Hello in this lecture, we’re going to record an adjusting transaction related to accounts receivable. We’re going to record the journal entry over here on the left hand side and then post it to the trial balance on the right hand side trial balance and format of assets in green liabilities in orange equity in the light blue and the income statement in the darker blue including revenue and expenses, we’ll first walk through which accounts will be affected and then explain why that is the case. So we know that it is an adjusting entry and knowing that it’s an adjusting entry means it’s slightly different than a normal journal entry in that it does have two accounts like normal journal entries, but it also generally has one income statement account below the blue line and one balance sheet account above the blue line the light blue line, so it’s going to be one account above owner’s equity, one account below owner’s equity.

Posts with the Debit tag

Adjusting Entry Wages Payable 7

Hello, in this lecture, we’re going to record the adjusting entry related to payroll, we’re going to record the journal entry up here on the left hand side and post that post that to the trial balance over on the right hand side trial balance in terms of assets and liabilities, then equity and the income statement, including revenue and expenses, all blue accounts, including the income statement being part of equity, we’re first going to go through and see if we can find the accounts that will be related to a payroll adjusting entry. And then we’ll go explain why we are going through this process. So just if we have the trial balance, and we know it’s an adjusting entry related to payroll, we know that there’s going to be at least two accounts affected. And we know that because it’s an adjusting entry, it will be as of the end of the time period. In this case, let’s say it’s the end of the year 1231.

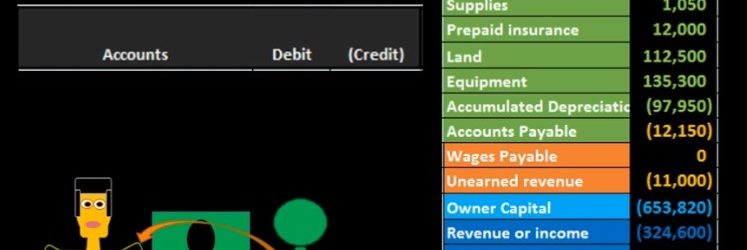

Adjusting entry unearned revenue 6

Hello in this lecture we’re going to record the adjusting entry related to unearned revenue. Remember that the adjusting entry is going to be a separate process. It’ll have the same rules as every journal entry. But we can add some added rules when we know that we are working with the adjusting entry process. For example, all adjusting entries will be as of the time period, the end of the month, or the end of the year. In this case, we have the unearned revenue. We know that all adjusting entries for the most part will have an account above the owners capital meaning and balance sheet account. So if we look at our trial balance, looking for an account related to unearned revenue, we see here unearned revenue. So we know that that’s going to be part of our journal entry.

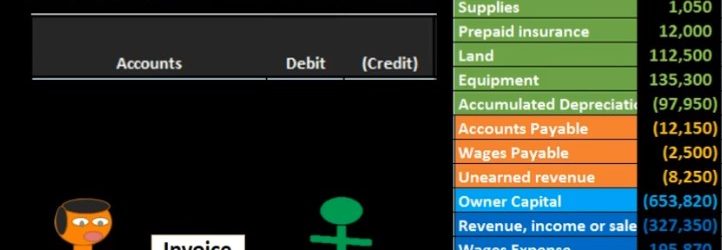

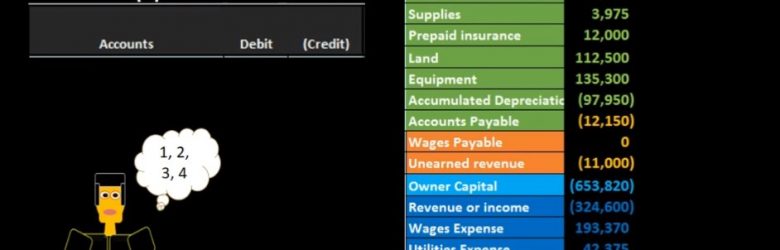

Adjusting Entry Supplies 5

Hello in this lecture, we’re going to record an adjusting entry related to supplies. Remember that adjusting entries are going to have their own set of rules, you want to keep them separate in your head. They are still journal entries, and they follow the journal entry rules. But if we know that we are dealing with adjusting entries, we can apply an additional set of rules to help us to understand what the journal entry will be. For example, the adjusting entries will all be at the end of the time period, the end of the month or the end of the year. And if we take a look at the supplies account, we also know that typical adjusting entries will always have an account in the balance sheet section in terms of the trial balance that’s going to be somewhere up above this owner’s capital account. So we look for an account on the trial balance related to this supplies. on the balance sheet we said how about supplies and we also note that the supplies, the adjusting entries will have an account below the equity section below the owner’s capital in the income statement, revenue and expenses.

General Ledger 245

Hello, in this presentation we will discuss the general ledger. At the end of this, we will be able to define what the general ledger is. We’ll list components of the general ledger and explain how the general ledger is used. When looking at transactions in terms of journal entries and posting those journal entries in track prior presentations, we were posting those journal entries mainly to a worksheet in order to see a quick computation over the beginning balance and what is happening to that balance, posting it to a format of a trial balance than an adjusting column and then an adjusted trial balance. Note, however, that we typically think of the journal entries being posted to a general ledger. The general ledger can be very complex when we look at it which is why it is often useful to not look at it when we first start posting the transactions but to see that how those transactions affect interest Visual accounts.

Accounts Receivable Journal Entries 230

Hello in this presentation we will be recording that journal entries for business transactions related to accounts receivable otherwise known as the revenue cycle. We will be recording these using debits and credits. At the end of this we will be able to list transactions involving accounts receivable record transactions involving accounts receivable using debits and credits and explain the effect of transactions on assets liabilities, equity, revenue, expenses and net income. We’re going to be recording these transactions up here on the left hand side constructing those journal entries in accordance with our thought process our list of questions to most efficiently construct the journal entries.

Cash Journal Entries with Cash 225

Hello in this presentation we are going to record business transactions involving cash using debits and credits. At the end of this, we will be able to list transactions involving cash record transactions involving cash using debits and credits and explain the effect of transactions on assets, liabilities, equity, revenue, expenses and net income. We’re going to record these transactions on the left hand side in accordance with our thought process. We’re then going to post them to a worksheet format, not necessarily or in this case, not a general ledger. But in a similar way, we will post it to this worksheet in order to see what is happening to each of these accounts individually as well as the groups of accounts in terms of assets, liabilities, equity, revenue and expenses, notes the order of the trial balance, always in the order of acids in this case in green liabilities in orange, and then we have the equity and revenue and expenses, the income statement accounts and net income at the bottom calculated as revenue minus expenses.

Financial Transaction Thought Process 160

Hello in this presentation we will be discussing the transaction thought process, a thought process used to record transactions in a systematic way. Objectives. At the end of this we will be able to list steps for recording transactions. Explain reasons for using a process when recording transaction and apply a thought process to recording transactions. First, we’re going to recap those rules we talked about in the prior presentation. If you have not seen the rules for the prior presentation, we recommend taking a look at that these rules are the rules we are going to use in order to construct a thought process. The rules being something that are just part of the process things that have to happen, the thought process being a system that we are going to use in order to learn this information as quickly and efficiently as possible and be able to record transactions as quickly and efficiently as possible.