accrual basis. So then we’re going to have cash paid for other operating expenses. So if we pick up those accounts, we’re going to have the other expenses here. And then we’re gonna have to say, Okay, is there anything that’s non cash basis for these other expenses? Whatever these expenses are? Is there anything up here that’s going to be an accrual type of account? If we have something like prepaid expenses, then that’s going to be an accrual type of account related to the other expenses. So any other expenses, then we’re trying to see, are they all cash expenses that we pay cash for them? Or is there some type of accrual related to them? If we’ve got prepaid expenses here, then we’re going to have to net those two together in order to get in this case, decreasing it by the 360,009 50.

07:41

So those two will be making up the cash paid to convert this number to an accrual basis. And note, what we’re doing here, of course, is finding a home for all these differences, just like we did with the indirect method, where at the end of the day, we’re going to get down to this 61,900 but we’re finding a home for all of these differences. We’re just going to kind of color code them as we go through this. Okay, so then we got cash paid for taxes. And that’s just going to be this item here. There’s no accrual basis up here, we don’t have any prepaid taxes or accrued taxes. So we’re just going to pull that over directly. And that will give us our total. So if we sum if we add up these, add them, subtract these up, we get to 130,200. Next, we’re going to have the cash paid for equipment and that’s going to be in the cash flows from investing activities. So we finished the net cash flows from operating activities. Now we’re going to go to the investing activities. Now the equipment is often the most messy item here because if we look at everything that’s related to equipment, on our statement here on our differences, we’re gonna say, Well, obviously equipment is going to be related there. And note that accumulated depreciation, we could say, well, the difference in accumulated depreciation is usually going to be the depreciation expense here, and if we were talking about the indirect method, we would be taking depreciation expense in the cash flow from operations because we would be starting at net income. And we would be pulling out the depreciation here, of course, the depreciation is not represented because we’re reconstructing it and therefore not including depreciation in our construction. So in order to add these numbers together in order to get them somewhere, we’re going to combine them together in this cash pay for equipment account. And then we’re going to go through any adjustments we need to make in order to break it out. So we’re going to say, Okay, I need to find a home for this one equipment, I need to find a home for this difference in accumulated depreciation, which you would think would match out to the depreciation expense, it doesn’t.

09:42

That means that there’s probably a sale that happened. So I’m just going to match those out now and this one number. And then I’m also going to include the loss which once again, if it was an indirect method, we will be pulling out of the net income number but because it’s a direct method, we’re just never going to included in that number. So again, I’m just going to combine that into this one number for now. So that we can find a home for it. And then we’re going to go back when we make our adjustments and try to say, Okay, what happened with the equipment? Did we buy equipment did refinance equipment, how much equipment did we buy, we sell equipment. And we’ll have to go through that whole process. So now, for now, we’re going to adjust, we’re just going to combine these numbers together, put them in there as cash paid for equipment and note that we’ll probably have to go back and look at that again. Now, most of the rest of this stuff is going to be similar to what we did on the the indirect method. So remember, the main difference is going to be the cash flows from operations. And then the equipment of course, is that kind of messy account because we have the income statement accounts, we have some differences that are on the equipment. If when we look at the rest of these numbers, we’re basically pulling over these numbers in a similar fashion, as we did in the indirect method. So well, so I’ll leave those accounts there.

11:03

Bottom line is we’re trying to get to the ending cash and Indian cash that ties out we’re trying to get to the cash here, the change 61,009 that matches here just like we did with the indirect method, and the Indian cash 123 400 that matches here, finding a home for all of these numbers, we’ll do that. We don’t really want to get into breaking out these numbers or pulling information or numbers from anywhere other than this worksheet, until we match this worksheet out and then think about what kind of adjustments we can do to trim this down, fix any problems that are there. Now if we look at these the added data again, we’re going to look at those journal entries related to the equipment. So we had the sale of equipment 26,050 the equipment cost 51, the depreciation 22 five, this is the journal entry that would be related to it. And again, in real life, we would look at the geo we’d find this transaction and and then Possibly pull out the paperwork related to it if we needed to. And then here’s the loss. So again, this is like a plug. So if we took, you know, the debits minus the credits, we would need a plug of 2100. It’s a loss because it’s a debit, also a loss because the cash received is less than the book value of 51 minus 222 850. Then we have this other one equipment that we purchased sticker price 113 250, we only paid 43,002 50 for it. So then we have this a note payable, this financing we dealt with. So this all deals with that equipment account. What are we going to do now to fix our equipment account? Well, if we go back here, note, we have this red item, we’re going to say okay, we’re going to do something to that. Now we need to go through this and say how are we going to use these journal entries to fix this number to make it you know, align what with what we think it should be, and yet not throw us out of balance. That’s our goal. That’s why we did it in this process.

12:59

When we look at this, it’s a little confusing because we can’t really go line by line, we’re going to try to look at this and say, Okay, what do we need to do to make this to make this work? We knew that the cash paid for equipment, we’re going to have to adjust that. Why? Because that that represents the actual cash flow here. So the cash paid for equipment, we’re saying was this 43,002 50. So what we’re doing here saying, well, that this number here needs to be that that 43,002 50. So we’re taking what’s what’s there, the 87 200 minus 243 250. And that should give us what it needs to be adjusted by, because that’s what this cash payment is made for. And then we got a cash receipt for equipment. And we know that we kind of included that here. And we know that that should be broken out because that’s cash that’s coming in. So we need another line item, we need another line item. And we know that’s the case. So we’re going to put that here. That should make these two amounts correct. And then the difference then is going to be going to happen paid for the long term note, because that’s where the other side of this of this happens. So the other side is going to be this notes payable. So the notes payable then is going to be the long term note, which we had here that should flip to be the correct amount. So it was at 25. And this actually looks like the cat like, like as if we received cash. So it needs to be flipped in the negative direction.

14:26

And then once we do that, we can kind of tie that out to the actual note, in terms of the cash paid for the long term note, we can look at the cash that was paid on the note which is going to be given in our example. So this is the type of transaction we’ll have in terms of increases and decreases, which should keep us in balance here should make this right this right and hopefully this right as well. So let’s see if we do that. Then if we do that to our worksheet, we’re going to say that the cash paid for equipment was at 87 to the 43 950 brings it to 43 to 50. Then we’re going to say that the Cash received from the sale of equipment was 2650 to 26,050. And then the cash paid for long term note was at 22 500 look like a receiving, we took it down 70 reversing it down to 47. So now this description is accurate. Now it’s cash paid, not received as it looked here. So then if we look at the full worksheet, then we could say, Okay, this is where we were at before, this number was right, this number was right, which was the summing up of these numbers, we had to fix this number, and this number and this number, we did so by having additions and subtractions that are in balance. So kind of like a journal entry, which left us with this hopefully being correct, Correct, correct, and still ending up in the same spot. So we’re still good, we should still be in balance. So then these numbers then are going to be like our final balance so we can kind of eliminate this stuff. And then be left with our final balance which would look something Like this again, this could be cleaned up further in just in terms of formatting and some terminology and whatnot. But this could be a worksheet, a step by step process to help us to get to a place where we’re in balance and we can you know, if we’re, if anything goes wrong, we don’t have to go back to the beginning kind of set this thing up and step by step process.